- U.S. stocks rebound higher along with China stocks although virus impact remains in flux

- U.S. ADP jobs expected to show a respectable increase

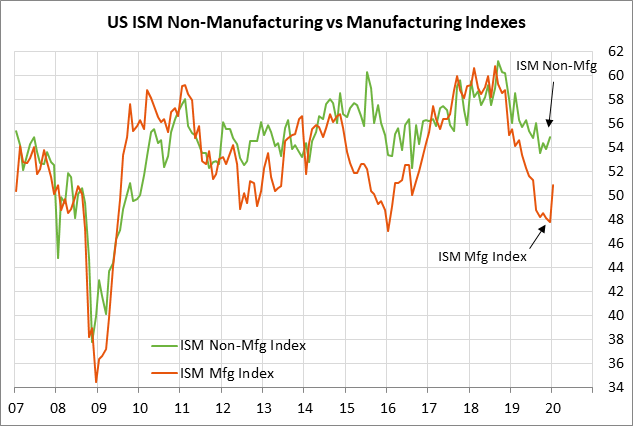

- .S. ISM non-manufacturing index expected to edge higherÂ

- U.S. trade deficit expected to widen

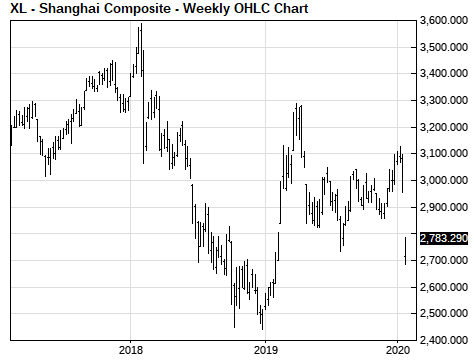

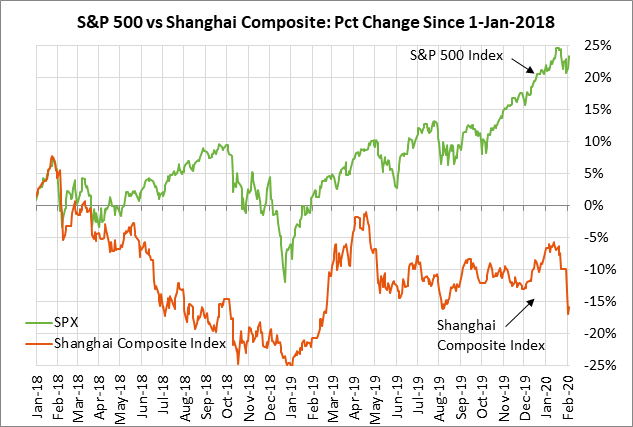

U.S. stocks rebound higher along with China stocks although virus impact remains in flux — The S&P 500 index on Tuesday rallied sharply by +1.50% to a 1-1/2 week high, bringing this week’s rally to a total of +2.23%. The U.S. stock market on Tuesday was relieved that the Chinese Shanghai Composite Index on Tuesday was able to stabilize and rebound higher by +1.34%.

Still, Tuesday’s upward rebound in Chinese stocks may have been temporary since it was mostly due to the PBOC’s aggressive liquidity injection and stock-buying by the national team. It seems difficult to believe that all the Chinese investors who want to dump their stocks have already done so.

Two-thirds of the Chinese economy will remain closed through the end of this week and the full economic impact of the coronavirus is far from over. The Chinese government is likely to continue the quarantines and extended holidays in some areas until they can be relatively certain that the virus has been contained. Since the virus has a long incubation period of 14 days, it will take at least several more weeks to know whether the regional quarantines are working to prevent an extensive spread of the virus beyond the current high-impact areas.

U.S. investors seem to be optimistic that there will not be a major outbreak of the virus in the United States. The CDC reports that there have been only 11 known cases of the coronavirus in America through Monday and no deaths. U.S. authorities are working hard to identify and isolate potential victims of the virus, thus preventing the spread of the virus.

While the new 2019-nCoV coronavirus is an alarming development, it at least has a lower death rate than SARS and is less widespread than other deadly viruses. As a matter of scale, it is worth remembering that pneumonia lands more than 250,000 Americans in the hospital each year and kills about 50,000 Americans each year, according to the CDC. The “common” flu has already killed some 10,000 Americans so far this season even though there is a vaccine for some of the variants.

It will be a matter of weeks before it becomes clear whether authorities will be able to fully contain the virus as they did with SARS, or whether the new coronavirus is already out of the bottle and will cause significant damage for months and perhaps even years to come.

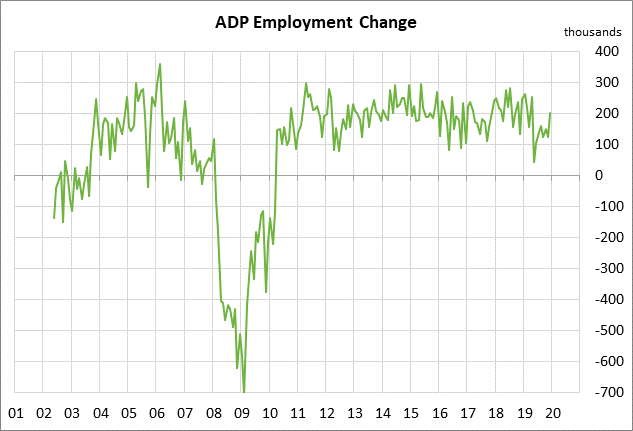

U.S. ADP jobs expected to show a respectable increase — The consensus is for today’s Jan ADP employment report to show an increase of +158,000, softening from Dec’s report of +202,000. Today’s expected report of +158,000 would roughly match the 3-month moving average and would be mildly weaker than the 12-month moving average of +167,000.

U.S. hiring in January should remain relatively firm since business confidence improved with the US/China trade deal that was announced in mid-December. The coronavirus did not emerge until mid-January. That means that any slowdown in hiring due to the virus is not likely to show up until February since the hiring process takes a matter of weeks before resulting in an actual hire that is reported in the payroll report.

On the labor front, the market is mainly looking ahead to Friday’s Jan unemployment report. The consensus is for a payroll report of +160,000, up from Dec’s weak report of +145,000 but below the 3-month average of +184,000 and the 12-month average of +176,000.

The consensus is for Friday’s Jan unemployment rate to be unchanged from the 50-year low of 3.5% seen in Nov-Dec. The Fed is forecasting that the unemployment rate has bottomed out and will move sideways this year and then move slightly higher to 3.6% by the end of 2021 and to 3.7% by the end of 2022. The Fed expects the labor market to remain tight in coming years with the unemployment rate remaining below its estimate of a long-term natural unemployment rate of 4.1%.

U.S. ISM non-manufacturing index expected to edge higher — The consensus is for today’s Jan ISM non-manufacturing index to show a +0.2 point increase to 55.1, adding to December’s solid +1.0 point increase to 54.9. Business confidence should see an improvement at least through mid-January due to the US/China and USMCA trade deals. The coronavirus will have somewhat of a negative impact on business confidence, although that impact may not show up until the February report.

The ISM’s index for the manufacturing sector, which was released on Monday, showed an unexpectedly large increase of +3.1 points to 50.9, much stronger than expectations of +0.7 to 48.5. The coronavirus did not seem to have any major negative impact on ISM manufacturing confidence in January.

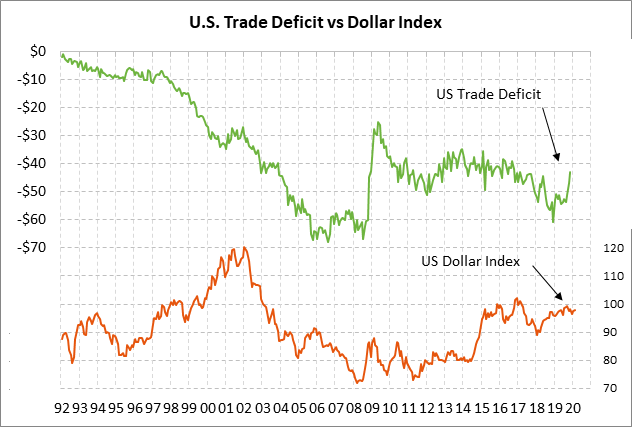

U.S. trade deficit expected to widen — The consensus is for today’s Dec trade deficit to expand to -$48.2 billion from Nov’s -$43.1 billion but remain narrower than the 12-month trend average of $52.0 billion. The U.S. trade deficit narrowed in late 2019 mainly because of a drop in imports compared with little change in exports. In November, U.S. exports showed a small +0.3% y/y increase while imports were down -3.8% y/y. Tariffs and retaliatory tariffs continue to cause major disruptions of U.S. trade flows. Despite the US/China phase-one trade deal that was signed on Jan 15, the U.S. is keeping tariffs on $370 billion of Chinese goods and China is keeping tariffs on $110 billion of U.S. goods with some exemptions to meet their requirements for purchasing U.S. products.