- Payroll report may indicate whether employers are pulling back due to pandemic resurgence

- Senate faces busy few days passing infrastructure bill and $3.5 trillion budget resolution

- Surge in U.S. Covid infections shows no sign of slowing down

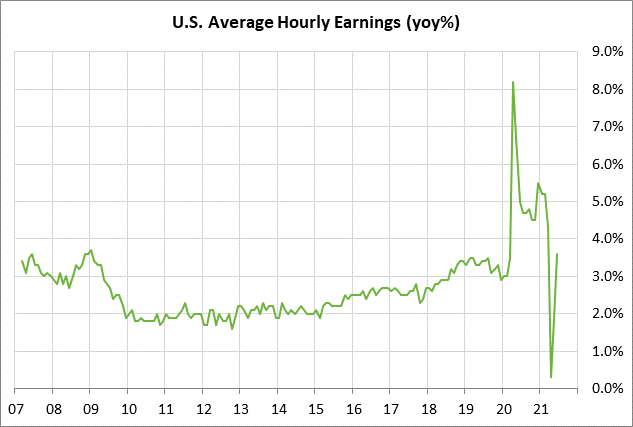

Payroll report may indicate whether employers are pulling back due to pandemic resurgence — The markets will be closely watching today’s July unemployment report to see if businesses are pulling back on their hiring plans due to the rapid spread of the delta variant among mostly unvaccinated people.

The markets will also be watching the extent to which labor market bottlenecks continue to plague the hiring process. The surge in the pandemic statistics may make an increasing number of people unwilling to go back to work in higher-risk jobs in sectors such as restaurants, travel, and entertainment, making it harder for businesses to find new employees.

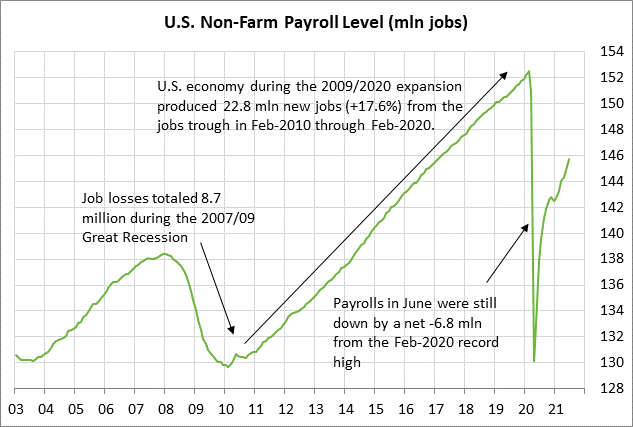

The consensus is for today’s July payroll report to show an increase of +875,000, which would be slightly stronger than June’s increase of +850,000 and the 3-month average of +717,000. Payrolls have risen by +15.6 million from last year’s pandemic trough but still need to rise by another +6.8 million to match the pre-pandemic record high posted in February 2020.

However, Wednesday’s ADP report was disappointing and undercut expectations for today’s payroll report. July ADP jobs rose by only +330,000, which was substantially weaker than expectations of +650,000.

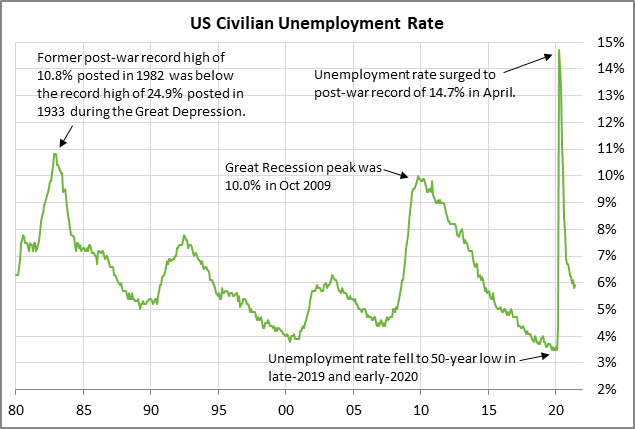

The consensus is for today’s July unemployment rate to show a -0.2 point decline to 5.7% after June’s small +0.1 point rise to 5.9%. The expected decline to 5.7% would be a new 16-month low, taking out the current low of 5.8% posted in May.

Senate faces busy few days passing infrastructure bill and $3.5 trillion budget resolution — The Senate is aiming to get the $550 billion infrastructure bill passed by early next week. Consideration of the bill has been slowed by the fact that many Senators are out of town today in Wyoming attending the funeral of former Senator Mike Enzi.

After the infrastructure bill is passed, the Senate will then proceed to the passage of the $3.5 trillion budget resolution, which contains the Democratic spending priorities that aren’t already in the infrastructure bill. Passage of the budget resolution is expected sometime next week.

The Senate was originally scheduled to leave today for its August recess. However, Senate Majority Leader Schumer said that the Senate will remain in session until it passes both the infrastructure bill and the budget resolution.

Meanwhile, the debt ceiling is gaining more market attention since Democrats have displayed no strategy for easy passage. Democrats have not included a debt ceiling hike in the budget resolution, presumably because (1) they don’t think they can pass the $3.5 trillion reconciliation bill this autumn before the Treasury reaches its X-date sometime in October or November, or (2) moderate Democratic Senators are refusing to support the budget resolution and reconciliation bill they contain the debt ceiling hike, which exposes them to increased political attacks from Republican fiscal hawks.

Democrats could still add a debt ceiling hike to the reconciliation bill this autumn. However, the Democratic strategy at this point seems to be to add a debt ceiling hike to the continuing resolution that must be passed by October 1 to fund the federal government and prevent a shutdown when the new fiscal year begins.

Democrats seem to believe that Republicans in September will feel pressured into voting to keep the government open and raise the debt ceiling. However, Democrats have the Presidency and majorities in the House and Senate, which means that Democrats seem likely to suffer more political damage than Republicans if there is a government shutdown on October 1 or the risk of a Treasury default in October or November.

Republicans have plenty of leverage if Democrats want to pass a debt ceiling hike through anything other than a reconciliation bill since at least 10 Republicans would be needed to avoid a filibuster. Senate Minority Leader McConnell has already made it clear that Republicans plan to take full advantage of their leverage.

The bottom line is that there is a significant risk of a partisan showdown over the debt ceiling this autumn, with potential fall-out for the markets if a Treasury default becomes a real possibility.

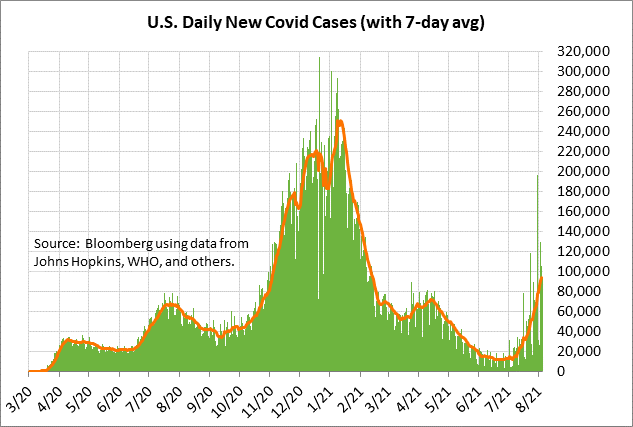

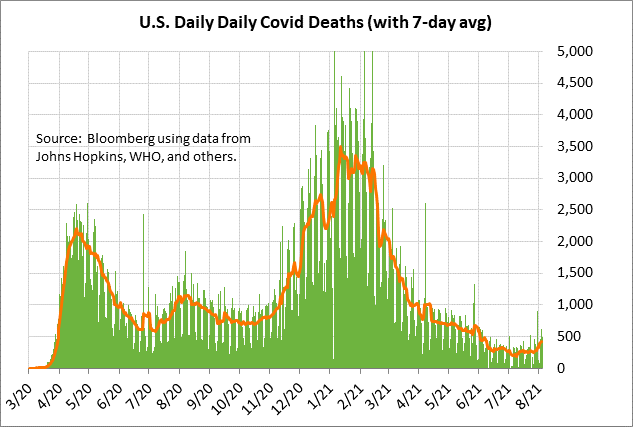

Surge in U.S. Covid infections shows no sign of slowing down — The 7-day average of new U.S. Covid infections continues to rise sharply and posted a new 5-3/4 month high on Wednesday of 93,998. In just the past six weeks, infections have risen by nearly nine times from the 16-month low of 11,351 posted on June 23. Covid deaths have also risen but not by as much as the overall infection level.

The CDC reports that 49.9% of the total U.S. population has been fully vaccinated, and that 60.8% of the U.S. population over the age of 18 has been fully vaccinated. The CDC says that 58.2% of the total U.S. population has received at least one vaccination dose.

Bloomberg reports that a daily average of 699,261 vaccination doses have been administered in the past week. That is up from recent levels near +500,000 as the pandemic warnings and various vaccine mandates seem to be causing an increased interest in getting vaccinated.