- Weekly market focus

- Senate continues work on infrastructure bill and $3.5 trillion budget resolution

- Surge in U.S. Covid infections shows no sign of slowing down

- Q2 earnings season is winding down

Weekly market focus — The U.S. markets this week will focus on (1) whether the pandemic statistics continue to worsen, (2) Senate action on the infrastructure bill and budget resolution, (3) any further regulatory action by China that disrupts global stocks, (4) the tail-end of Q2 earnings season with reports from 14 of the S&P 500 companies, (5) the Treasury’s sale of 3, 10, and 30-year securities this week, and (6) this week’s U.S. economic calendar with the key report being Wednesday’s July CPI report (expected +5.3% y/y vs June’s +5.4%).

Senate continues work on infrastructure bill and $3.5 trillion budget resolution — The Senate over the weekend made slow progress on passing the $550 billion infrastructure bill, although passage is still expected by Tuesday. After passage, the bill will go to the House, although House Speaker Pelosi has said the infrastructure bill won’t get a vote in the House until the Senate also passes the $3.5 trillion reconciliation bill this autumn.

After passing the infrastructure bill, the Senate later this week will begin considering the $3.5 trillion budget resolution, which contains the Democratic spending priorities that aren’t already in the infrastructure bill. The Senate is expected to pass that bill by late this week and then leave for its August recess. The budget resolution contains the instructions for writing legislation to the Committees, which will proceed to write a reconciliation bill for the Senate to consider this autumn.

Meanwhile, the debt ceiling is gaining more market attention since Democrats have displayed no strategy for easy passage. Democrats have not included a debt ceiling hike in the budget resolution, presumably because (1) they don’t think they can pass the $3.5 trillion reconciliation bill this autumn before the Treasury reaches its X-date sometime in October or November, or (2) moderate Democratic Senators are refusing to support the budget resolution and reconciliation bill if they contain the debt ceiling hike, which exposes them to increased political attacks from Republican fiscal hawks.

Democrats could still add a debt ceiling hike to the reconciliation bill this autumn. However, the Democratic strategy at this point seems to be to add a debt ceiling hike to the continuing resolution that must be passed by October 1 to fund the federal government and prevent a shutdown when the new fiscal year begins.

Democrats seem to believe that Republicans in September will feel pressured into voting to keep the government open and raise the debt ceiling. However, Democrats have the Presidency and majorities in the House and Senate, which means that Democrats seem likely to suffer more political damage than Republicans if there is a government shutdown on October 1 or the risk of a Treasury default in October or November.

Republicans have plenty of leverage if Democrats want to pass a debt ceiling hike through anything other than a reconciliation bill since at least 10 Republicans would be needed to avoid a filibuster. Senate Minority Leader McConnell has already made it clear that Republicans plan to take full advantage of their leverage.

The bottom line is that there is a significant risk of a partisan showdown over the debt ceiling this autumn, with potential fall-out for the markets if a Treasury default becomes a real possibility.

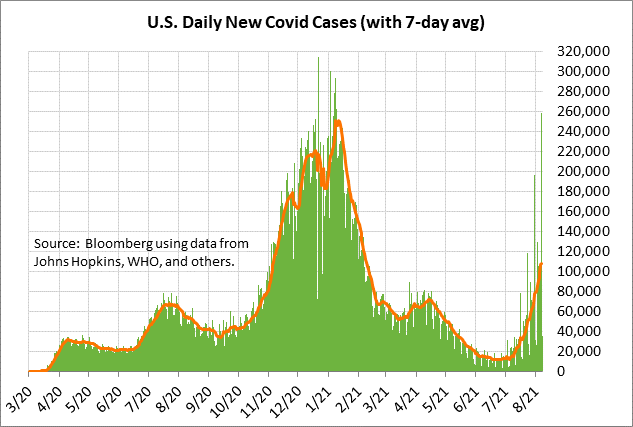

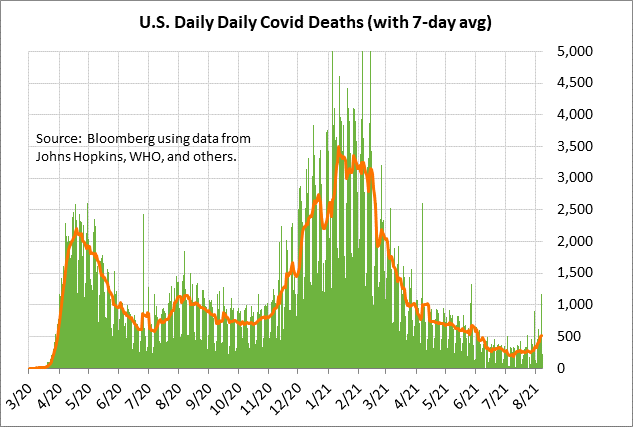

Surge in U.S. Covid infections shows no sign of slowing down — The 7-day average of new U.S. Covid infections continues to rise sharply and posted a new 6-month high on Saturday of 107,773. In just the past six weeks, infections have risen by nearly ten times from the 16-month low of 11,351 posted on June 23. The 7-day average of Covid deaths has risen to a 2-1/4 month high of 511 deaths, up from early-July’s 6-month low of 185 deaths.

The CDC reports that 50.1% of the total U.S. population has been fully vaccinated, and that 61.1% of the U.S. population over the age of 18 has been fully vaccinated. The CDC says that 58.7% of the total U.S. population has received at least one vaccination dose.

Bloomberg reports that a daily average of 712,389 vaccination doses have been administered in the past week. That is up from recent levels near +500,000 as the pandemic warnings and various vaccine mandates seem to be causing an increased interest in getting vaccinated.

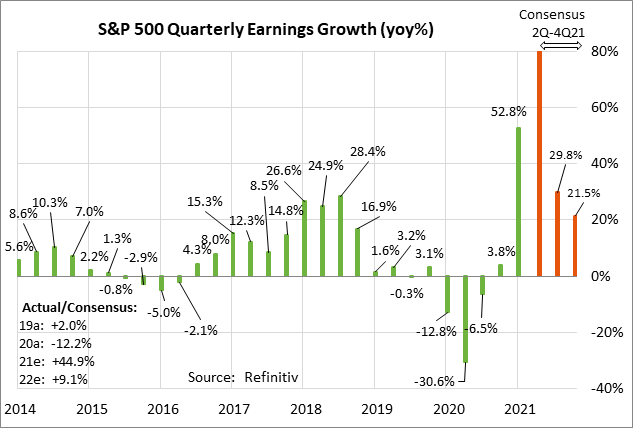

Q2 earnings season is winding down — Q2 earnings season has already seen its peak since 443 of the S&P companies have reported. There are earnings reports from 14 of the S&P companies this week. Notable earnings reports this week include Tyson Foods on Monday; Sysco on Tuesday; Ebay on Wednesday; and Walt Disney on Thursday.

Q2 earnings season has been very strong, with 87.4% of the 443 reporting companies in the S&P 500 having beaten the market consensus, which is well above the long-term average of 65.5% and the 4-quarter average of 83.4%, according to Refinitiv.

The consensus is for Q2 earnings growth of +93.1% y/y for the S&P 500 companies, which is much better than the consensus of +65.4% as of July 1. The year-on-year figure is, of course, inflated by the fact that earnings dropped sharply in Q2-2020 during the height of the pandemic economic shutdowns, causing a very low year-earlier base. For all of 2021, the consensus is for earnings growth of +44.9%, more than recovering from the -12.2% decline seen in 2020.