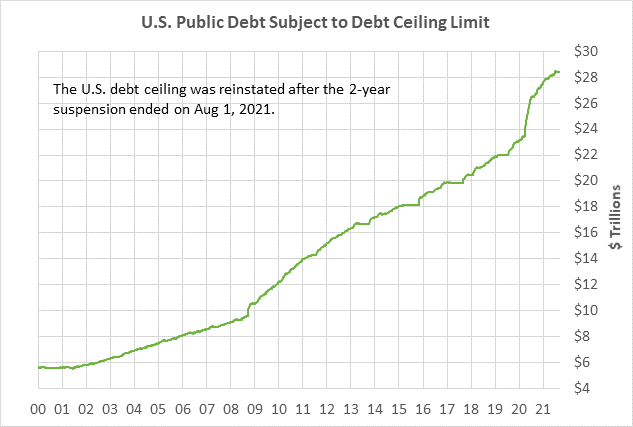

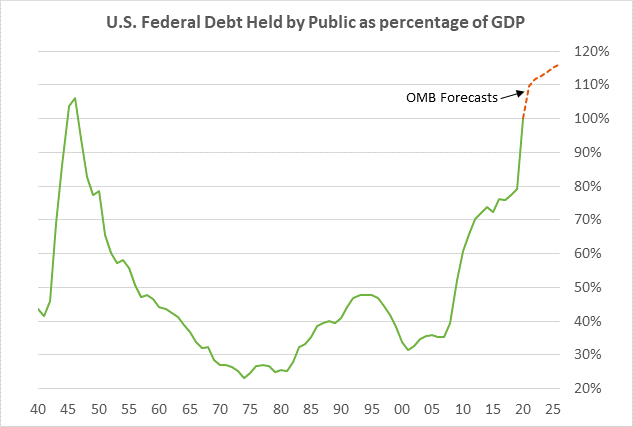

- Washington barrels toward another debt ceiling crisis

- U.S. manufacturing production expected to remain strong

Washington barrels toward another debt ceiling crisis — Washington is quickly heading towards another debt ceiling crisis as Democrats and Republicans are on a collision course, with neither side indicating any flexibility.

The current Democratic plan is to add a debt ceiling hike or suspension to the upcoming continuing resolution, along with hurricane aid. Democratic leaders believe that Republicans will be forced to allow the bill to pass, lest they be blamed for the combination of a U.S. government shutdown, a sovereign debt default, and a lack of aid for hurricane victims.

Politico reports that Democratic leaders believe that Republicans will cave in under pressure from Republican business leaders who would be aghast at a plunge in the stock market if the serious threat arises of a sovereign debt default.

However, Republicans are highlighting that Democrats have control of the White House and Congress and that Democrats therefore have the responsibility of passing a debt ceiling hike, particularly since they could do so by putting it into the reconciliation bill and bypassing a Senate Republican filibuster. Republicans believe that Democrats will take the brunt of the blame for a government shutdown and a sovereign debt default since they have majority control of Washington.

Senate Minority Leader McConnell yesterday said, “Republicans are united in opposition to raising the debt ceiling.” Mr. McConnell said that Republicans oppose raising the debt ceiling “not because it doesn’t need to be done but because doing so would pave the way for Democrats to pass their $3.5 trillion spending bill.

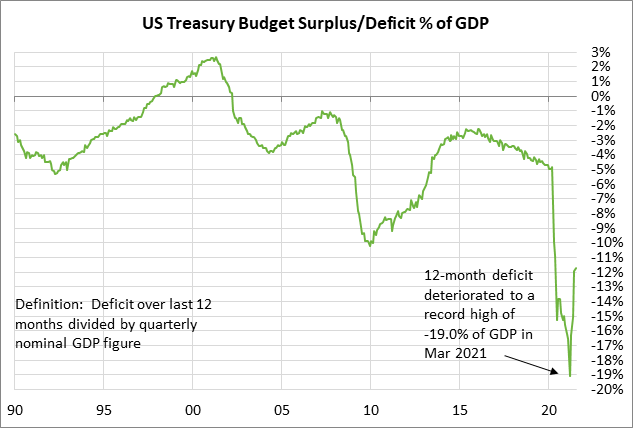

Democrats counter that argument by pointing out that the debt ceiling needs to be raised to pay for spending obligations that were already made by previous administrations, including the $7.8 trillion rise in the national debt seen during the Trump administration.

The strategy of both sides is essentially to create a crisis to try to force the other side to back down. The stock market may soon be the victim of the latest example of Washington dysfunction. There are numerous examples in the past several decades where Congress refused to act on a bipartisan basis until a free-fall in the stock market forced Congress to act.

There are now only two weeks left until the end of the fiscal year on September 30. House Speaker Pelosi reportedly plans to put a continuing resolution on the House floor next week for a vote, then send it over to the Senate for action before September 30.

By next week, it should be clear whether Democrats will follow through with their reported strategy of including a debt ceiling hike in the continuing resolution. Alternatively, they could choose to bring up the debt ceiling hike as standalone legislation or as part of the reconciliation bill. However, putting the debt ceiling into the reconciliation bill would be a Plan B that would only be executed if Democrats become convinced that they will never get the 10 Republican votes in the Senate that they need to approve a debt ceiling hike by regular order.

The Bipartisan Policy Center last Friday said that it has narrowed down its estimate of the Treasury’s X-date to between mid-October and mid-November, which is only a month away. The BPC’s director of economic policy said, “Given the current pace of federal spending and revenues, we are reasonably confident that the X Date won’t arrive before the start of the fiscal year, or even the week or so following. But the train could go off the rails shortly thereafter, and just because Congress has a bit more breathing room than previously expected, doesn’t mean lawmakers need to use it.”

When the Treasury reaches its “X Date,” the Treasury will be out of cash and will start defaulting on its financial obligations. At that point, the Treasury will only be able spend the cash that it is collecting from tax revenues. It is unclear whether the Treasury would be able to prioritize the bills that its pays, perhaps allowing it to keep paying interest and principal on Treasury debt and avoiding a sovereign debt default. However, even if the Treasury can pull off that trick, it will still be unable to pay all of its bills, perhaps including military salaries, Social Security payments, and other politically-important expenses.

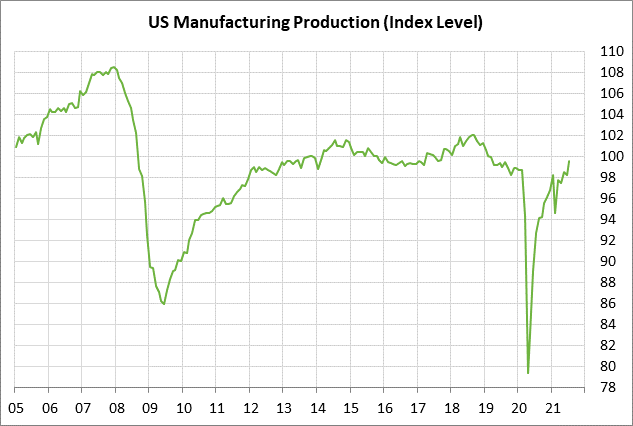

U.S. manufacturing production expected to remain strong — The consensus is for today’s Aug manufacturing production report to show an increase of +0.4% m/m, adding to July’s sharp gain of +1.4% m/m. The broader Aug industrial production report is expected to show an increase of +0.5% m/m, adding to July’s increase of +0.9% m/m.

Manufacturing production has been very choppy this year and has yet to see a monthly gain for two consecutive months. There was a big +3.4% m/m increase in March, but that was followed by reports of -0.3% in April, +1.1% in May, -0.3% in June, and +1.4% in July. The year-on-year figures have been strong, but that has little meaning since the U.S. economy was partially closed down a year ago. However, the manufacturing sector is clearly picking up steam, as seen by the fact that manufacturing production rose by +8.8% in July on a 3-month annualized basis.

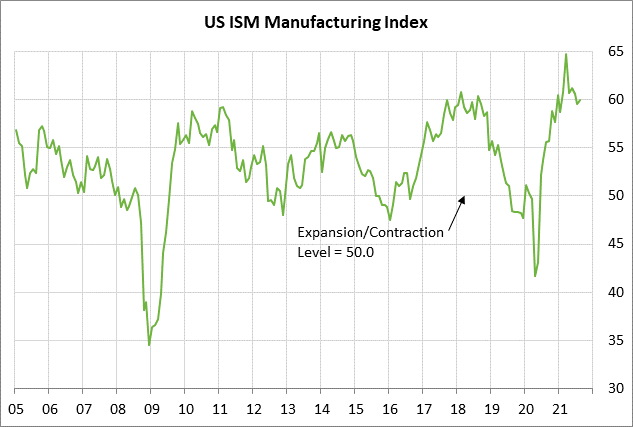

The ISM manufacturing index reached the euphoric 37-year high of 64.7 in March as pandemic infections fell and vaccinations became widely available. The ISM index has since fallen back due to manufacturing obstacles such as supply chain disruptions, transportation delays, and labor shortages. However, the ISM index in August was still very strong at 59.9, illustrating strong manufacturing confidence.