- Weekly market focus

- Debt ceiling continues to pose considerable market uncertainty

- Markets will continue to assess the timing of QE tapering

- U.S. Covid infection rate falls to 1-3/4 month low

Weekly market focus — The markets this week will focus on (1) the prospects for the debt ceiling and the infrastructure and reconciliation bills, (2) continued concern about how the Evergrande debt crisis will unfold, (3) whether the U.S. Covid infection rate continues to fade, (4) the continued focus on Fed policy as the FOMC seems headed for a QE tapering announcement at its next meeting on Nov 1-2, (5) anticipation of Q3 earnings season, which begins next week with earnings reports from the big Wall Street banks, and (6) Friday’s payroll report (expected +488,000 after August’s disappointing report of +235,000).

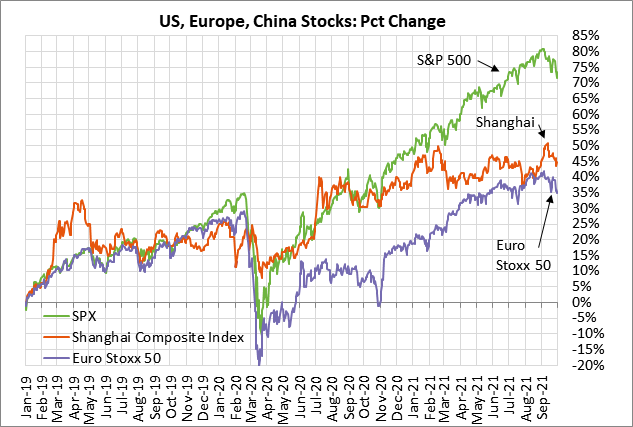

The Chinese markets are closed this week for a week-long holiday. However, the markets will continue to pay close attention to the Evergrande debt crisis in China. Evergrande has already missed bank interest payments and interest payments on bonds. The markets will continue to watch whether the Chinese government will launch some type of rescue program, or at least organize a debt restructuring that minimizes the impact on the financial markets and the economy. The Chinese central bank in the past two weeks has been consistently adding liquidity to the banking system to calm market nerves.

Debt ceiling continues to pose considerable market uncertainty — The markets continue to be very worried about the debt ceiling. Treasury Secretary Yellen last week set a drop-dead date of October 18 for a debt ceiling hike or suspension. That was on the earlier end of the recent estimate by the Bipartisan Policy Center that the Treasury’s X-date will be somewhere between October 15 and November 4.

On the X-date, the Treasury will run out of cash and will be unable to pay all the nation’s bills. The markets would be unhappy if the Treasury misses payroll checks to federal employees and the military, Social Security payments, and payments to vendors. However, the real impact would come if the Treasury were to miss an interest or principal payment on Treasury securities, which would represent a sovereign debt default. That could cause widespread panic and create a new financial crisis and recession.

The Democrats have no real option except to pass a debt ceiling hike through the reconciliation process, which is time-consuming. However, Democrats seem to think they can pressure Republicans into relenting and dropping their Senate filibuster. The longer Democrats wait to begin the reconciliation process, the more nervous the markets will get because Democrats might not get the bill done in time with reconciliation to prevent a Treasury default.

The markets are also closely watching the prospects for the $550 billion infrastructure bill and the Democrat’s $3.5 trillion reconciliation bill. The stock market would like to see those bills pass since the fiscal stimulus would boost the economy, although the stock market is clearly not happy about the corporate tax hike in the reconciliation bill.

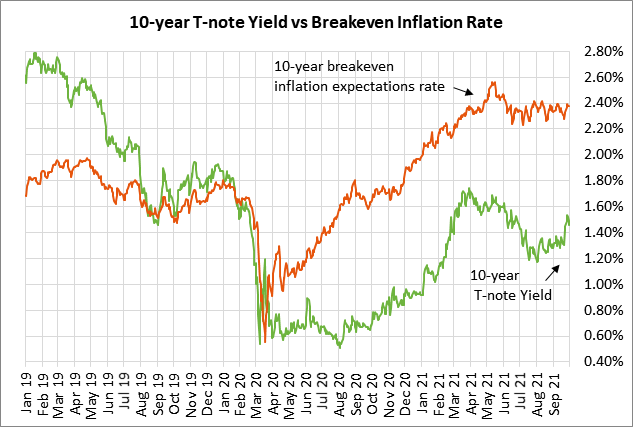

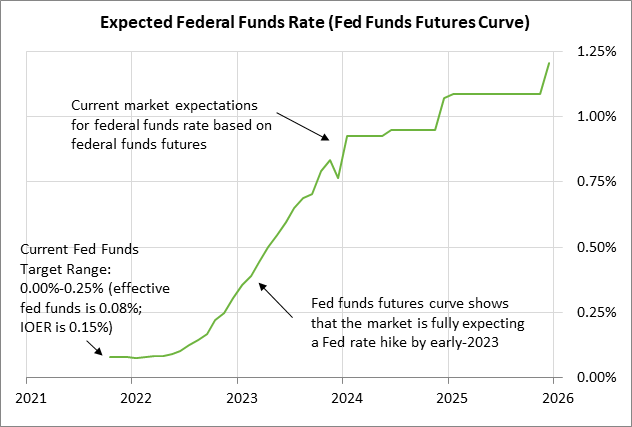

Markets will continue to assess the timing of QE tapering — The markets this week will continue to assess the timing of QE tapering and the Fed’s first rate hike.

The market consensus is that the FOMC at its next meeting on November 1-2 will formally announce QE tapering. The FOMC’s last post-meeting statement said, “The economy has made progress toward these goals. If progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.” Fed Chair Powell said at his post-meeting press conference that the tapering program will likely be concluded by mid-2022.

The markets are discounting about a 50-50 chance of a rate hike by the end of 2022 and a full chance of a rate hike by early-2023. That is in line with the updated dot-plot, in which half the 18 FOMC members expect at least one rate hike by the end of 2022, and the other half expect an unchanged rate. The dot-plot indicated a median forecast that the Fed will raise its funds rate three times for an overall rate hike to 1.0% by the end of 2023.

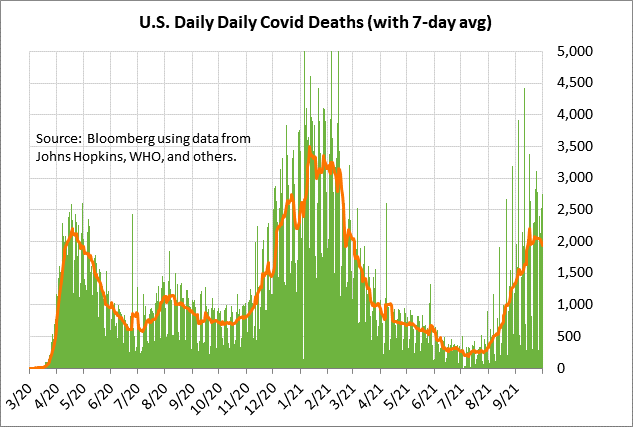

U.S. Covid infection rate falls to 1-3/4 month low — The markets are hoping that the recent decline in the Covid infection rate will continue. The 7-day average of new U.S. Covid infections last Friday fell to a 1-3/4 month low of 109,271.

Also, there is hope that the Covid death rate peaked after the 7-day average of daily U.S. Covid deaths last Friday fell to a 3-week low of 1,882.

The U.S. vaccination level continues to slowly climb, although the U.S. is still far away from herd immunity. The CDC reports that 64.6% of the U.S. population is now fully vaccinated against Covid, and 75.6% have received at least one vaccination dose.

Bloomberg reports that an average of 741,394 doses per day was administered over the past week, which is well above the area of +500,000 seen prior to the delta variant. The daily vaccination rate may start climbing further in the coming weeks as the U.S. starts to administer a third booster shot. The third booster shot should, in theory, help slow break-through Covid infections.