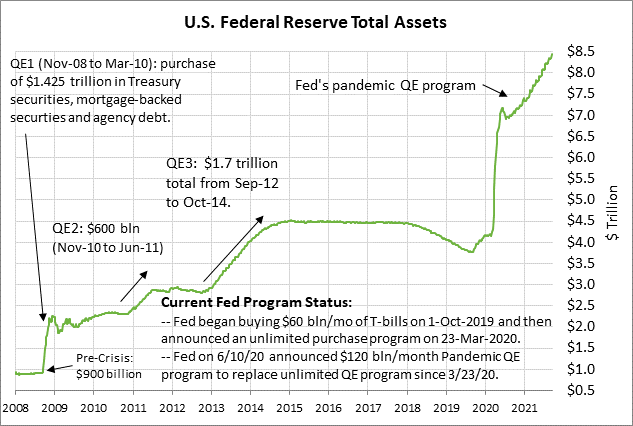

- FOMC indicates QE tapering is likely at next FOMC meeting

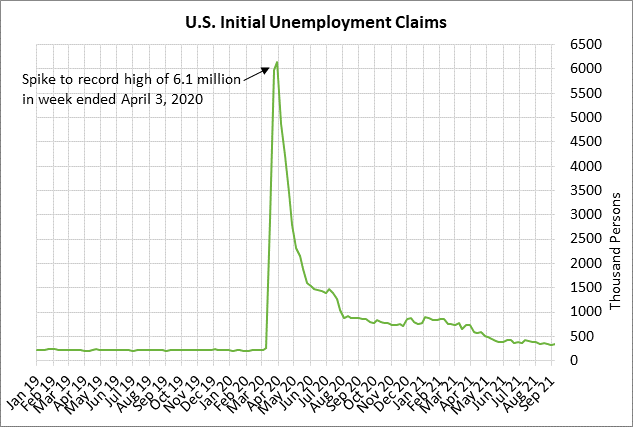

- U.S. unemployment claims expected to show continued labor market improvement

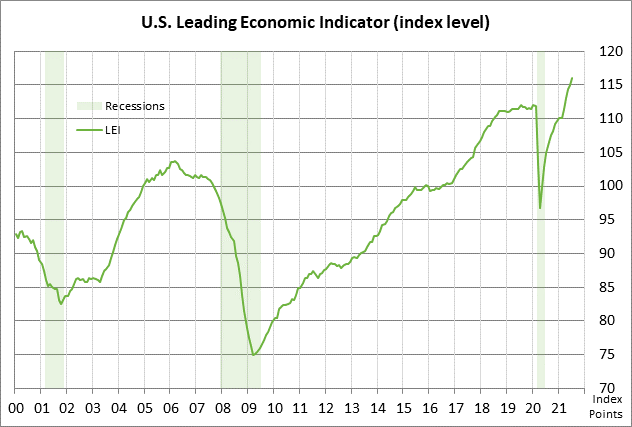

- U.S. leading indicators expected to remain strong

- 10-year TIPS auction

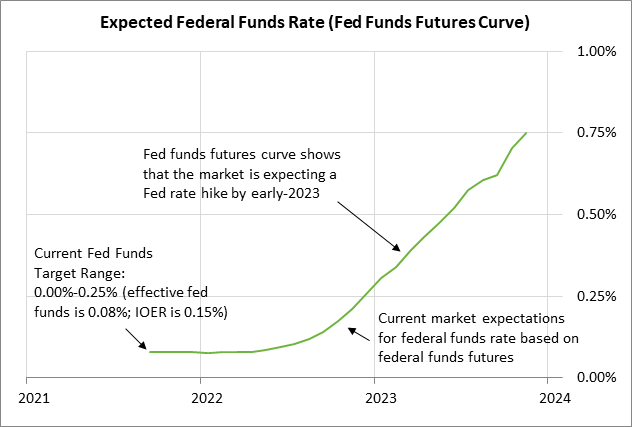

FOMC indicates QE tapering is likely at next FOMC meeting — The FOMC after the 2-day meeting that concluded on Wednesday provided the early warning about QE tapering that the markets had been expecting. Stocks closed higher after the markets were relieved that the FOMC did not go ahead with QE tapering at yesterday’s meeting. The federal funds futures curve was little changed through mid-2022, but tightened up by 1-5 bp for the contracts from mid-2022 through late-2023.

The FOMC’s post-meeting statement said, “The economy has made progress toward these goals. If progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.”

The FOMC’s language suggested that the Fed’s official announcement of QE tapering will come at its next meeting on November 2-3, assuming that progress towards the Fed’s goals “continues broadly as expected.” Yet, if there are unexpected negative developments for the economy over the near-term, then the FOMC could decide to delay the announcement until the following meeting on December 14-15.

The economy faces near-term risks as the pandemic’s resurgence continues and as there could be a crisis coming over the need to raise the debt ceiling. There is also uncertainty about the extent to which the Evergrande debt crisis in China could create fall-out and contagion for the global economy.

Fed Chair Powell, in his post-meeting comments, said that the Fed is likely to wrap up its QE tapering program by mid-2022. That would be a relatively quick tapering program that would leave the door open for a rate hike by late 2022.

Indeed, the markets were a bit surprised that two more FOMC members are now expecting at least one rate hike in 2022, bringing the total to 9 members who are expecting at least one rate hike in 2022. That means half of the 18 FOMC members are expecting at least one rate hike in 2022, and half are expecting rates to remain unchanged. The markets are not fully discounting the Fed’s first rate hike until early 2023.

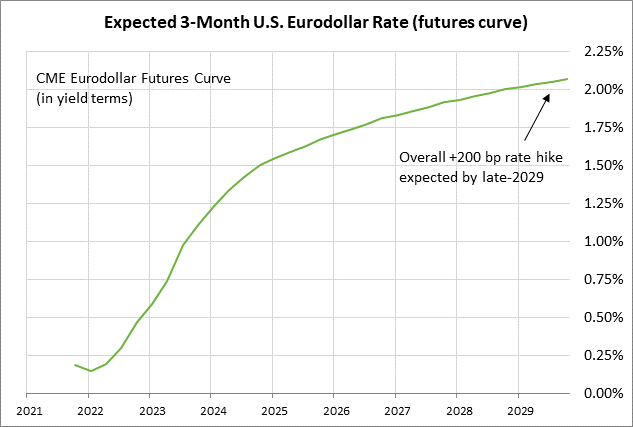

For the end of 2023, the dot-plot’s median forecast is for the funds rate to be at 1.0%, implying three rate hikes for a total rate hike of more than 75 bp. By the end of 2024, the median forecast is for a funds rate of 1.8%, which implies a total rate hike of nearly 175 bp. The effective federal funds rate is currently at 0.08%, which is below the 0.125% mid-point of the 0.00%/0.25% target range.

Mr. Powell again stressed that there is no direct connection between the timing of QE tapering and the Fed’s first rate hike. He said, “The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest-rate liftoff. He said that he didn’t expect the Fed to begin raising interest rates until the QE tapering program is over in mid-2022.

U.S. unemployment claims expected to show continued labor market improvement — The consensus is for today’s weekly initial unemployment claims report to show a decline of -12,000 to 320,000, reversing part of last week’s +20,000 increase to 332,000. Continuing claims are expected to fall -55,000 to 2.610 million, adding to last week’s decline of -187,000 to 2.665 million.

The initial and continuing claims series are both in very good shape, at or near 18-month lows. Relative to pre-pandemic levels, initial claims are now elevated by only 116,000 and continuing claims are elevated by 975,000 million.

However, improvement in the U.S. labor market might be stalling due to the resurgence of the pandemic. The markets were very disappointed by the Aug payroll report of +235,000, which was much weaker than the consensus of +610,000. The payroll report suggested that some businesses are pulling back on their hiring as they wait to see what happens with the pandemic’s resurgence.

U.S. leading indicators expected to remain strong — The consensus is for today’s Aug leading indicators report to show an increase of +0.7% m/m, adding to July’s increase of +0.9%. The LEI since March has soared by a total of +5.4% and was up by +10.6% y/y in July.

The consensus is that U.S. GDP growth peaked at +6.6% (q/q annualized) in Q2 and will ease to +5.0% in the current third quarter and remain little changed at +5.1% in Q4. On a calendar-year basis, the consensus is for GDP growth of +5.9% in 2021, which would easily overcome the -3.4% loss in 2020. The market is then expecting GDP growth to ease to +4.2% in 2022 and +2.4% in 2023.

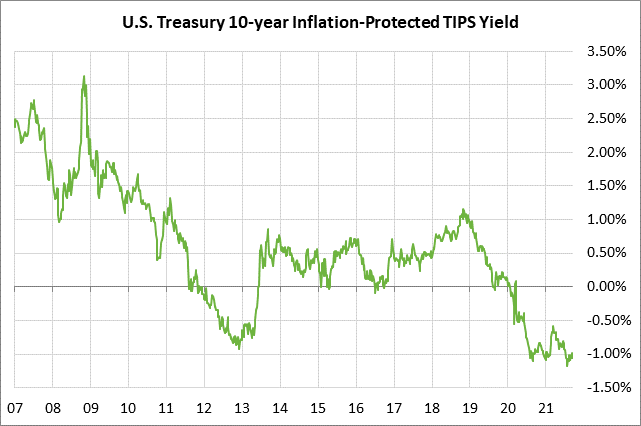

10-year TIPS auction — The Treasury today will sell $14 billion of 10-year TIPS in the first of two reopenings of the 1/8% 10-year TIPS of July 2031. The benchmark 10-year TIPS yield yesterday closed at -0.98%.

The 12-auction averages for the 10-year TIPS are as follows: 2.46 bid cover ratio, $26 million in non-competitive bids, 6.9 bp tail to the median yield, 31.4 bp tail to the low yield, and 50% taken at the high yield. The 10-year TIPS is the third most popular security among foreign investors and central banks, behind the 30-year and 5-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 67.5% of the last twelve 10-year TIPS auctions, well above the median of 62.2% for all recent Treasury coupon auctions.