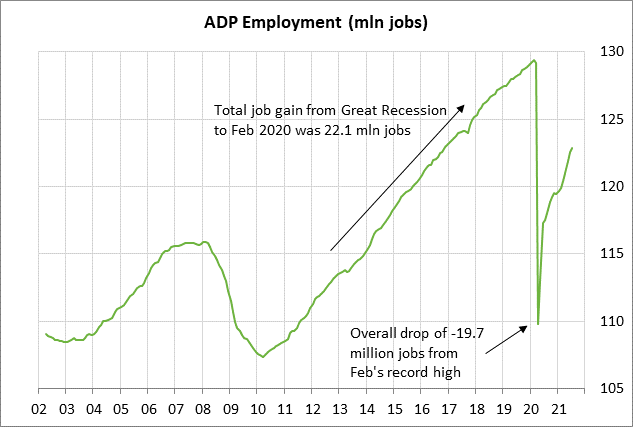

- Today’s U.S. ADP report will factor into the Fed’s QE tapering decision

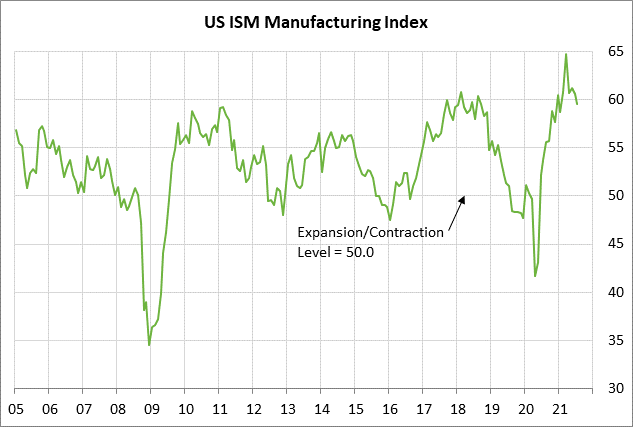

- U.S. ISM manufacturing index expected to decline but show continued strength

- U.S. Covid infections keep climbing

Today’s U.S. ADP report will factor into the Fed’s QE tapering decision — Today’s ADP report and Friday’s payroll report will be critical factors in the FOMC’s decision at its next meeting in three weeks (Sep 21-22) on whether they will announce QE tapering.

Strong labor market data for August could convince the FOMC that it is safe to go ahead with QE tapering even though the pandemic is still raging. By contrast, if the August labor market data is weak, then the FOMC may delay a tapering decision until its next meeting on Nov 2-3 as it waits to gauge the size of the hit to the U.S. economy from the pandemic’s resurgence.

The consensus is for today’s Aug ADP employment report to show a solid increase of +625,000. The ADP report in July showed a disappointing increase of 330,000, but that followed strength in the previous three months (i.e., +622,000 in April, +882,000 in May, and +680,000 in June).

Looking ahead to Friday’s August unemployment report, the consensus is for Aug payrolls to show a solid increase of +750,000. Payrolls have been very strong in the past three months, with a monthly average of +832,000 (May +614,000, June +938,000, July +943,000).

The markets will be watching to see whether businesses are pulling back on their hiring plans due to the pandemic’s resurgence, which has caused some businesses to delay plans to return to the office and institute mandatory vaccination rules. Increased pandemic restrictions are undercutting confidence in the restaurant, travel, and entertainment industries.

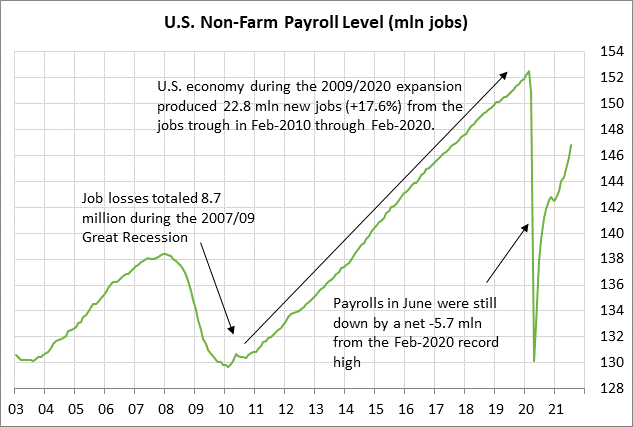

A pull-back in hiring would disrupt the Fed’s plans since the U.S. labor market still has a long way to go before returning to health. The U.S. economy must produce another 5.7 million jobs to get the payroll job level back up to the pre-pandemic record high seen in February 2020. ADP jobs still need to rise by another 6.5 million to reach their pre-pandemic record high.

The consensus is for Friday’s Aug unemployment rate to show a -0.2 point decline to 5.2%, adding to July’s sharp -0.5 point decline to a 16-month low of 5.4%. July’s drop in the unemployment rate to 5.4% was a welcome development since the unemployment rate is now only 1.9 points above the pre-pandemic record low of 3.5%.

However, the Fed knows that the unemployment rate will be increasingly difficult to push lower since more people are likely to come back into the labor market as jobs increase. The increased pool of available workers will put upward pressure on the unemployment rate.

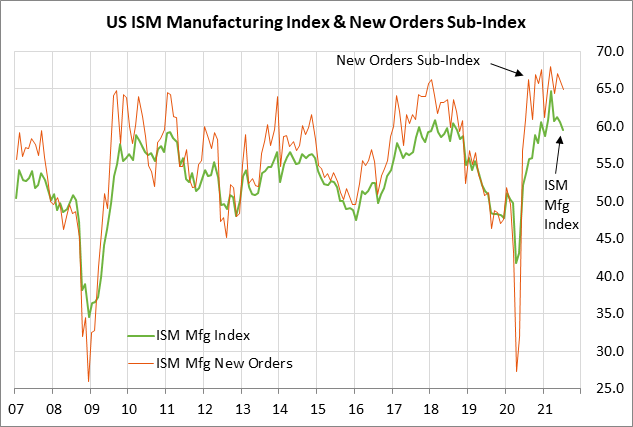

U.S. ISM manufacturing index expected to decline but show continued strength — The consensus is for today’s Aug ISM manufacturing index to show a -1.0 point decline to 58.5, adding to July’s -1.1 point decline to 59.5. The ISM manufacturing new orders sub-index in July fell by -1.1 points but remained very strong at 64.9, indicating a strong orders pipeline.

The fading level of manufacturing confidence is not surprising since confidence this past spring reached euphoric levels as vaccinations became widely available and the pandemic infection rates dropped sharply.

The decline in manufacturing confidence is being driven by various obstacles such as the pandemic’s resurgence and increased pandemic restrictions. The manufacturing sector is also facing a host of supply issues such as component shortages, the chip shortage, labor shortages, and shipping problems.

Despite these obstacles, today’s expected ISM index level of 58.5 would still be a strong level that indicates that U.S. executives remain optimistic about the prospects for the U.S. manufacturing sector. There is still a big pipeline of orders that need to be filled, and supply chain and shipping issues should gradually ease going into next year, allowing production to increase at an unencumbered rate.

Expectations for a decline in today’s ISM manufacturing index are based in part on the already-reported news that Markit’s U.S. manufacturing PMI in early August fell by -2.2 points to 61.2. That report will be revised today.

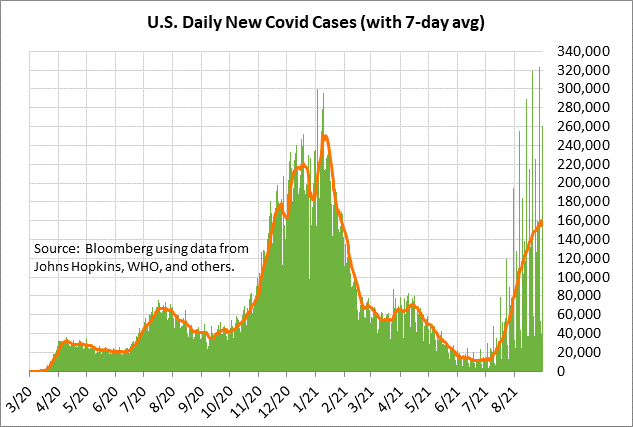

U.S. Covid infections keep climbing — The recent surge in Covid infections has yet to peak. The 7-day average of new U.S. Covid infections on Monday rose to a new 7-month high of 160,272. New daily U.S. Covid infections are now at nearly two-thirds of the record high of 251,085 posted in January.

On the brighter side, more people are gaining some immunity every day by getting vaccinations or by recovering from a Covid infection, thus bringing the U.S. closer to some semblance of herd immunity. Bloomberg reports that a daily average of 898,466 vaccine doses have been administered over the past week, which is much higher than the pre-delta level in the 500,000 area. The CDC reports that 52.4% of the total U.S. population is now fully vaccinated, while 61.8% have received at least one dose.