- US/China trade talks plod along with only 4 weeks left until the Dec 15 tariff date

- Washington ready to pass a Dec 20 CR

- Sterling rallies to 1-month high on Brexit optimism

- U.S. housing starts expected to remain strong

US/China trade talks plod along with only 4 weeks left until the Dec 15 tariff date — The markets remain hopeful that the U.S. and China will reach a phase-one deal although there seems to be no end to the last-minute demands and brinkmanship. The markets turned less optimistic yesterday after CNBC reported that Chinese officials are pessimistic about a trade deal because of President Trump’s insistence that he will not roll back existing tariffs. China continues to demand that the U.S. roll back some of the existing tariffs for a trade deal, in addition to scrapping the upcoming Dec 15 tariff.

The good news is that both sides continue to make good-faith gestures in the direction of a deal. The Trump administration on Monday gave a 6-month extension of the licenses to U.S. businesses to do business with Huawei. Meanwhile, China has been buying some U.S. ag products including soybeans and wheat.

The only real deadline for a deal doesn’t come until the December 15 date for Mr. Trump’s new 15% tariff on the remaining $160 billion of Chinese goods. The markets would be glad if a deal could get done by then considering that the two sides still seem to have some major issues to overcome such as the rollback of existing tariffs and defining the Chinese commitment for ag purchases.

Washington ready to pass a Dec 20 CR – The House today is expected to vote on a new continuing resolution to provide spending authority until Dec 20. Senate Majority Leader McConnell on Monday said he agrees with the idea of a clean CR until Dec 20 and that he believes President Trump would sign that CR. A new CR would avert a U.S. government shutdown that would otherwise occur this Friday when the current CR expires Thursday night.

Even if a new CR gets done this week, Congressional leaders do not appear to be particularly optimistic about getting an omnibus spending deal done by what would be the new deadline of Dec 20. Talk is already emerging that another CR may be necessary to get Congress into early 2020 since there is probably too little time to get a final spending deal done by Dec 20. Congressional leaders and the White House remain at odds mainly over President Trump’s demand for $9 billion in wall funding.

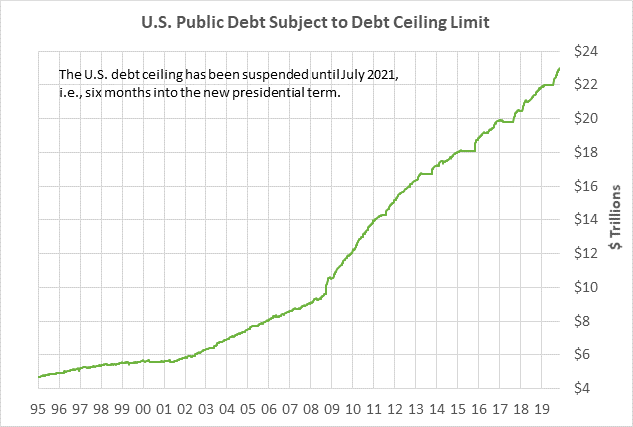

The markets are not particularly worried about Washington’s problems in getting a spending deal done for the remainder of the fiscal year since a deal is likely to get done eventually. The markets by now have seen enough U.S. government shutdowns that the threat of a shutdown no longer causes much reaction in the markets. By contrast, the markets do get worried about the debt ceiling and the threat of a Treasury default. However, the debt ceiling is not currently a problem since the debt ceiling has been suspended until July 2021, which is six months into the next presidential term.

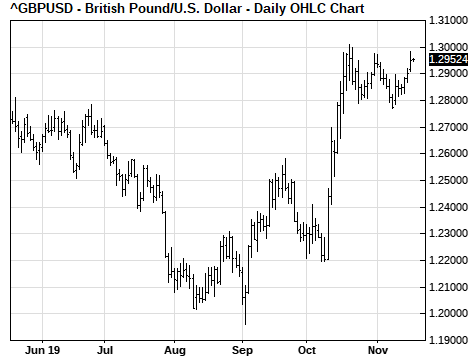

Sterling rallies to 1-month high on Brexit optimism — GBP/USD on Monday rallied to a new 1-month high of 1.2985 that was just shy of the mid-October 6-month high of 1.3013, and closed the day +0.43% at 1.2953.

GBP/USD on Monday rallied on Prime Minister Johnson’s statement that all Conservative Party candidates standing for election in the upcoming Dec 12 general election have signed a pledge to support his Brexit bill. That means that Mr. Johnson should be able to easily push his Brexit withdrawal bill through the new Parliament by the Brexit deadline of January 31 if Conservatives win a majority of seats in the new Parliament.

The betting odds are currently showing a strong probability of 65% that the Conservatives will win a majority of seats in the Dec 12 election and be able to take control of the new Parliament.

The markets would obviously be pleased if the UK Parliament can approve a Brexit withdrawal agreement before the Jan 31 deadline. However, the UK’s Brexit problems would still be far from over because the UK government will then have only 11 months to negotiate a full trade agreement with the EU before the transition period expires at the end of 2020. If there is no UK-EU trade agreement, and no UK request for a transition extension, then the UK on Dec 31, 2020, will again face the threat of a chaotic no-deal Brexit separation from the EU with hard borders and WTO tariffs. The markets can expect to be subjected to another round of hardball by PM Johnson on threats for a no-deal Brexit at the end of 2020 if the UK doesn’t get its way with the EU on a trade deal.

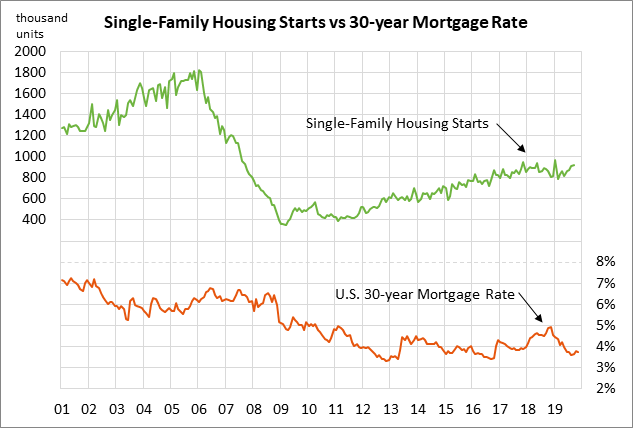

U.S. housing starts expected to remain strong — The market consensus is for today’s Oct housing starts report to show a +5.1% increase to 1.320 million, reversing more than half of September’s sharp -9.4% drop to 1.256 million. Housing starts in August spiked upward by +15.1% to a 12-year high of 1.386 million units but then fell back by -9.4% in September.

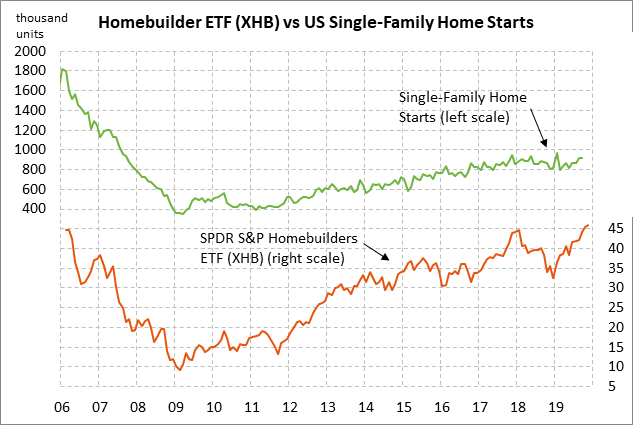

Homebuilder confidence remains strong with the NAHB housing index at 70 in November, which is just 4 points below the 20-year high of 74 posted in Dec 2017. Meanwhile, homebuilder stocks are doing well with the SPDR S&P Homebuilders ETF (XHB) up +41% year-to-date and trading just below September’s 1-3/4 year high and the early-2018 record high.

Conditions in the U.S. housing sector are positive mainly because of this year’s plunge in mortgage rates. The current 30-year mortgage rate of 3.75% is down by a massive -119 bp from the 8-3/4 year high of 4.94% posted in late 2018 and is just mildly above the recent 3-year low of 3.49% posted in September.