- Jackson Hole conference could bring Powell warning about QE taperingÂ

- Q2 GDP expected to be revised slightly higherÂ

- Initial unemployment claims expected to remain near last week’s 17-month low

- 7-year T-note auction to yield near 1.12%

Jackson Hole conference could bring Powell warning about QE tapering — The markets are on guard ahead of the Fed’s Jackson Hole conference that begins today due to the possibility that Fed Chair Powell may deliver an explicit warning that QE tapering is near. Mr. Powell will speak remotely at the conference at 10 AM ET Friday.

The Fed already delivered a tapering warning of sorts with last Wednesday’s release of the July 27-28 FOMC meeting minutes, which said that most participants “judged that it could be appropriate to start reducing the pace of asset purchases this year.”

However, there were “several” FOMC members who thought that QE tapering wouldn’t be appropriate until next year. Also, the macroeconomic situation since the July 27-28 FOMC meeting has deteriorated due to the pandemic’s resurgence, which means there might be less enthusiasm among FOMC members for near-term QE tapering.

The markets will therefore be waiting for Fed Chair Powell on Friday to give the Fed’s latest guidance about the expected timing of QE tapering. The markets won’t be shocked if Mr. Powell delivers a clear early warning about QE tapering. However, there is likely to be some disappointment since a significant number of market participants seem to be hoping that Mr. Powell on Friday will defer a warning and will continue his theme that it is still too early to taper QE due to uncertainties caused by the delta variant.

Despite such dovish hopes, the FOMC seems likely to officially announce QE tapering at either its next meeting on September 21-22 or at the following meeting on November 2-3. If Mr. Powell expects a QE tapering decision in just four weeks at the September meeting, then he may want to give an explicit warning this week, so the markets are not caught off-guard when that announcement is delivered. The Fed knows that it must clearly telegraph its intentions on QE tapering if it doesn’t want another taper tantrum, such as the one that occurred in 2013.

An obvious time for the Fed to actually start the QE tapering process would be January 1, 2022, thus allowing for adjustments to be based on calendar quarters. Some FOMC members have already said they want the QE tapering program to be finished by as soon as mid-2022.

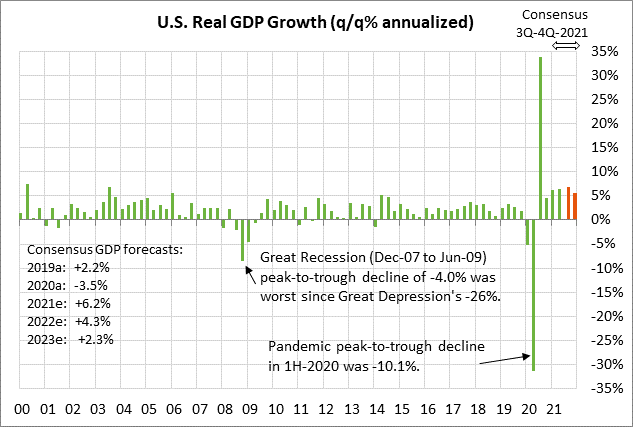

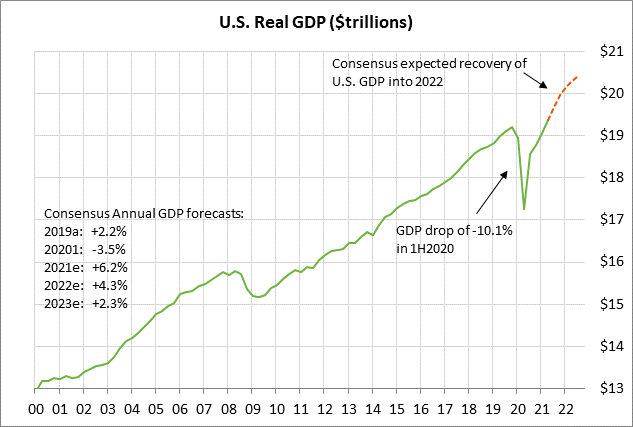

Q2 GDP expected to be revised slightly higher — The consensus is for today’s Q2 GDP to be revised slightly higher to +6.7% (q/q annualized) from the last estimate of +6.5%. The upward revision is expected to stem from the consensus that today’s Q2 personal consumption report will be revised higher to +12.2% from +11.8%.

The markets are mainly looking ahead to next month’s Q3 GDP report since the second quarter was already over almost two months ago. The consensus is for Q3 GDP to reach a new peak of +6.9%. However, the consensus is for GDP growth to then decelerate to +5.6% in Q4, +3.8% in Q1-2022, and +3.0% in Q2-2022.

On a calendar year basis, the consensus is for GDP growth in 2021 to rise by +6.2%, which would more than reverse the -3.5% decline seen in 2020. The expected 2021 GDP increase of +6.2% would be the strongest U.S. annual GDP report in 37 years, i.e., since the +7.2% increase seen in 1984.

After peaking this year at +6.2%, U.S. GDP is expected to remain strong at +4.3% in 2022, but then ease to a more normal level of +2.3% in 2023. U.S. GDP growth is expected to decelerate in 2022 and 2023 as fiscal stimulus and pent-up demand wears off. Also, the Fed is expected to start removing stimulus later this year with QE tapering and to start raising interest rates in 2023, thus cooling the economy.

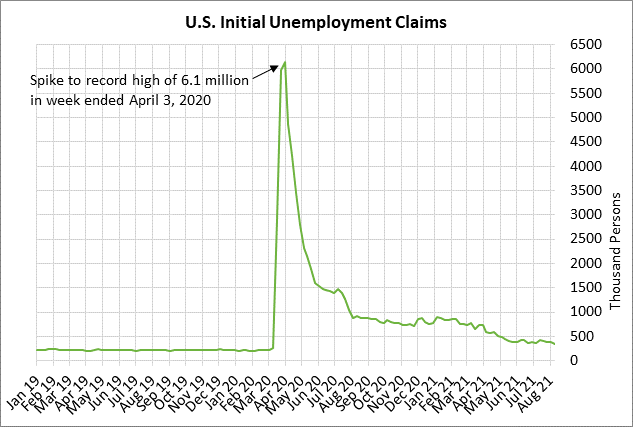

Initial unemployment claims expected to remain near last week’s 17-month low — The consensus is for today’s weekly initial unemployment claims report to show a small increase of +2,000 to 350,000, backsliding after last week’s -29,000 decline to 348,000. Meanwhile, today’s continuing claims report is expected to show a decline of -56,000 to 2.764 million, adding to last week’s -79,000 decline to 2.820 million.

The unemployment claims data remains in good shape with both initial and continuing claims last week falling to new 17-month lows. Relative to pre-pandemic levels, initial claims are elevated by only +132,000 and continuing claims are elevated by +1.112 million.

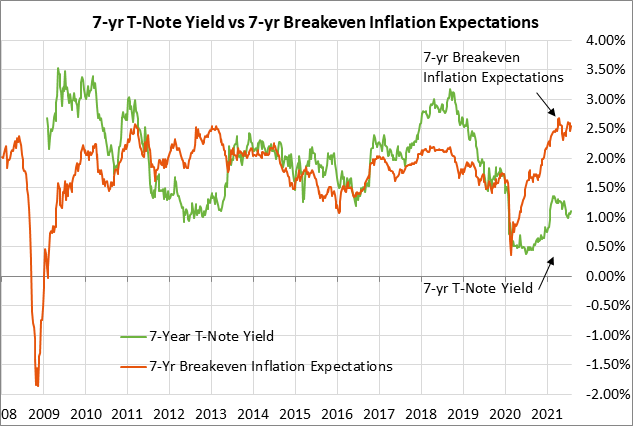

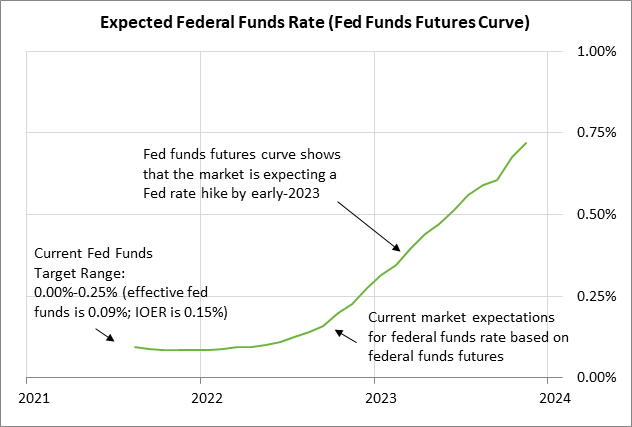

7-year T-note auction to yield near 1.12% — The Treasury today will sell $62 billion of 7-year T-notes, concluding this week’s $209 billion T-note package. The benchmark 7-year T-note yield yesterday closed at 1.12%, which is in the lower half of the range seen since March. The 7-year T-note yield continues to be suppressed by market expectations that the Fed will not implement its first rate hike until early 2023. The Treasury market today will be cautious since there have been some poor 7-year auctions in recent months.

The 12-auction averages for the 7-year are as follows: 2.31 bid cover ratio, $15 million in non-competitive bids, 5.9 bp tail to the median yield, 55.3 bp tail to the low yield, and 42% taken at the high yield. The 7-year T-note is the third-least popular security among foreign investors and central banks behind the 3-year and 2-year. Indirect bidders, a proxy for foreign buyers, have taken an average of 59.4% of the last twelve 7-year T-note auctions, which is moderately below the median of 62.2% for all recent Treasury coupon auctions.