- Congress will be quiet for 1-1/2 weeks until House returns to pass budget resolution

- July PPI expected to remain strong

- Unemployment claims expected to show continued labor market improvement

- 30-year T-note auction to yield near 1.37%

Congress will be quiet for 1-1/2 weeks until House returns to pass budget resolution — The Senate left Washington on Wednesday for its August recess after passing the $3.5 trillion budget resolution by a party-line vote of 50-49. The Senate is not planning to return to Washington until September 13.

The next Congressional event will be the return of the House to session on August 23-24 to pass the budget resolution. That will allow the Congressional committees to start writing the actual legislation for the budget reconciliation bill, which is due by September 15. The House schedule shows that the House plans to go back on recess after the August 23-24 session and not return to session until September 20. However, the House Committees are scheduled to start working again on August 31.

When the House and Senate return to session in September, their first order of business will be to pass a continuing resolution to fund the federal government when the new fiscal year begins on October 1. Congress must also pass a debt ceiling hike by October or November when the Treasury reaches its X-date, runs out of cash, and starts defaulting on its financial obligations.

The Senate this autumn is expected to pass the $3.5 trillion budget reconciliation bill with the Democrat’s spending priorities and tax hikes. After the Senate passes the reconciliation bill, House Speaker Pelosi has said both the bipartisan infrastructure bill and the reconciliation bill will get a vote in the House.

Democrats will face some obstacles in getting the reconciliation bill passed because they need the vote of every single Democratic Senator. However, Democratic Senators Manchin and Sinema on Wednesday again voiced their opposition to a spending bill as large at $3.5 trillion. An internal Democratic battle is expected between the progressive and moderate wings of the party on the ultimate size of the bill and its contents.

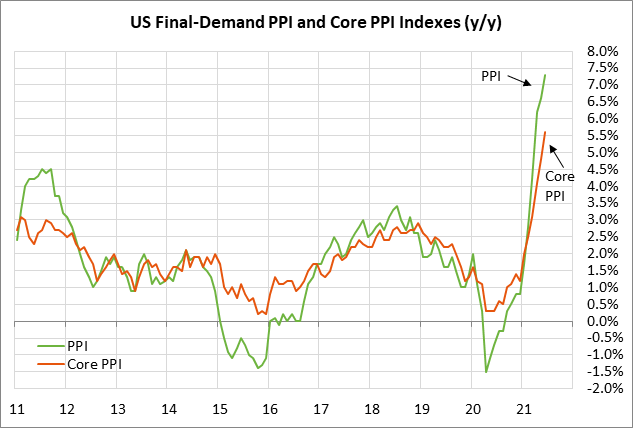

July PPI expected to remain strong — The consensus is for today’s July final-demand PPI to show increases of 0.6% m/m and +7.2% y/y, which would be less than June’s increases of +1.0% m/m and +7.3% y/y. Today’s July core PPI is expected to show increases of +0.5% m/m and +5.6% y/y versus June’s report of +1.0% m/m and +5.6% y/y.

The markets were generally pleased that yesterday’s July CPI was no worse than expectations and showed a little easing on a 3-month annualized basis. The July CPI rose by +0.5% m/m and +5.4% y/y, which was very close to expectations of +0.5% m/m and +5.3% y/y. The July core CPI rose by +0.3% m/m and +5.4% y/y, which was close to expectations of +0.4% m/m and +5.3% y/y.

On a 3-month annualized basis, the July CPI eased to +8.4% from June’s peak of +9.7%, and the July core CPI eased to +8.1% from June’s peak of +10.6%.

Despite the alarming inflation statistics seen recently, the markets continue to concur with the Fed that the current inflation surge is transitory. The Fed makes the case that much of the strength in the inflation statistics is in sectors linked to pandemic reopenings.

The Fed expects inflation to cool next year. The FOMC’s consensus forecast is that the core PCE deflator will ease to +2.1% by the end of 2022, down from the expected +3.0% level seen at the end of this year.

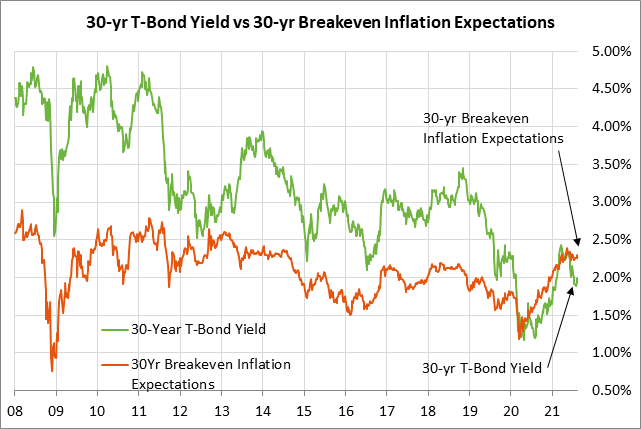

The market’s relaxed attitude to inflation can be seen in the 10-year breakeven inflation expectations rate, which measures the difference between 10-year T-note nominal and TIPS yields. The 10-year breakeven rate is currently at 2.40%, which is down by -19 bp from May’s 8-1/4 year high of 2.59%.

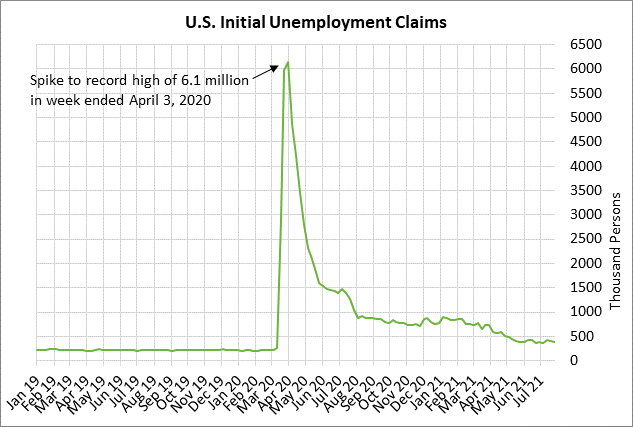

Unemployment claims expected to show continued labor market improvement — The consensus is for today’s weekly initial unemployment claims report to show a decline of -10,000 to 375,000, adding to last week’s decline of -14,000 to 385,000. Meanwhile, continuing claims are expected to fall -30,000 to 2.900 million, adding to last week’s plunge of -366,000 to a 1-1/2 year low of 2.930 million.

Initial claims are now only +169,000 above the pre-pandemic level. However, continuing claims are still 1.2 million above the pre-pandemic level.

The markets were pleased on the job front with last Friday’s strong July payroll report of +943,000, which was close to the +938,000 report seen in June. However, the question is whether job growth will soften over the next few months due to the spread of the delta variant and concerns about a negative impact on the economy.

30-year T-note auction to yield near 1.37% — The Treasury today will sell $27 billion of new 30-year T-bonds, concluding this week’s $126 billion quarterly refunding operation. Today’s 30-year T-bond issue was trading at 2.01% in when-issued trading late yesterday afternoon.

The 12-auction averages for the 30-year are as follows: 2.30 bid cover ratio, $6 million in non-competitive bids, 6.4 bp tail to the median yield, 76.8 bp tail to the low yield, and 48% taken at the high yield. The 30-year is mildly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.3% of the last twelve 30-year T-bond auctions, which is mildly above the median of 61.2% for all recent Treasury coupon auctions.