- June U.S. deflator expected to show the same large increases seen for the June CPI and PPI reports

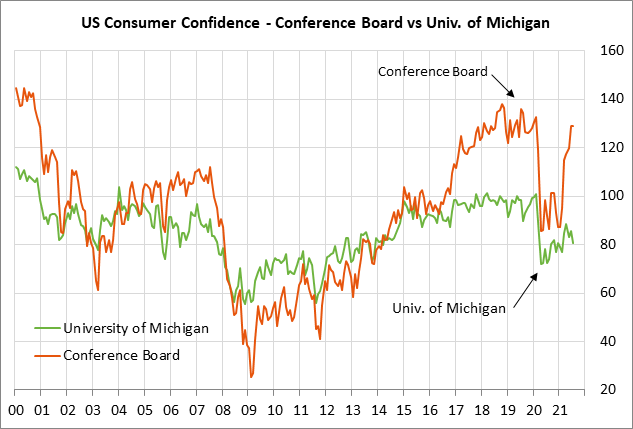

- U.S. consumer sentiment expected to be unchanged after early-July decline

- Senate faces test of passing both spending bills next week

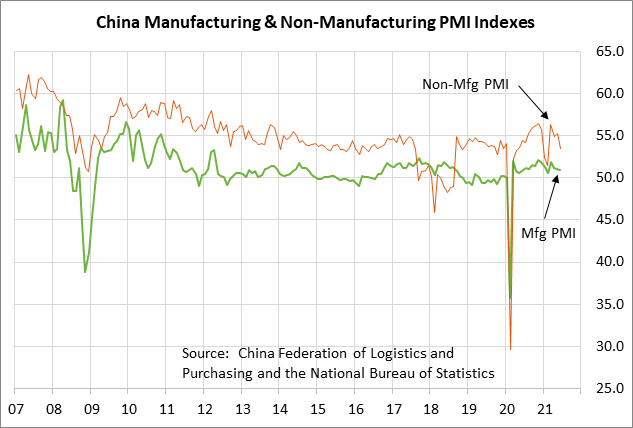

- Chinese PMI reports expected to show small declines

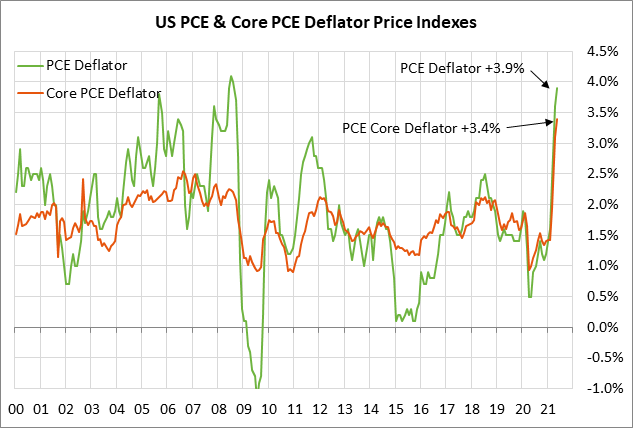

June U.S. deflator expected to show the same large increases seen for the June CPI and PPI reports — The consensus is for today’s June PCE deflator to show a strong increase of +0.6% m/m, adding to May’s increase of +0.4% m/m. The June core PCE deflator is also expected to show an increase of +0.6% m/m, adding to May’s +0.5% increase.

On a year-on-year basis, the headline deflator is expected to edge higher to +4.0% from May’s +3.9%, while the core deflator is expected to rise to +3.7% from May’s +3.4%.

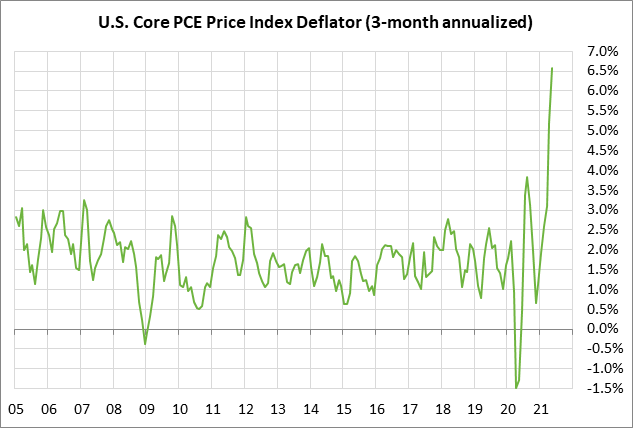

Inflation in recent months has risen sharply, with the 3-month annualized deflator in May up +6.8% and the core deflator up +6.6%. The CPI data for June, which has already been released, was even stronger, with a headline increase of +9.7% on a 3-month annualized basis and a core increase of +10.6%.

The Fed has so far convinced the markets that the current inflation surge is transitory since it is being caused mainly by reopening pressures that should subside by next year. The markets are therefore likely to take today’s June PCE deflator data in stride, as they did the already-reported June CPI and PPI data.

Market expectations for inflation have increased in the past two weeks, but remain comfortably below the peak seen in May. Specifically, the 10-year breakeven inflation expectations rate has risen by 20 bp since last week to 2.41%, but remains 18 bp below the 8-1/4 year high of 2.59% posted in May.

U.S. consumer sentiment expected to be unchanged after early-July decline — The consensus is for today’s final-July University of Michigan U.S. consumer sentiment index to be unchanged from the early-July report of 80.8, which would leave the index down by -4.7 points from June.

U.S. consumer sentiment fell in early July as consumers worried about the resurgence of the pandemic and whether there will be new shutdowns and layoffs. Also, consumers are being hit with higher gasoline costs since average national price of regular gasoline is currently at a 6-3/4 year high of $3.17 per gallon.

Senate faces test of passing both spending bills next week — Senate Majority Leader Schumer says he has the votes to pass both the $550 billion bipartisan infrastructure bill and the Democrat’s $3.5 trillion budget resolution. Mr. Schumer says he will to get both bills passed before the Senate leaves for its recess next Friday (Aug 6).

The Senate earlier this week approved a cloture motion to send the $550 billion infrastructure bill to the Senate floor for debate. The Senate passed the cloture motion by the wide margin of 67-32, with 17 Republicans voting in favor. The good news is that Mr. Schumer now needs only 50 votes (plus Vice President Harris) to win the final approval of the bill, which means he can afford to lose some Democratic and Republican votes for the final bill. The bad news is that even if the Senate passes the bill, House Speaker Pelosi has said the bill won’t get a vote in the House until the Senate also passes a $3.5 trillion reconciliation bill, which isn’t likely to happen until this autumn.

Mr. Schumer has said he also has the votes to pass the $3.5 trillion budget resolution. He needs every one of the 50 Democratic Senators to vote in favor since no Republicans plan to support the signature Democratic spending bill. Even though some Democratic Senators such as Sinema, Manchin, and Tester are expressing doubts about the size of the bill, they are expected to vote next week to at least approve the budget resolution to get the ball rolling to write the final reconciliation bill.

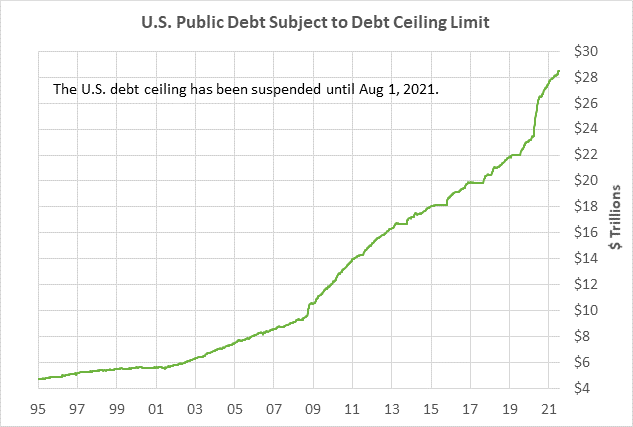

Meanwhile, the debt ceiling will be reinstated on Sunday at the current level of the U.S. debt, which means the U.S. government will no longer be able to borrow any net new amount of money that would push the U.S. national debt above the new limit. The Treasury will be able to conserve its cash with its usual emergency measures for some number of weeks. The CBO recently said that the Treasury may be able to last until October or November before hitting its X-date when it will run out of cash and will start defaulting on its financial obligations.

The Democrats need to find a way to get the debt ceiling raised, either with the cooperation of the Republicans or with the Democratic-only reconciliation bill if it is ready by the time the Treasury hits its X-date.

When Congress returns from its August recess after Labor Day, Democrats will also need to get a spending bill passed for the new fiscal year or else there will be a partial government shutdown when the new fiscal year begins on October 1.

Chinese PMI reports expected to show small declines — The consensus is for tonight’s Chinese July PMI reports to show small declines as China’s post-pandemic economic surge fades. The consensus is for today’s Chinese July manufacturing PMI to show a small -0.1 point decline to 50.8, adding to June’s -0.1 point decline to 50.9. Today’s July non-manufacturing PMI is expected to show a decline of -0.2 points to 53.3, adding to June’s large -1.7 point decline to 53.5.

Despite the mildly lower PMI reports, the Chinese economy is so far holding its own with steady growth. The consensus is for Chinese GDP to ease from +7.9% y/y in Q2 to +6.0% in Q3 and +5.0% in Q4. GDP growth is then expected to stabilize near +5.6% in 2022.