- Weekly global market focus

- Markets wait for of Monday’s drop in Chinese mainland stocks

- U.S. ISM manufacturing index will be largely overlooked since it will not fully reflect the virus impact

- U.S. earnings season remains in high gear

Weekly global market focus — The U.S. markets this week will focus on (1) the extent of the economic damage being done by China’s coronavirus, (2) Washington events including President Trump’s State of the Union address on Tuesday and the Senate’s verdict on Wednesday in President Trump’s impeachment trial, (3) the Democratic presidential campaign as the first vote occurs today with the Iowa caucuses, (4) global stocks, which are focused on the extent of today’s sell-off in the Chinese mainland stocks, (5) world bond yields, which have plunged on the coronavirus with the amount of negative interest-rate global debt rising by $2.7 trillion to $13.9 trillion in just the last two weeks, (6) a heavy earnings week with 96 of the S&P 500 companies reporting, and (7) Friday’s Jan payroll report (expected +160,000 after Dec’s +145,000).

Brexit will be in the news today as Prime Minister Johnson delivers a speech laying out his demands for a UK/EU trade deal. Meanwhile, the EU today is scheduled to release the details of its negotiating mandate. The UK Telegraph over the weekend reported that PM Johnson is “privately infuriated” that the EU seems to be backtracking on the plan for a UK/EU free trade agreement because the UK will not agree to any dovetailing of UK regulations and taxes with the EU. PM Johnson is threatening to move from a Canadian-style free trade agreement to an Australian model where the two sides pick some sectors for cooperation while other sectors operate under WTO tariffs.

This week’s Chinese economic data will be watched for the extent of the virus damage done thus far. China’s Jan Caixin services PMI on Tuesday night is expected to show a -0.5 point decline to 52.0, adding to Dec’s -1.0 point decline. China’s Jan trade report on Thursday night is expected to show a -4.5% y/y drop in exports and a +2.0% y/y increase in imports.

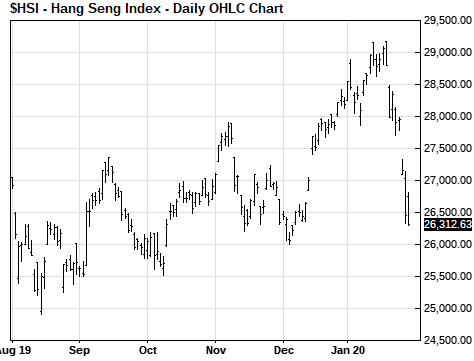

Markets wait for of Monday’s drop in Chinese mainland stocks — The global markets are waiting to see how far Chinese mainland stocks will drop when they reopen on Monday after the 6-session extended holiday. A sell-off of anything more than the 5-7% sell-off already seen in Chinese mainland stock proxies would negatively impact the rest of the global markets. The Hang Seng index last Friday closed -5.7% lower from its close on Jan 23, which was the last day of trading for mainland China. The iShares MSCI China ETF (MCHI), which trades on the Nasdaq, closed last Friday down by -6.8% from the Jan 23 close when mainland Chinese stocks were last open.

Chinese authorities over the weekend announced a slew of support measures designed to support the Chinese economy and financial system in the wake of the virus. State-supported financial institutions today are also expected to be out in force, providing some buying support for Chinese stocks.

China’s economy is being hit hard by the virus since there are large swaths of the Chinese population under quarantine, large-scale business shutdowns, and the extension of the Lunar New Year holiday through this week in a large portion of the country. There is no sign that the spread of the virus is yet slowing. The impact from the coronavirus is likely to rival that from SARS with a hit to China’s Q1 and Q2 GDP of one percentage point or more. SARS caused a 2 percentage point hit to China’s GDP in Q2-2003 to +9.1% from Q1’s +11.1%.

The consensus is that U.S. GDP will take a hit of at least 0.2 percentage points from the virus, with Goldman forecasting a 0.4 point hit to Q1 U.S. GDP. U.S. exports to China will decline, U.S. supply chains will be disrupted by the near shutdown of China’s economy, and U.S. citizens may reduce their travel and stay away from public places since the virus has already migrated to the U.S.

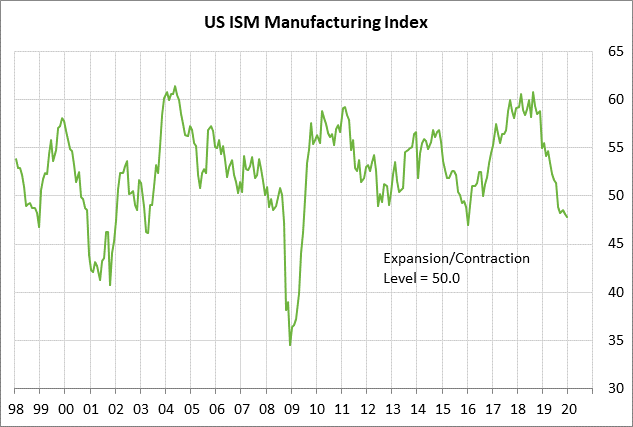

U.S. ISM manufacturing index will be largely overlooked since it will not fully reflect the virus impact — The market consensus is for today’s Jan ISM manufacturing index to show a +0.7 point increase to 48.5, more than reversing Dec’s -0.3 point decline to 47.8. The Jan ISM new orders index is expected to edge slightly higher by +0.1 to 47.7, adding to Dec’s +0.8 point increase to 47.6.

Today’s ISM manufacturing index will be of limited value since it will not pick up the full effect of the spreading coronavirus. Indeed, last week’s Jan China manufacturing PMI fell by only -0.2 points to 50.0 and did not come close to fully taking into account the coronavirus that has shut down large swaths of the Chinese economy.

There had been some hope that December’s US/China trade agreement might allow the global manufacturing sector to start to recover. However, the spreading economic damage from the Chinese coronavirus means that the U.S. manufacturing sector is likely to remain in a recession for at least several more months. U.S. manufacturing production fell by -1.3% y/y in December and has been in negative year-on-year territory since last July.

U.S. earnings season remains in high gear — There are 96 of the S&P 500 companies that report earnings this week. Notable reports include Alphabet on Monday; Disney and Ford on Tuesday; GM on Wednesday; Twitter and Yum! Brands on Thursday; and AbbVie on Friday.

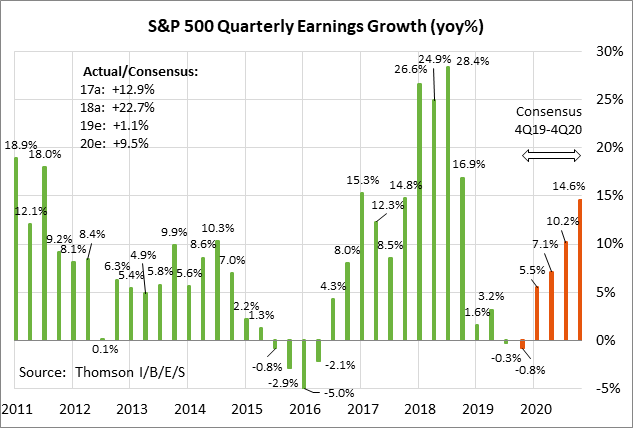

The consensus is for Q4 SPX earnings growth of -0.8% y/y (+2.4% ex-energy), according to Refinitiv. That would follow the weak 2019 quarterly growth rates of +1.6% in Q1, +3.2% in Q2, and -0.3% in Q3. Looking ahead, the consensus is for earnings growth of +5.5% in Q1-2020, +7.1% in Q2, +10.2% in Q3, and +14.6% in Q4. The consensus is for earnings growth in calendar 2020 to improve to +9.5% from the weak growth of only +1.1% seen in 2019 due to trade tensions and a hangover from the 2018 earnings surge of +23% on the massive tax cut.