- Weekly market focus

- Senate returns to Washington as legislative crunch time arrives

- Fed’s quiet period begins ahead of next week’s FOMC meeting

- U.S. pandemic infections level off

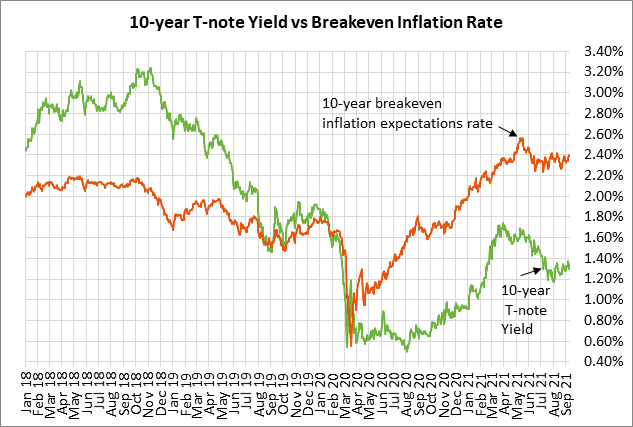

Weekly market focus — The U.S. markets this week will focus on (1) whether the U.S. Covid infection levels continue to decline, (2) whether the FOMC at its meeting next week will formally announce QE tapering, (3) the return of the Senate to session this week and the House next week as Congress needs to work on the continuing resolution, a debt ceiling hike, the $550 billion bipartisan infrastructure bill, and the Democrat’s $3.5 trillion spending bill, (4) the U.S. inflation situation with tomorrow’s release of the Aug CPI (expected +5.3% y/y headline and +4.2% y/y core), and (5) whether Friday’s early-Sep U.S. consumer sentiment index shows a recovery from August’s 10-year low.

Senate returns to Washington as legislative crunch time arrives — The Senate returns to session today, while the House returns next Monday. As Congress returns to Washington, they have a deluge of legislation to consider.

The first order of business will be to try to keep the government open when the new fiscal year begins on October 1. Congress has not passed spending bills for the new fiscal year and must therefore approve a continuing resolution to keep the government running past October 1. House Democratic leaders reportedly plan to bring a continuing resolution to the floor for a vote next week.

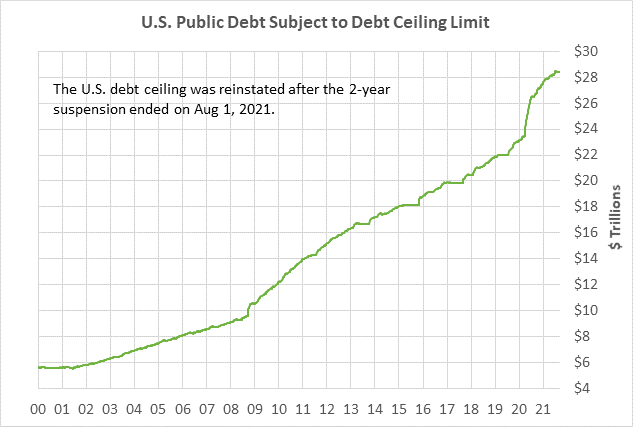

Congress has a little more time for a debt ceiling hike since the Congressional Budget Office has said that the Treasury will not hit its X-date until October or November. However, when the Treasury hits its X-date and is out of cash, the Treasury will no longer be able to meet all its financial obligations and the threat will arise of a sovereign debt default, which would be catastrophic.

Democrats may try to attach a debt ceiling hike to the continuing resolution, or they may bring it up as stand-alone legislation. Either way, Republicans have said they will oppose a debt ceiling hike, which raises the risks for the markets of a showdown and the risk of a Treasury default.

House Speaker Pelosi has given her committees a deadline of this Wednesday to produce the legislative language of the $3.5 trillion reconciliation bill that contains President Biden’s spending and taxation initiatives. Senate Majority Leader Schumer recently said that the Senate will move “full speed ahead” with a goal of approving a reconciliation bill by the end of September.

However, Democratic Senator Manchin on Sunday again voiced his opposition to the $3.5 trillion plan, saying he would support only a $1.5 trillion plan and that there is no hurry in trying to approve the bill by the end of September. It remains to be seen how Democratic leaders plan to placate Mr. Manchin and other moderate Democrats such as Arizona Senator Senema.

Meanwhile, House Speaker Pelosi promised her moderate wing that she will hold a vote on the $550 billion bipartisan infrastructure bill by September 27, which is now only two weeks away. Democrats seem unlikely to pass the exact same bill as the Senate since that would finalize Congressional approval and send it to President Biden for his signature.

Instead, the House is likely to either reject the bill for now or approve a different bill, thus allowing Ms. Pelosi to hold the infrastructure bill hostage to try to ensure that Senators Manchin and Senema and perhaps others eventually agree to some version of the Democrat’s $3.5 trillion reconciliation bill.

Fed’s quiet period begins ahead of next week’s FOMC meeting — The Fed’s quiet period has begun ahead of next week’s FOMC meeting on Tuesday and Wednesday. That means that the markets will not have any new Fed comments to chew on this week.

The markets are on guard for the possibility that the FOMC might officially announce its QE tapering as soon as next week’s meeting. However, the markets suspect the FOMC might defer that announcement to one of the following meetings on November 2-3 or December 14-15 due to the disappointing Aug payroll report of +235,000.

Despite the disappointing Aug payroll report and the uncertainty caused by the delta variant, the markets still believe that the FOMC will go ahead with QE tapering this year.

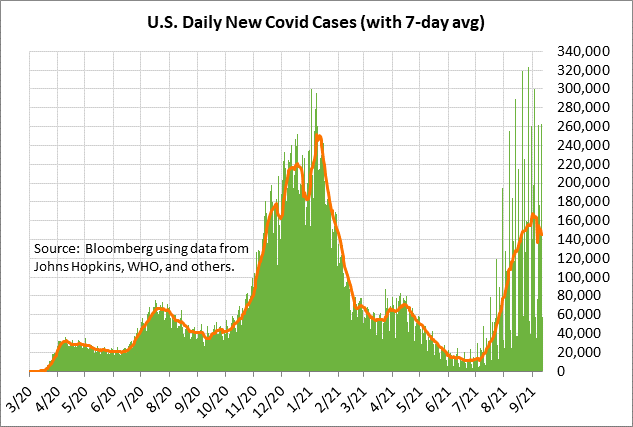

U.S. pandemic infections level off — The markets are hoping that the recent leveling-off of Covid infections means that the worst is past for the delta resurgence.

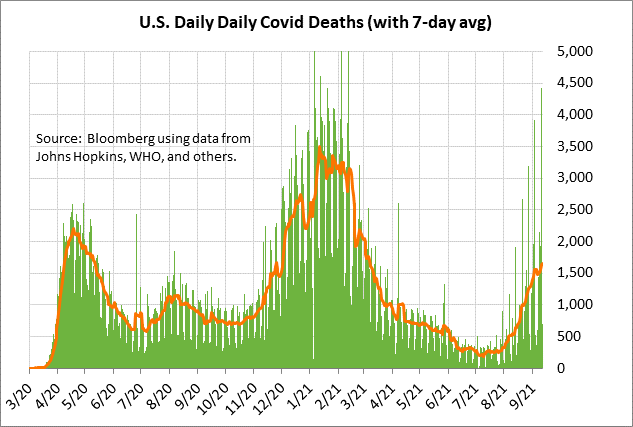

The 7-day average of daily new U.S. Covid infections on Saturday fell by a total of -14% to 144,928 from the 7-1/2 month high of 167,680 posted on September 1. However, the 7-day average of daily Covid deaths on Saturday rose to a 6-month high of 1,655 deaths.

The U.S. vaccination rate continues at a relatively strong pace, thus helping the U.S. get closer to herd immunity. Bloomberg reports that an average of 711,899 doses per day were administered over the past week, which is higher than the 500,000 area seen prior to the delta surge.

The CDC reports that 53.8% of the total U.S. population is now fully vaccinated and that 63.1% of the U.S. population has received at least one vaccination dose.