- Weekly global market focus

- Chinese PMI reports indicate slow easing in Chinese economy

- Senate faces test of passing both spending bills before August recess

- Rising U.S. Covid infection rate sparks worries about slower economic growth

- Q2 earnings season sees second busiest week

Weekly global market focus — The U.S. markets this week will focus on (1) the worsening global pandemic and the fall-out for the economy and the markets, (2) any further action by Chinese regulatory authorities against Chinese and U.S.-listed companies, (3) the Senate’s consideration of the $550 billion bipartisan infrastructure bill and the $3.5 trillion budget resolution, (4) this week’s busy Q2 earnings season with reports from 130 of the S&P 500 companies, (5) comments today by Fed Chair Powell at a virtual town hall with educators, and (6) key economic reports including today’s July ISM manufacturing index (expected +0.1 to 60.7) and Friday’s July payroll report (expected +900,000).

Chinese PMI reports indicate slow easing in Chinese economy — Last Friday night’s Chinese July PMI reports showed small declines as China’s post-pandemic economic surge fades. The Chinese July manufacturing PMI fell by -0.5 to 50.4, which was a larger decline than expectations of -0.1 point. The July non-manufacturing PMI fell by -0.2 point to 53.3, which was in line with market expectations. The consensus is for Chinese GDP to ease from +7.9% y/y in Q2 to +6.0% in Q3 and +5.0% in Q4. GDP growth is then expected to stabilize near +5.6% in 2022.

Senate faces test of passing both spending bills before August recess — The Senate is following a rocky road on trying to pass the $550 billion bipartisan infrastructure bill. The bill last Friday received a 66-34 vote to formally advance the legislation to debate, but the legislation then got bogged down over the weekend by a last-minute dispute over the exact language of the bill.

The Senate this week is expected to vote on amendments and then hold a final vote. Senate Majority Leader Schumer wants to win final approval of the bill by this Friday.

The Senate was originally scheduled to leave for their August this Friday. However, Senate Democratic leaders indicated that the Senate will delay their recess if necessary to get both the infrastructure bill and the $3.5 trillion Democratic budget resolution passed.

The House left for their August recess last Friday and is not scheduled to return until after Labor Day. Even if the Senate passes the infrastructure bill this week, House Speaker Pelosi has said the bill will not get a vote in the House until the Senate has also passed the $3.5 trillion budget resolution.

Meanwhile, the debt ceiling was reinstated yesterday (Aug 1), which means the U.S. government will no longer be able to borrow any net new amount of money that would push the U.S. national debt above the reinstated limit. The Treasury will be able to use its usual emergency measures to conserve its cash for some number of weeks. The CBO recently said that the Treasury may be able to last until October or November before hitting its X-date when it will run out of cash and will start defaulting on its financial obligations.

The Democrats need to find a way to get the debt ceiling raised, either with the cooperation of the Republicans or with the Democratic-only reconciliation bill if it is ready by the time the Treasury hits its X-date.

When Congress returns from its August recess after Labor Day, Democrats will also need to get a spending bill passed for the new fiscal year, or else there will be a partial government shutdown when the new fiscal year begins on October 1.

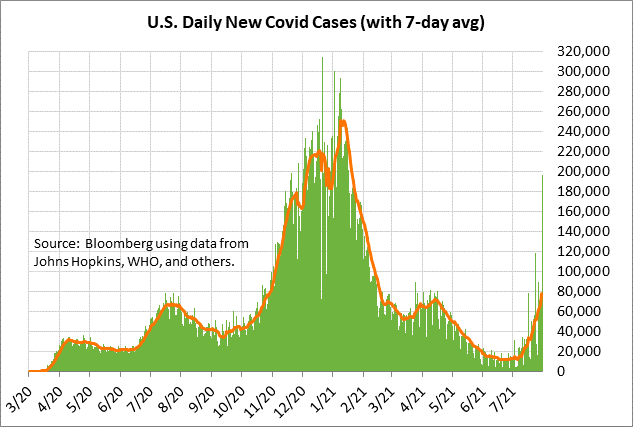

Rising U.S. Covid infection rate sparks worries about slower economic growth — The U.S. Covid infection rate continues to rise and cause market worries about weaker U.S. economic growth. U.S. Covid infections have surged in just the past month as the Delta variant sweeps the country. The 7-day average of new U.S. Covid infections last Friday rose to a new 5-1/2 month high of 77,796 cases, which is about seven times higher than the 16-month low of 11,351 posted just a month ago on June 23.

The CDC reports that 49.5% of the U.S. population is now fully vaccinated, and 57.4% have received at least one dose. Bloomberg reports that the U.S. has administered a daily average of 652,085 vaccination doses over the past week, which is a little higher than recent weeks as warnings about the Delta variant appear to be sparking increased interest in getting vaccinated.

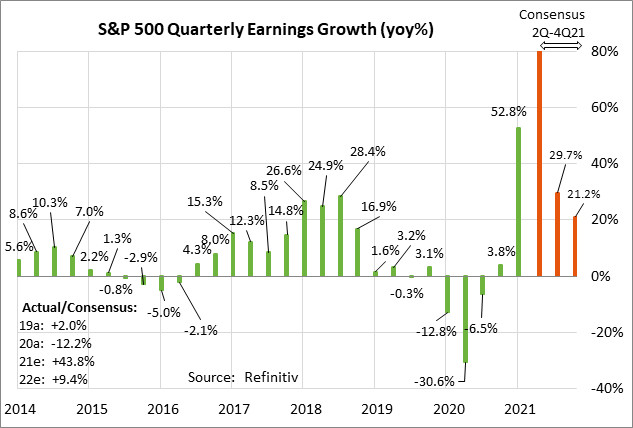

Q2 earnings season sees second busiest week — Q2 earnings season saw its peak last week but will still be busy this week with reports from 130 of the S&P 500 companies. Notable earnings reports this week include: Under Armour on Tuesday; Activision Blizzard on Tuesday; GM, Electronic Arts, and Royal Caribbean Cruises on Wednesday; Moderna and Expedia on Thursday; and Norwegian Cruise Line Holdings and Berkshire Hathaway on Friday.

Q2 earnings season has been very strong, with 88.5% of the 296 reporting companies in the S&P 500 having beaten the market consensus, which is well above the long-term average of 65.5% and the 4-quarter average of 83.4%, according to Refinitiv.

The consensus is for Q2 earnings growth of +89.8% y/y for the S&P 500 companies, which is much better than the consensus of +65.4% as of July 1. The year-on-year figure is, of course, inflated by the fact that earnings dropped sharply in Q2-2020 during the height of the pandemic economic shutdowns, causing a very low year-earlier base. For all of 2021, the consensus is for earnings growth of +43.8%, more than recovering from the -12.2% decline seen in 2020.