- Weekly market focus

- House Democrats jockey on budget resolution

- U.S. pandemic worsens and global economic damage grows

- Q2 earnings season is winding down

Weekly market focus — The U.S. markets this week will focus on (1) whether the pandemic statistics continue to worsen, (2) Fed policy as Fed Chair Powell holds a town hall meeting on Tuesday, the July 27-28 FOMC meeting minutes are released on Wednesday, and next week’s Jackson Hole conference approaches, (3) whether Tuesday’s retail sales report indicates a cut-back in U.S. consumer spending, (4) the Treasury’s sale of 20-year T-bonds on Wednesday and 30-year TIPS on Thursday, and (5) earnings reports from 19 of the S&P 500 companies.

Overseas, the markets will be focused on (1) any new regulatory surprises from the Chinese government, (2) this week’s 4-day meeting of China’s top legislative body, and (3) reaction to the early-Monday Chinese industrial production and retail sales reports.

House Democrats jockey on budget resolution — The Senate last Wednesday left for its August recess after passing the $3.5 trillion budget resolution. The Senate doesn’t plan to return to Washington until September 13.

The action now shifts to the House where Democratic House members are jockeying over the budget resolution. The House will return to session next Monday and Tuesday (Aug 23-24) in an attempt to pass the budget resolution. Passage of the resolution would allow the Congressional committees to start writing the actual legislation for the budget reconciliation bill. After the House session next week, the House is scheduled to go back into recess and not return to Washington until September 20.

House Speaker Pelosi may have some difficulty getting the budget resolution passed next week after nine moderate Democrats last Friday issued a letter threatening to not vote for the budget resolution unless the House first passes the infrastructure bill. That would upset Ms. Pelosi’s plan for the House to hold a vote on the infrastructure bill only after the Senate has passed the $3.5 trillion reconciliation bill, which isn’t expected to happen until October or November.

Ms. Pelosi can only hope that the nine Democrats that signed the letter last Friday are engaged in some messaging to their voters back home and are not serious about voting against the budget resolution next week. Ms. Pelosi is also trying to satisfy the progressive wing of her party, who are refusing to vote on the infrastructure bill until the Senate has passed the reconciliation bill since they suspect the reconciliation bill might stall if they first pass the infrastructure bill.

When the House and Senate return to session in September, their first order of business will be to pass a continuing resolution to fund the federal government when the new fiscal year begins on October 1. Congress must also pass a debt ceiling hike by October or November before the Treasury reaches its X-date, runs out of cash, and starts defaulting on its financial obligations.

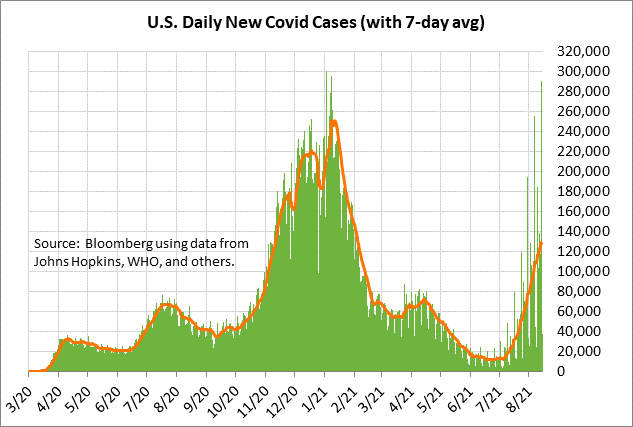

U.S. pandemic worsens and global economic damage grows — The U.S. pandemic has worsened sharply in the past two months and the economic fallout is starting. The University of Michigan last Friday reported that its August U.S. consumer sentiment index plunged by -11.0 points to a 9-3/4 year low, falling even below the previous pandemic low seen in April 2020. Consumers are clearly getting cold feet about the economy due to the pandemic surge and seem likely to be more cautious about their spending plans.

The 7-day average of new U.S. Covid infections continues to rise sharply and posted a new 6-1/4 month high on Wednesday of 122,649. In just the past six weeks, infections have risen by more than ten times from the 16-month low of 11,351 posted on June 23. The surge in Covid infections has now risen halfway to the record high of 250,464 posted earlier this year in mid-January.

The fact that the pandemic has surged to half its previous peak, even with about half of the U.S. population being vaccinated, illustrates the game-changing transmissibility of the delta variant.

The markets are also watching the economic fallout from China with its zero-tolerance approach to Covid. China last Thursday partially shut down about 25% of the world’s third busiest port of Ningbo-Zhoushan because a single worker tested positive for Covid. There will be some fallout for global shipping and corporate supply chains from the Chinese port shutdown.

China also halted flights in and out of Beijing. Data from aviation specialist OAG showed the number of seats being offered by Chinese carriers plunged -32% in one week and sent global carrier capacity down -6.5%.

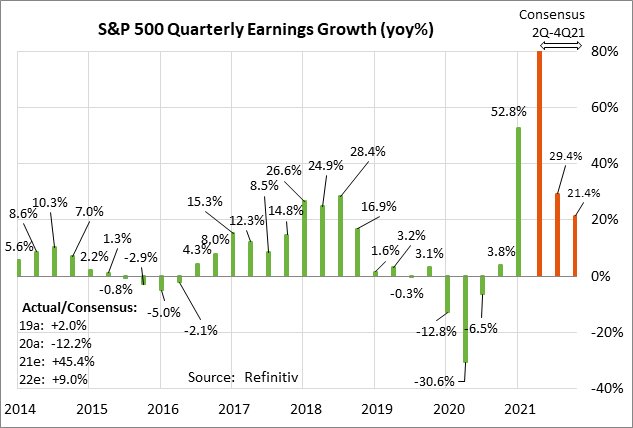

Q2 earnings season is winding down — Q2 earnings season is winding down with 457 of the S&P companies having already reported. There are earnings reports from 19 of the S&P companies this week, with notable reports including Walmart and Home Depot on Tuesday; Nvidia, Cisco, Target, Lowe’s, and TJX on Wednesday; Applied Materials and Ross Stores on Thursday. and Deere on Friday.

Q2 earnings season has been very strong, with 86.9% of the 457 reporting companies in the S&P 500 having beaten the market consensus, which is well above the long-term average of 65.5% and the 4-quarter average of 83.4%, according to Refinitiv. The consensus is for Q2 earnings growth of +93.8% y/y for the S&P 500 companies, which is much better than the consensus of +65.4% as of July 1. For all of 2021, the consensus is for earnings growth of +45.3%, more than recovering from the -12.2% decline seen in 2020.