- U.S. CPI expected to show another strong monthly increase but Fed still insists inflation surge is transitory

- 30-year T-bond auction to yield near 2.00%Â

- U.S. pandemic statistics surge due to Delta variant

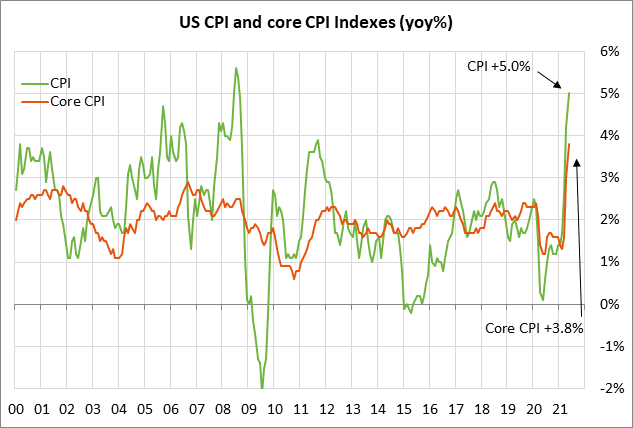

U.S. CPI expected to show another strong monthly increase but Fed still insists inflation surge is transitory — The consensus for today’s June CPI report is for another strong increase of +0.5% m/m and +4.9% y/y, which would be just slightly below May’s report of +0.6% m/m and +5.0% y/y.

The June core CPI is expected to show another strong monthly increase of +0.4% m/m, adding to May’s +0.7% m/m increase. On a year-on-year basis, the June core CPI is expected to edge higher to +4.0% y/y from May’s +3.8%.

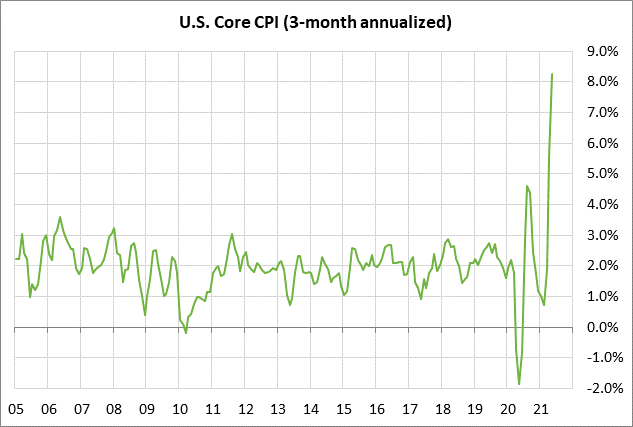

The year-on-year CPI figures are currently of little use due to the low year-earlier base caused by the pandemic shutdowns. However, the CPI data shows that inflation has been surging in recent months. On a 3-month annualized basis, the CPI in June rose by an extraordinary +8.4%, and the core CPI rose by +8.3%.

Today’s consensus for the June CPI reports would produce new 3-month annualized figures of +7.9% for the headline CPI and +8.5% for the core CPI.

The debate continues about whether the current surge in inflation will be transitory or persistent. Fed officials continue to insist that the surge will be transitory. Just yesterday, Richmond Fed President Barkin said that inflation could cool more than expected and that the U.S. labor market “hasn’t healed enough” for the Fed to taper bond buying.

The markets are also starting to come around to the idea that the surge in inflation will be transitory. One argument is that the supply disruptions that recently pushed prices higher are already starting to ease. Sep lumber prices, for example, completely reversed the +121% upward spike seen in March-April and are back to where they were in early March.

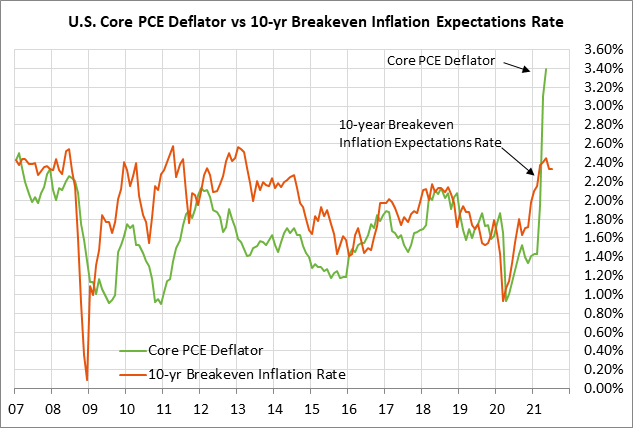

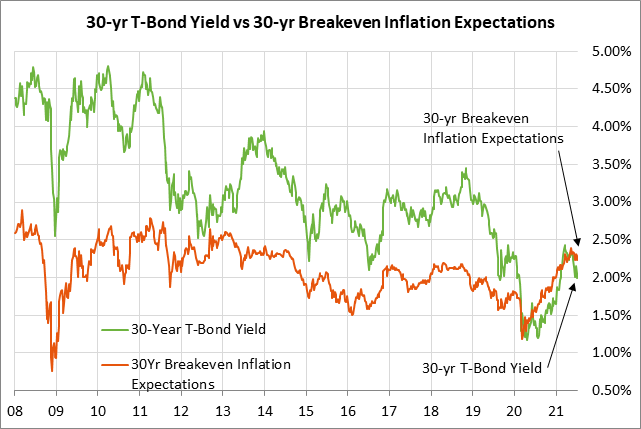

Inflation expectations have also eased in the past two months. The 10-year breakeven inflation expectations rate is currently at 2.33%, down by -26 bp from the 8-1/4 year high of 2.59% posted in mid-May. However, it is notable that the 10-year breakeven rate is still well above the Fed’s inflation target of 2.0%.

30-year T-bond auction to yield near 2.00% — The Treasury today will sell $24 billion of 30-year bonds, capping this week’s sale of 3-year, 10-year, and 30-year securities. Demand was respectable for yesterday’s 3-year and 10-year auctions. Today’s 30-year auction will be the second and final reopening of the 2-3/8% 30-year bond of May 205, which the Treasury first sold in May.

The 30-year bond yield yesterday closed at 2.00%, which is just mildly above last Thursday’s 5-1/4 month low of 1.86%. The 30-year T-bond yield has been falling over the past two months, along with the rest of the longer end of the Treasury curve. The Treasury market seems to be discounting weaker economic growth in the coming months as the post-pandemic surge fades and fiscal stimulus wears off.

The Treasury market also does not seem to be worried about the Fed’s QE tapering, which is expected to arrive by the end of the year. The markets are generally expecting an early warning on QE tapering at the August Jackson Hole conference or at the September 21-22 FOMC meeting, with the official announcement following a month or two later.

The markets are not expecting a QE tapering warning as soon as the next FOMC meeting in two weeks on July 27-28. Fed officials at present are still downplaying QE tapering as they try to prevent a taper tantrum.

The 12-auction averages for the 30-year are as follows: 2.33 bid cover ratio, $6 million in non-competitive bids, 5.9 bp tail to the median yield, 79.4 bp tail to the low yield, and 48% taken at the high yield. The 30-year is a popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.2% of the last twelve 30-year bond auctions, which is moderately above the median of 61.2% for all recent Treasury coupon auctions.

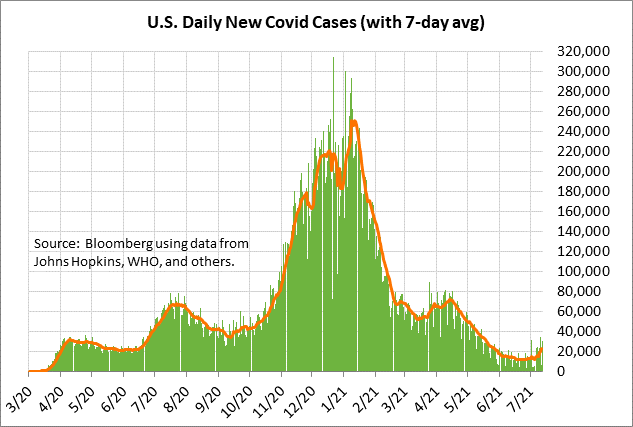

U.S. pandemic statistics surge due to Delta variant — The U.S. Covid infection rate is surging due to the spread of the highly-transmissible Delta variant, which now accounts for more than half of all new U.S. cases. The 7-day average of new U.S. Covid infections on Monday surged to a 1-1/2 month high of 22,961, doubling from the 15-1/2 month low of 11,351 posted only three weeks ago on June 23.

The spread of the Delta variant is taking root due to the slower speed of vaccinations. The CDC reports that 48% of the U.S. population is now fully vaccinated and 55.5% of the U.S. population has received at least one dose.

Bloomberg reports that the U.S. administered an average of only 527,353 does per day over the last week. Bloomberg estimates that it would take another 9 months to get 75% of the U.S. population vaccinated, which is a measure of herd immunity and a return to normalcy.