- House will return from its recess to vote on budget resolution

- July CPI expected to remain strong

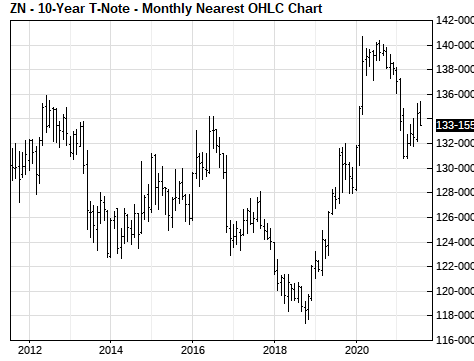

- 10-year T-note yield remains subdued despite strong economy and inflation

- 10-year T-note auction to yield near 1.37%

House will return from its recess to vote on budget resolution — House Majority Leader Hoyer on Tuesday announced that the House will come back into session on August 23 to vote on the budget resolution and take care of any other pressing business. The House has been on recess since July 30 and wasn’t planning to return to Washington until September 20.

The willingness of House Democratic leaders to interrupt their recess shows they are serious about moving the $3.5 trillion reconciliation bill forward as quickly as possible. As soon as both the Senate and House pass the budget resolution, then the various Committees can get busy writing the legislation that is outlined by the budget resolution.

Meanwhile, the Senate yesterday approved the $550 billion bipartisan infrastructure bill by the wide margin of 69-30. The bill will now go to the House. However, House Speaker Pelosi has said the infrastructure bill won’t get a vote in the House until the Senate also passes the $3.5 trillion reconciliation bill this autumn.

Immediately after passing the infrastructure bill, the Senate began considering the $3.5 trillion budget resolution, which contains the Democratic social spending priorities and tax hikes on corporations and wealthy taxpayers. The Senate began a vote-a-rama on amendments to the budget resolution, which was expected to last into the early morning hours of Wednesday. After passing the resolution, the Senate will leave for its August recess and is not planning to return to Washington until September 13.

The reconciliation bill will require all 50 Democratic Senators to vote in favor, but doesn’t need any Republican votes to pass. The stock market is carefully watching the reconciliation bill since Democrats plan to raise the corporate tax rate, which will reduce after-tax corporate profits and thus have a deleterious impact on stock prices.

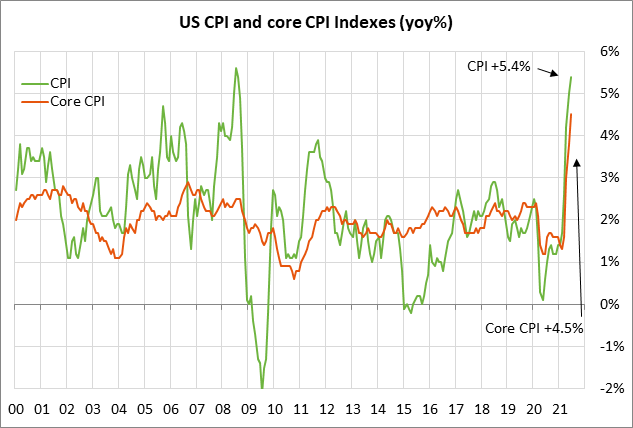

July CPI expected to remain strong — Today’s CPI report is expected to remain very strong as pandemic-related pressures continue to keep inflation high.

The consensus is for today’s July CPI to show increases of +0.5% m/m and +5.3% y/y, which would be a little cooler than June’s report of +0.9% m/m and +5.4% y/y. The July core CPI is also expected to remain strong with increases of +0.4% m/m and +4.3% y/y, down from June’s report of +0.9% m/m and +4.5% y/y.

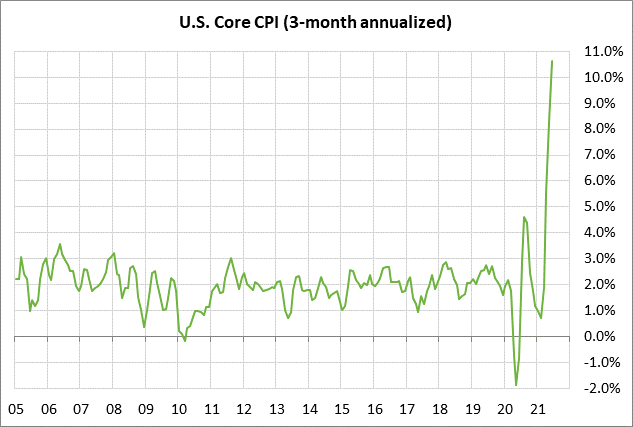

The strength in the CPI has been seen over the past several months and is not simply due to a low year-earlier base. On a 3-month annualized basis, the June CPI soared by 9.7% and the core CPI was even worse at +10.6%.

Despite the alarming inflation statistics, the markets continue to concur with the Fed that the current inflation surge is transitory. The Fed makes the case that much of the strength in the inflation statistics is in sectors linked to pandemic reopenings.

The Fed expects inflation to cool next year. The FOMC’s consensus forecast is that the core PCE deflator will ease to +2.1% by the end of 2022, down from the expected +3.0% level seen at the end of this year.

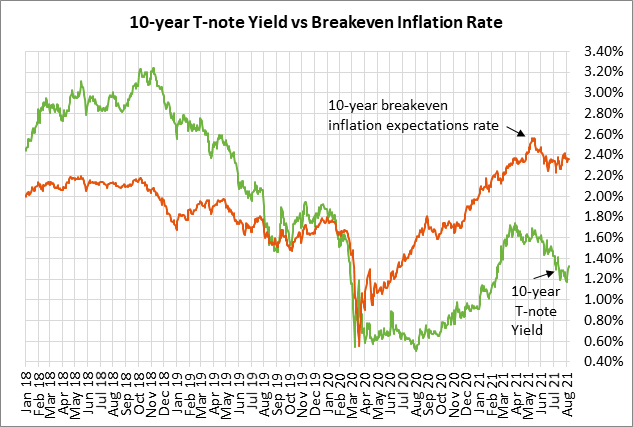

The market’s relaxed attitude to inflation can be seen in the 10-year breakeven inflation expectations rate, which measures the difference between 10-year T-note nominal and TIPS yields. The 10-year breakeven rate is currently at 2.39%, which is down by -20 bp from May’s 8-1/4 year high of 2.59%.

10-year T-note yield remains subdued despite strong economy and inflation — The 10-year T-note yield saw a sharp rise early this year due to the availability of vaccines and expectations for the global economy to make a strong come-back. However, the 10-year T-note yield peaked at a 1-1/2 year high of 1.77% in March and has since fallen by -42 bp to 1.35%.

The T-note yield has fallen back despite the fact that (1) U.S. GDP soared by +6.5% in Q2, and (2) the core PCE deflator rose by +6.7% in June on a 3-month annualized basis. In addition, the market is expecting the FOMC in the coming weeks to announce QE tapering and start cutting back on its bond purchases.

The T-note yield has fallen back because economic growth is expected to slip back to normal levels by next year. Also, the Fed is expected to keep its funds rate target near zero into early 2020. In addition, the delta Covid variant has hit many countries hard, including the U.S., and is causing a new obstacle for economic growth. New Covid infections in the U.S. are at a 6-month high and are showing no signs of slowing down.

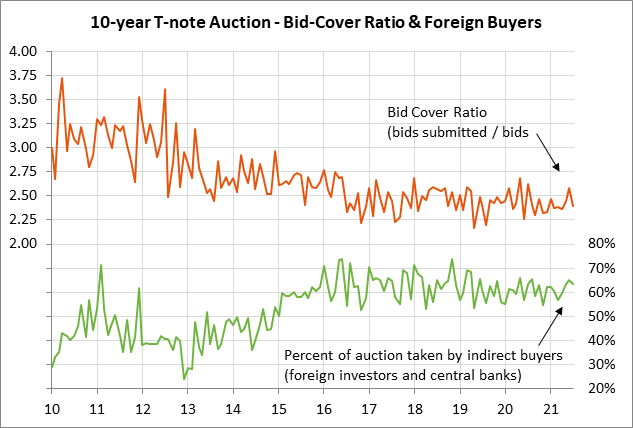

10-year T-note auction to yield near 1.37% — The Treasury today will sell $41 billion of new 10-year T-notes. The Treasury will then conclude this week’s $126 billion quarterly refunding operation by selling $27 billion of new 30-year T-bonds on Thursday. Today’s 10-year T-note issue was trading at 1.37% in when-issued trading late yesterday afternoon.

The 12-auction averages for the 10-year are as follows: 2.40 bid cover ratio, $17 million in non-competitive bids, 5.1 bp tail to the median yield, 69.4 bp tail to the low yield, and 50% taken at the high yield. The 10-year is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 61.2% of the last twelve 10-year T-note auctions, which matches the median for all recent Treasury coupon auctions.