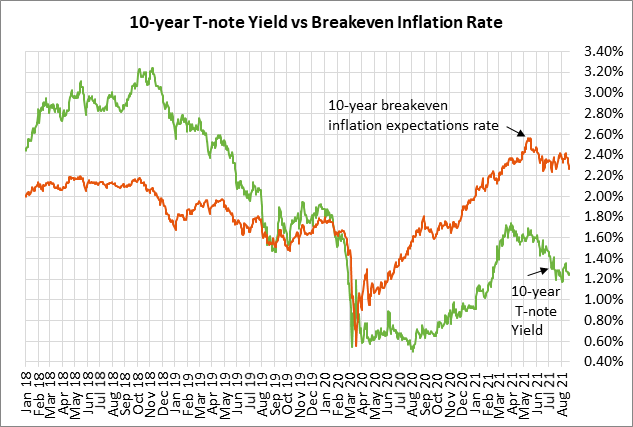

Weekly market focus — The U.S. markets this week will focus on (1) Fed Chair Powell’s comments Friday at the Jackson Hole conference where he may provide a stepped-up warning about QE tapering, (2) whether the U.S. pandemic statistics continue to worsen and the implications for the economy, (3) the Treasury’s sale of $209 billion of T-notes, (4) reports this week from 13 of the S&P 500 companies, and (5) a U.S. economic calendar that is focused on housing reports, Thursday’s Q2 GDP revision, and Friday’s PCE deflator report.

This week’s Jackson Hole conference could bring Powell warning about QE tapering — The markets are on guard ahead of the Fed’s Jackson Hole conference that begins this Thursday due to the possibility that Fed Chair Powell may deliver an explicit warning that QE tapering is near. Mr. Powell will speak remotely at the conference at 10 AM ET Friday.

The Fed already delivered a tapering warning of sorts after last Wednesday’s release of the July 27-28 FOMC meeting minutes said that most participants “judged that it could be appropriate to start reducing the pace of asset purchases this year.” However, there were “several” FOMC members who thought that QE tapering wouldn’t be appropriate until next year. Also, the macroeconomic situation since the July 27-28 FOMC meeting has deteriorated due to the pandemic’s resurgence, which means there might be less enthusiasm at the FOMC for near-term QE tapering.

The markets will therefore be waiting for Fed Chair Powell on Friday to give the Fed’s latest guidance about the expected timing of QE tapering.

In any case, there now seems to be a strong chance that the FOMC will officially announce QE tapering at either its next meeting on September 21-22 or at the following meeting on November 2-3. If Mr. Powell expects a QE tapering decision in just four weeks at the September meeting, then he may want to give an explicit warning this week, so the markets are not caught off-guard when that announcement is delivered. The Fed knows that it must clearly telegraph its intentions on QE tapering if it doesn’t want another taper tantrum, such as the one that occurred in 2013.

An obvious time for the Fed to actually start the QE tapering process would be January 1, 2022, thus allowing for adjustments to be based on calendar quarters. Some FOMC members have already said they want the QE tapering program to be finished by as soon as mid-2022.

House returns this week to vote on budget resolution — The House will temporarily return from its recess today to vote on the Democrat’s $3.5 trillion budget resolution, which the Senate approved before they left on their recess. The resolution is likely to pass, thus delivering the instructions to the various Congressional committees to write the legislation for Democrat’s reconciliation bill. That bill will contain the Democrat’s spending priorities, as well as tax increases on corporations and high-income taxpayers.

House Speaker Pelosi this week is also expected to hold a procedural vote on the $550 billion infrastructure bill. That procedural vote is an attempt to appease a handful of moderate Democratic House members who recently said they would not vote in favor of the budget resolution unless the House first approves the bipartisan infrastructure bill. Those moderate Democrats want passage of the infrastructure bill now so they can bring a win back to their districts this summer. It remains to be seen whether those moderate Democrats will be placated by only a procedural vote.

Ms. Pelosi has said all along that she will not allow an up-or-down vote on the infrastructure bill until after the Senate this autumn passes the reconciliation bill. Progressive Democrats are worried that the Senate might never pass the reconciliation bill if the House gives final approval of the infrastructure bill. The bulk of the Democratic caucus is therefore refusing to pass the infrastructure bill until the Senate first passes the reconciliation bill.

While the moderate Democrats this week might continue to raise a fuss, it seems likely that they will fall into line and that the Democratic-controlled House will pass the budget resolution this week. After the House is done voting this week, they will resume their recess and will not return to Washington until September 20.

When the House and Senate return to session in September, their first order of business will be to pass a continuing resolution to fund the federal government when the new fiscal year begins on October 1. Congress must also pass a debt ceiling hike by October or November before the Treasury reaches its X-date, runs out of cash, and starts defaulting on its financial obligations.

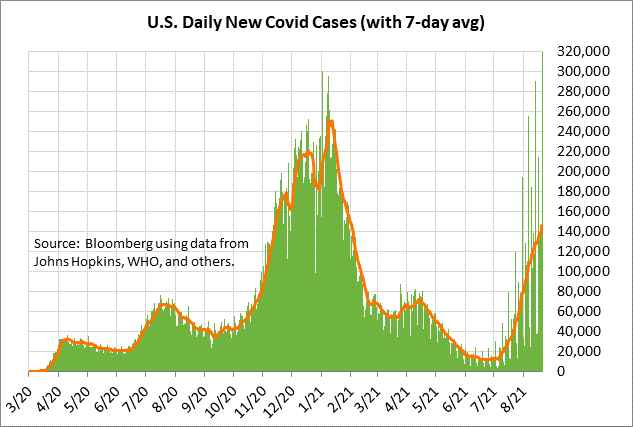

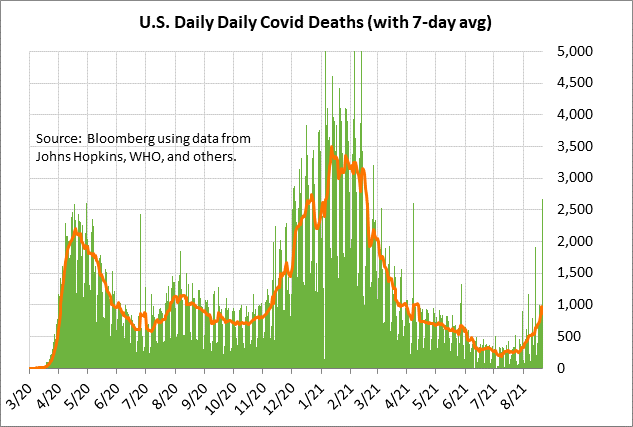

U.S. pandemic surge slows — New U.S. Covid infections are still rising, but at least at a slower rate. The 7-day average of new U.S. Covid infections last Friday rose to a new 6-1/2 month high of 145,284. The slower rate of new infections can be seen by the fact that last Friday’s average infection level was up by only 12.9% from the week earlier-level, which was a far slower week-on-week rise than recent levels of +30% and above.

Still, the daily infection rate has risen to more than half of January’s record high of 251,058, even though about half of the total U.S. population is fully vaccinated. That illustrates the dangerous transmissibility of the delta variant and the difficulty the U.S. is having bringing the pandemic under control. The CDC reports that 51.3% of the total U.S. population is now fully vaccinated and 60.5% have received at least one dose. Bloomberg reports that a daily average of 845,106 doses were given in the past week, up from previous levels near 500,000.