- U.S. PPI report expected to show continued strength in August inflation statistics

- Asian factory disruptions cause new problems for the global supply chain

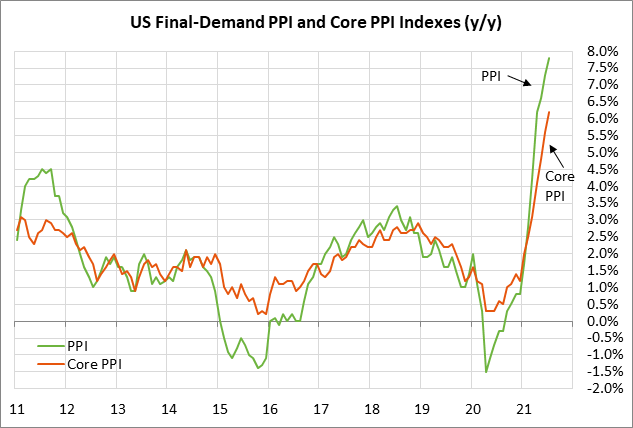

U.S. PPI report expected to show continued strength in August inflation statistics — The consensus is for today’s Aug final-demand PPI to show another sharp increase of +0.6% m/m and +8.2% y/y, following July’s report of +1.0% m/m an +7.8% y/y.

Meanwhile, the Aug PPI ex-food & energy is expected to increase by +0.6% m/m and +6.6% y/y, following July’s report of +1.0% m/m and +6.2% y/y.

The markets continue to take the current inflation surge in stride since they generally agree with the Fed that the surge is transitory. The Fed has argued that most of the surge in inflation has taken place in the sectors of the economy that have been most affected by the economic reopening and supply squeezes.

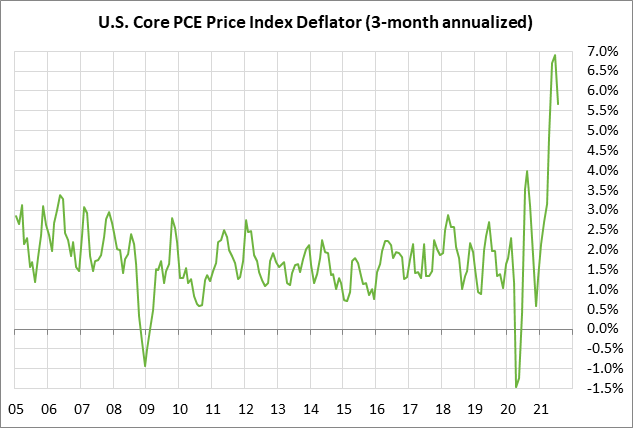

The FOMC in its latest macroeconomic forecasts, released after its June meeting, is forecasting that the PCE deflator will be elevated at +3.4% at the end of this year, but will then ease to +2.1% at the end of 2022 and 2.2% at the end of 2023. For the core PCE deflator, the FOMC is forecasting it will rise to +3.0% at the end of this year, but will then ease to +2.1% at the end of 2022 and remain at +2.1% at the end of 2023.

The FOMC’s official forecasts indicate that the Fed believes that inflation will return to its target by the end of next year. The Fed therefore believes that a policy response is not currently necessary to address the current inflation surge.

There was at least a little good news in the latest set of inflation statistics for July. On a 3-month annualized basis, the PCE deflator eased to +6.1% from June’s peak of +6.7% and the core PCE deflator eased to +5.7% from June’s peak of +6.9%.

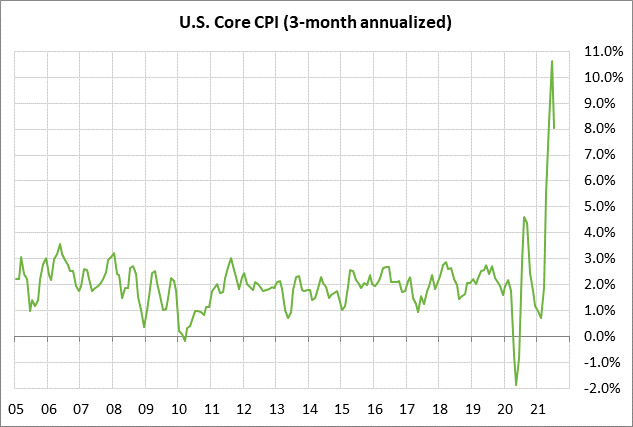

The CPI in July also eased on a 3-month annualized basis to +8.4% headline and +8.1% core from June’s peaks of +9.7% and +10.6%, respectively.

Asian factory disruptions cause new problems for the global supply chain — Manufacturing activity in Asia has begun to contract as the spread of the delta Covid variant in the region forced factories to halt or slow production.

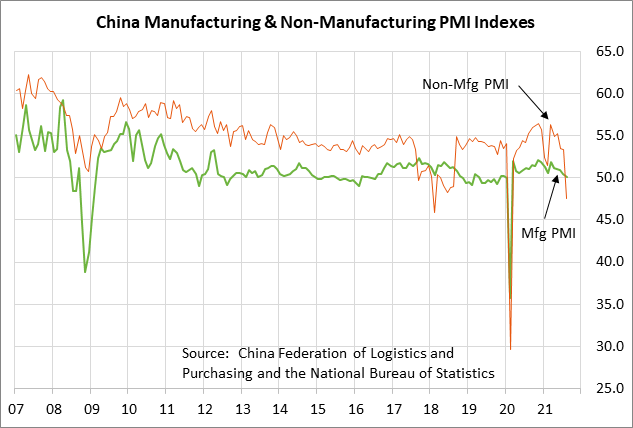

China’s national manufacturing PMI in August fell by -0.2 points to a 1-1/2 year low of 50.1, barely staying above the expansion-contraction level of 50.0. China’s manufacturing PMI has fallen for five consecutive months. The most recent decline has been due to the various shutdowns and restrictions that China imposed in reaction to the spread of the delta variant.

Elsewhere in Asia, Vietnam’s Aug IHS Markit PMI plunged by -4.9 points 40.2 from 45.1 in July, the third consecutive month of contraction and the lowest reading since the pandemic began. Also, Thailand’s Aug PMI fell by -0.4 points to 48.3 from 48.7 in July, the seventh month of contraction in the past eight months.

Manufacturing purchasing managers indexes for Indonesia, the Philippines, and Malaysia all remained deep in contraction territory in August, reflecting the disruption from pandemic lockdowns that slow factory output.

Southeast Asia’s under-vaccinated economies have seen record levels of Covid infections and deaths. Of 53 countries in a Bloomberg Covid Resilience Ranking, the bottom five are all in Southeast Asia. Those same five countries provide about 6% of global exports and supply crucial products to the world’s top economies, including half of U.S. semiconductor imports, according to estimates by Natixis.

The slowdown in factory production in Southeast Asia from the pandemic is further disrupting global supply chains. Companies worldwide are already struggling with sky-high shipping costs and a lack of containers to ship their goods. This does not bode well for the upcoming Christmas holiday season, a make-or-break time of year for many companies, as the supply chain disruptions will delay global shipments and prevent stores from filling their shelves.

The situation in Vietnam is set to worsen. The Vietnamese government last Tuesday extended stay-home orders and evening curfews in the major industrial provinces of Binh Duong and Dong Nai for an additional 15 days. Binh Duong and Dong Nai, home to multiple industrial parks used by global suppliers, have recently reported record Covid infections. This will undoubtedly further slow Vietnam’s factory output and snarl global supply chains.

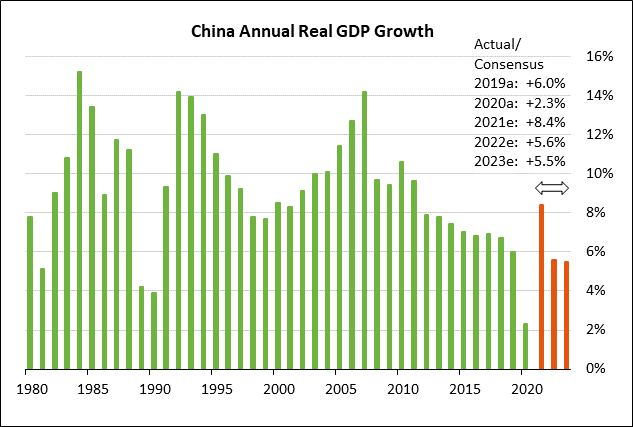

The recent shutdowns in China have caused a downward revision in expectations for Chinese GDP growth. China’s quarterly GDP peaked at +18.3% y/y in Q1-2021 but then decelerated to +7.9% y/y in Q2. The consensus is for GDP growth to ease to +5.6% in Q3 and +4.7% in Q4, which would be weaker than pre-pandemic levels.

On a calendar year basis, the consensus is for China’s GDP to recover sharply by +8.4% this year from the poor growth rate of +2.3% seen in 2020. However, China’s GDP is then expected to decelerate to +5.6% in 2022 and +5.5% in 2023.