- Powell speaks today as market expectations firm up for timing of QE tapering

- U.S. retail sales expected to fade in July

- U.S. manufacturing production expected to show strength

- U.S. homebuilder confidence expected to remain strong

Powell speaks today as market expectations firm up for timing of QE tapering — Fed Chair Powell today will hold a virtual town hall with educators from across the country. Although the topic is education, Mr. Powell might still have something to say about the economy, the pandemic, or monetary policy.

On the Fed-policy front, the markets are looking ahead to tomorrow’s release of minutes of the July 27-28 FOMC meeting. The FOMC at that meeting took its “first deep dive” into discussing QE tapering, according to Mr. Powell. However, Mr. Powell said that the Fed still has “some ground to cover” before reaching the point of QE tapering.

The July FOMC meeting outcome did not seem to shift the market’s forecast of the timing of the Fed’s QE tapering. A Bloomberg poll taken on July 16-21 found that 74% of respondents expect the Fed to provide an early warning of QE tapering at next week’s (Aug 26-28) Jackson Hole conference or at the next FOMC meeting on September 21-22.

The survey found that 36% of the respondents expect the Fed to formally announce its QE program somewhere between September and November, while the largest plurality of 47% expect that announcement in December.

Regarding the actual implementation date, a hefty 71% of respondents expect the tapering to begin in Q1-2022. The remaining respondents were roughly split about whether the tapering will be either before or after Q1.

Boston Fed President Rosengren, in a CNBC interview yesterday, voiced an opinion that was a bit more hawkish on QE tapering than the consensus view. He said he expects there to be enough job growth to support a decision to formally announce QE tapering at the next FOMC meeting on September 21-22. He said he would support the implementation of the tapering beginning in October or November, and certainly not “any later than December.” He said he would want to conclude the tapering program by mid-2022.

A Wall Street Journal article on Monday also suggested that the Fed’s view on tapering is a bit more hawkish than the market consensus. The article said, “Federal Reserve officials are nearing agreement to begin scaling back their easy money policies in about three months if the economic recovery continues, with some pushing to end their asset-purchase program by the middle of next year.”

The concept of ending QE tapering by mid-2022 would leave the Fed the option of starting to raise interest rates in late 2022, if appropriate. Dallas Fed President Bullard recently said that he wants to start tapering QE in October and conclude the program by March. He said, “I don’t want to have to move too rapidly [to raise rates] because it can be very disruptive, so I think the pace I’m suggesting would give us a lot more optionality [on raising rates] in 2022 if we needed to use it.”

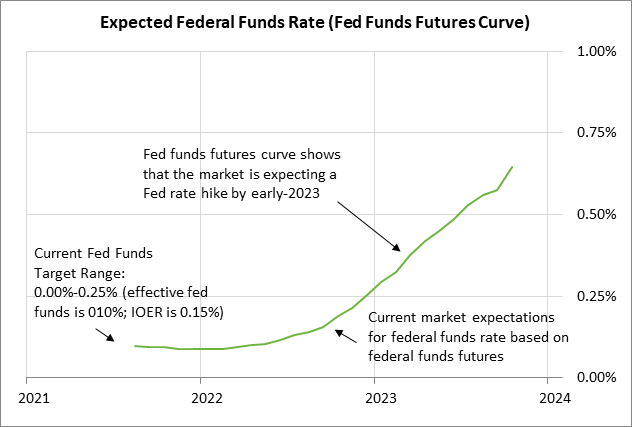

The market is not fully discounting the Fed’s first rate hike until early 2023, but that expectation could move forward to late 2022 if the U.S. economy continues to show unexpected strength.

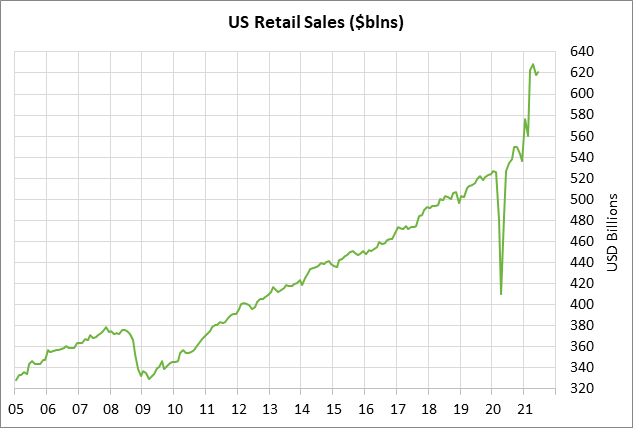

U.S. retail sales expected to fade in July — The consensus is for today’s July retail sales report to decelerate to -0.2% m/m and +0.2% m/m ex-autos from June’s strong report of +0.6% m/m and +1.3% ex-autos.

U.S. retail sales soared early this year due to (1) pent-up demand as the pandemic faded, and (2) two rounds of pandemic checks from the government. U.S. retail sales peaked at $628.8 billion in April 2021, which was 19% higher than the pre-pandemic level seen in January 2020. However, retail sales have since fallen by a net -1.1% from April’s peak since retail sales were at unsustainably high levels and since there aren’t going to be any more stimulus checks.

The markets are expecting consumers to trim their spending as they become more cautious about the resurgence of the pandemic. The markets were surprised by last Friday’s University of Michigan report that its August U.S. consumer sentiment index plunged by -11.0 points to a 9-3/4 year low, falling even below the previous pandemic low seen in April 2020.

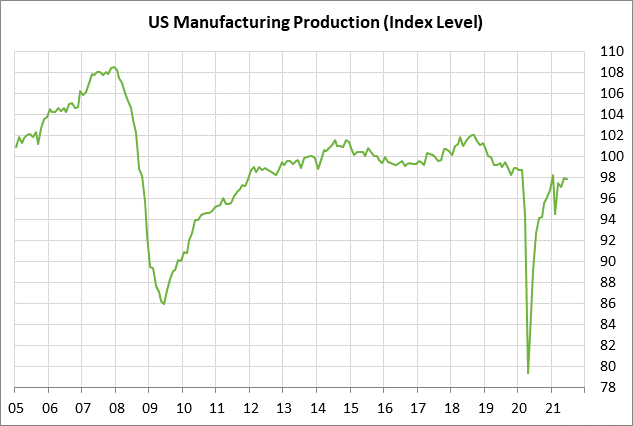

U.S. manufacturing production expected to show strength — The consensus is for today’s July manufacturing production report to show an increase of +0.7% m/m, returning to strength after June’s -0.1% decline. The broader July industrial production report is expected to show an increase of +0.5% m/m after June’s increase of +0.4%.

The U.S. manufacturing sector has a strong pipeline of orders to fill, but production has been hampered by the chip shortage, various supply chain disruptions, and reports of labor shortages. Production should be able to improve as businesses find ways to get around those obstacles.

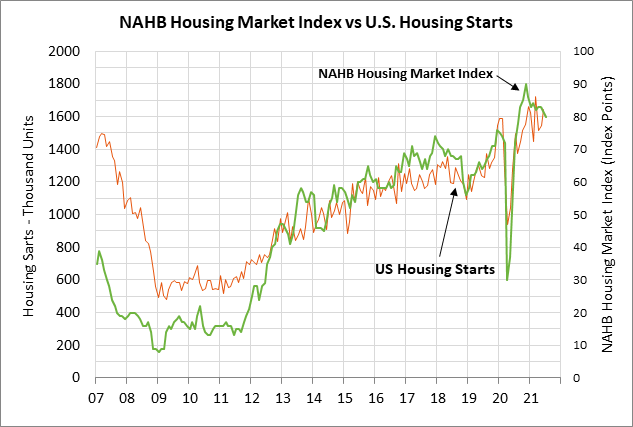

U.S. homebuilder confidence expected to remain strong — The consensus is for today’s Aug NAHB housing market index to be unchanged at 80 following July’s small decline of -1 to 80. The index has faded a bit from last November’s record high of 90. However, the index is still in very strong shape at 80, which is comfortably above the pre-pandemic level of 75 seen in January 2020.

U.S. homebuilder confidence remains solid due to strong demand for new homes, tight supplies, and low mortgage rates. New homes sales have fallen in recent months due to tight supplies and resistance to the sharp rise in new home prices. However, homebuilders remain optimistic about the outlook for the new home market.