- FOMC expected to wait until November for formal QE tapering announcementÂ

- House passes combined CR and debt ceiling suspension that will be filibustered by Senate Republicans

- U.S. existing home sales expected to give back most of July’s gain

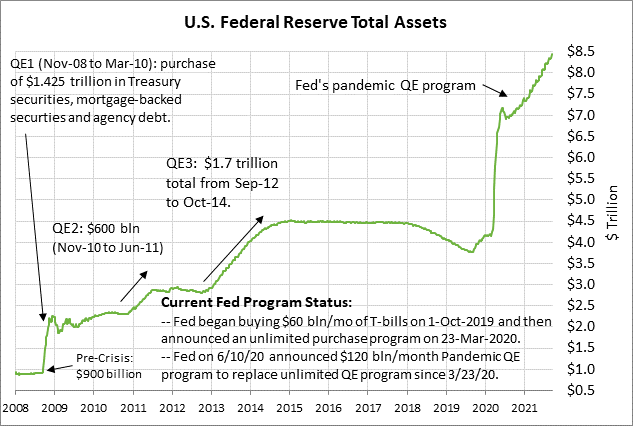

FOMC expected to wait until November for formal QE tapering announcement — The FOMC today will conclude its 2-day meeting with the usual release of the post-meeting statement and a press conference by Fed Chair Powell. The FOMC today will also release an updated Summary of Economic Projections.

The market consensus is that the FOMC will wait until November to formally announce QE tapering. However, the FOMC today seems likely to add warning language to its post-meeting statement that constitutes the advance warning about QE tapering that the Fed has promised.

A survey of 52 economists by Bloomberg released last Friday found that two-thirds of the respondents expect the Fed to formally announce its QE tapering at its next meeting on November 2-3, with the tapering beginning in either December or January.

The Fed is not expected to formally announce QE tapering as soon as this week due to (1) the weak Aug payroll report of +235,000, (2) uncertainty about the pandemic’s resurgence, (3) the possibility of a debt ceiling crisis, and (4) the possibility of major fall-out from the Evergrande debt crisis in China.

Fed Chair Powell at the Jackson Hole conference on Aug 27 indicated that the conditions have been met for QE tapering. He said the Fed believes that the economy has now met the test of “substantial further progress” toward the Fed’s inflation objective and that the labor market has also made “good progress.” He said that at the last FOMC meeting in late July, “I was of the view, as were most participants, that if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year.”

The markets were pleased that Mr. Powell, in his Aug 27 Jackson Hole comments, went out of his way to stress that the beginning of QE tapering will not bring interest rate liftoff any closer. He said, “The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test.”

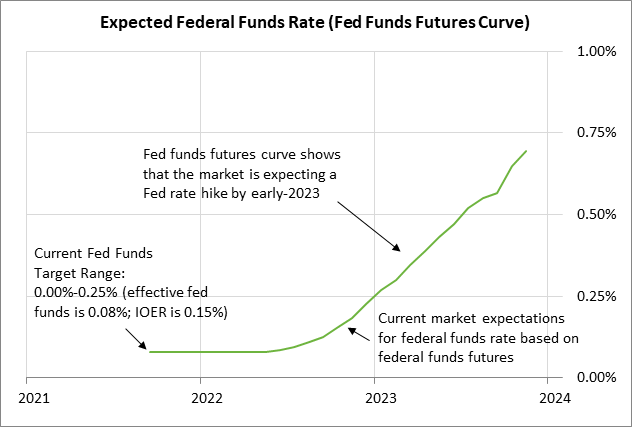

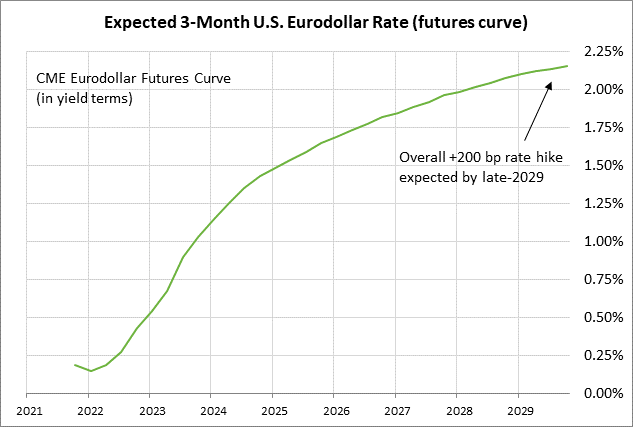

The market consensus is that the FOMC will not start raising interest rates until early 2023. The federal funds futures market is discounting two 25 bp rate hikes in 2023, with further rate hikes coming in the following years.

The FOMC today will release an updated dot-plot forecast of the funds rate, replacing the last version that was issued after the June 15-16 meeting. The June dot-plot showed that 11 of 18 FOMC officials saw two rate hikes by the end of 2023, which was more than the 5 members in March who expected at least two rate hikes. Moreover, 7 of 18 members in June expected a rate hike as soon as 2022, up from only 4 in March.

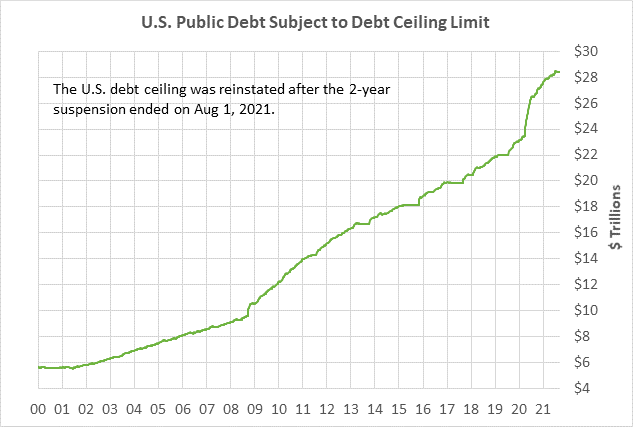

House passes combined CR and debt ceiling suspension that will be filibustered by Senate Republicans — The House late Tuesday approved a bill that contained the continuing resolution, a debt ceiling suspension, and aid for hurricane and wildfire recovery and for Afghan refugees. The CR would last until December 2. The debt ceiling suspension would last until December 16, 2022, which is after the November 2022 mid-term elections.

The Senate is not expected to be able to pass the combined CR/debt ceiling suspension because there aren’t 10 Republican votes to approve cloture. After Majority Leader Schumer makes clear that Republicans are filibustering the bill, the Senate may strip out the debt ceiling suspension but approve the CR, and send that back to the House. If the House approved that clean CR, then a government shutdown beginning next Friday (Oct 1) would be averted.

However, Democrats would be no closer to solving the debt ceiling problem. If Democrats are unsuccessful in getting Republicans to help pass the bill in the Senate, the Democrats could still pass a debt ceiling hike by including it in the $3.5 trillion reconciliation bill. But that reconciliation bill is already facing significant problems in the Democratic caucus and it remains to be seen if, or when, that bill might pass.

Another potential emergency strategy would be for Senate Democrats to vote to strip the filibuster from a debt ceiling suspension bill, thus allowing the debt ceiling suspension to pass without Republican votes. However, there would probably be some Democratic Senators who would not agree with the idea of stripping the minority party’s filibuster rights, even if it applied only to a debt ceiling bill.

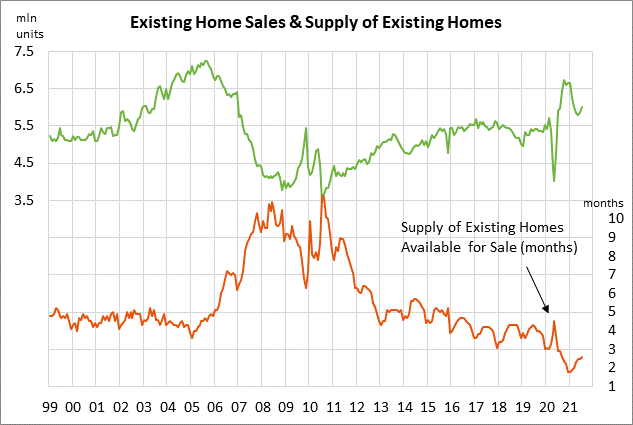

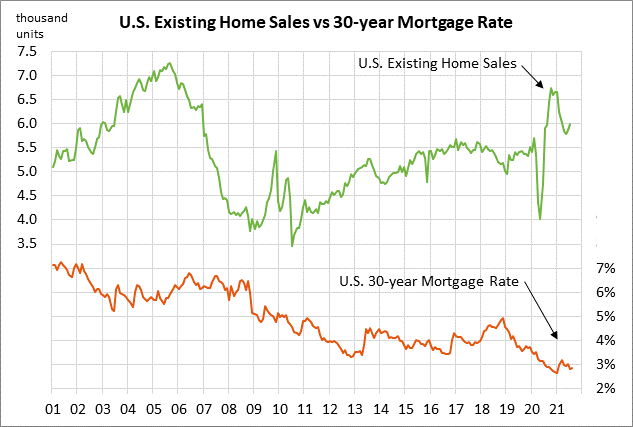

U.S. existing home sales expected to give back most of July’s gain — The consensus is for today’s Aug existing home sales report to show a decline of -1.8% m/m to 5.88 million, giving back most of July’s +2.0% increase to 5.99 million. U.S. existing home sales posted a 15-year high back in October 2020, but have since fallen by a total of -11% to 5.99 million units. Home sales are still above pre-pandemic levels but have fallen back due to a low inventory of homes on the market and high prices.

The supply of existing homes on the market was at 2.6 months in July, which was below the pre-pandemic level near 4 months. Strong demand has hoovered up many of the homes that were for sale, thus leaving few homes on the market. Meanwhile, high home prices are causing some resistance among potential homebuyers and are hurting sales. The FHFA U.S. home price index has soared by +22% from the pre-pandemic level.