- Weekly market focus

- House expected to vote this week on CR and debt ceiling hike

- Consensus is that FOMC will wait until its November meeting for formal QE tapering announcement

- U.S. Covid infection rates plateau at high level

Weekly market focus — The global markets this week will focus on (1) the FOMC meeting on Tuesday/Wednesday and comments by Fed Chair Powell and other Fed officials on Friday at a Fed panel, (2) House consideration of the CR, debt ceiling hike, $550 billion infrastructure bill, and $3.5 trillion reconciliation bill, (3) whether the U.S. Covid infection rate starts to fade, (4) the Evergrande crisis in China as the government tries to prevent contagion from the massive property developer’s expected debt default, and (5) the Treasury’s sale of 20-year bonds and 10-year TIPS.

House expected to vote this week on CR and debt ceiling hike — The House returns today from its summer recess and the legislative crunch will begin. The Senate already returned to Washington last week.

House Majority Leader Hoyer last Friday said that the House this week will hold votes on a continuing resolution (CR) and a debt ceiling hike. There was no decision as of last Friday about whether the debt ceiling hike would be attached to the CR or would be a standalone bill.

The House and Senate both need to pass a CR to providing funding authorization for the federal government for the new fiscal year that begins on October 1. Without a continuing resolution, there will be a partial government shutdown starting on October 1.

The House will likely be able to pass a debt ceiling hike (or suspension) this week. However, the debt ceiling hike will then be bogged down in the Senate, where it will not be able to pass without votes from at least 10 Republican Senators to avoid a filibuster.

Democrats and Republicans have indicated no flexibility and appear to be on a collision course towards a debt ceiling crisis. Both sides seem willing to risk a sharp stock market sell-off that would pressure the other side to act. Democrats could pass the bill without Republican help if they wished by putting it into the reconciliation bill. However, it is unclear whether Democrats could even pass a reconciliation bill by the time the Treasury’s X-date arrives in late October or early November.

Aside from votes on the CR and debt ceiling, House Speaker Pelosi has promised moderate House Democrats that she will hold a vote on the $550 billion infrastructure bill by next Monday (Sep 27). If House Democrats were to approve the same bill that has already been passed by the Senate, then Congressional approval would be complete and it would go to President Biden’s desk for his signature. However, it seems more likely that Ms. Pelosi will encourage the House to pass a slightly different bill so that the infrastructure bill is not finalized and she can continue to use the bill as leverage to force moderate Democratic Senators to vote for the $3.5 trillion reconciliation bill.

House leaders reportedly plan to hold a House vote on the $3.5 trillion reconciliation bill before the new legislative period begins on October 1. However, the reconciliation bill faces a torturous path in the Senate due to opposition from some moderate Democratic Senators to the overall size of the bill and some of its provisions.

Consensus is that FOMC will wait until its November meeting for formal QE tapering announcement — The consensus is that the FOMC will wait until November to formally announce QE tapering. However, the FOMC at its 2-day meeting this week (Tue/Wed) is expected to add warning language to its post-meeting statement that constitutes the advance warning about QE tapering that the Fed has promised.

A survey of 52 economists by Bloomberg released last Friday found that two-thirds of the respondents expect the Fed to formally announce its QE tapering at its next meeting on November 2-3, with the tapering beginning in either December or January.

The Fed this week is not expected to formally announce QE tapering due to (1) the weak Aug payroll report of +235,000, (2) uncertainty about the pandemic’s resurgence, and (3) the possibility of a crisis in Washington over the debt ceiling in October.

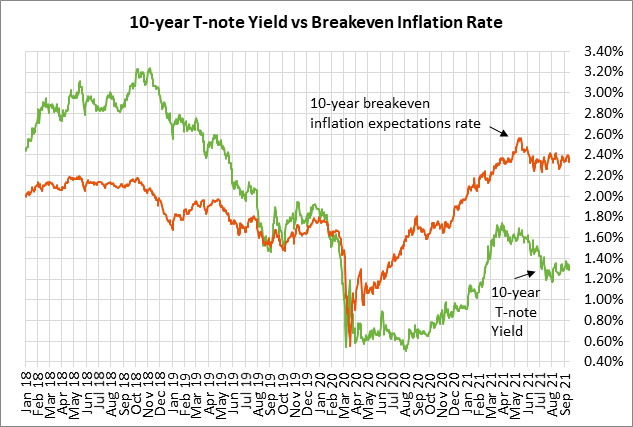

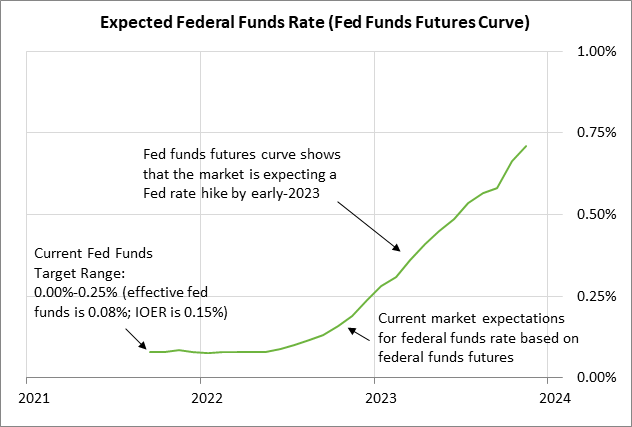

Regarding interest rates, the Bloomberg survey found a consensus that the Fed will leave its funds rate unchanged through 2022, but then raise rates twice in 2023 and three times in 2024. That is roughly in line with market expectations as reflected in the federal funds futures market.

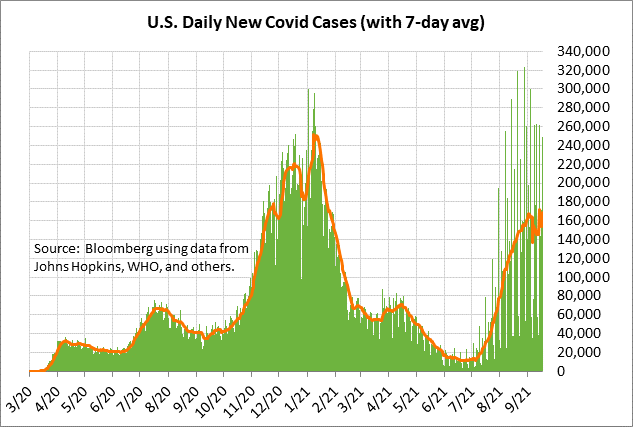

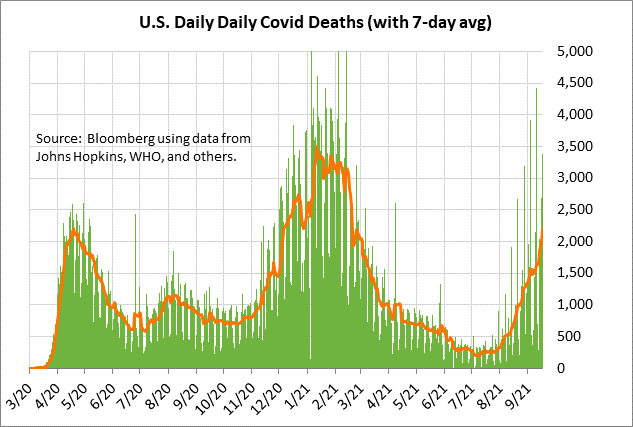

U.S. Covid infection rates plateau at high level — U.S. Covid infection rates have stabilized, but a high level that poses high risks for the general populace due to continued high non-vaccination rates and the threat of breakthrough infections for those who are vaccinated. The pandemic is expected to continue to hamper the U.S. economy.

The 7-day average of new U.S. daily Covid infections has been stuck in the high range of about 140,000-170,000 for the past month. Meanwhile, the 7-day average of daily Covid deaths last Friday hit a new 7-month high of 2,230.

The U.S. Covid infection rate remains high due to the large number of people who are not vaccinated and due to the transmissibility of the delta variant even to people who have been vaccinated. Bloomberg reports that an average of 781,574 doses per day have been given over the past week, which is higher than the 500,000 area seen before the delta variant emerged. The CDC reports that 54.4% of the U.S. population has now been fully vaccinated, while 63.6% have received at least one dose.