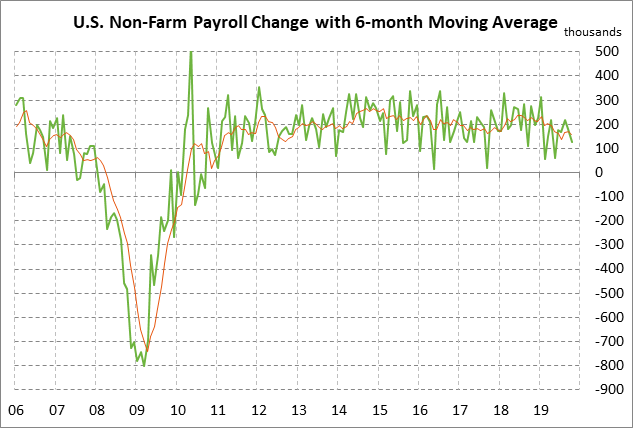

- Payroll growth expected to be modest after excluding upward bump from returning GM strikers

- US/Chinese tariff deadline of Dec 15 is now just 6 business days away

- U.S. consumer sentiment index expected to tick higher

Payroll growth expected to be modest after excluding upward bump from returning GM strikers — The consensus is for today’s Nov payroll report to show an increase of +184,000, improving from October’s weak report of +128,000. Today’s payroll report is expected to be inflated by about +46,000 because of returning GM strikers, who subtracted about -46,000 from the weak Oct payroll report.

Expectations for today’s payroll report were dented by Wednesday’s news that the Nov ADP employment report rose by only +67,000, which was substantially below expectations of +140,000.

In the bigger picture, job growth is slowing as seen by the fact that the 6-month moving average fell to +156,000 in October, down sharply from the +223,000 monthly average seen in 2018.

U.S. job growth is downshifting because the U.S. manufacturing sector is in a recession and because GDP is in the process of slowing to next year’s expected pace of +1.8% from about +2.3% in 2019 and +2.9% in 2018. In addition, the U.S. economy has already generated 21.9 million new jobs since the Great Recession ended, meaning that many U.S. businesses may already be fully staffed, particularly with economic growth now slowing.

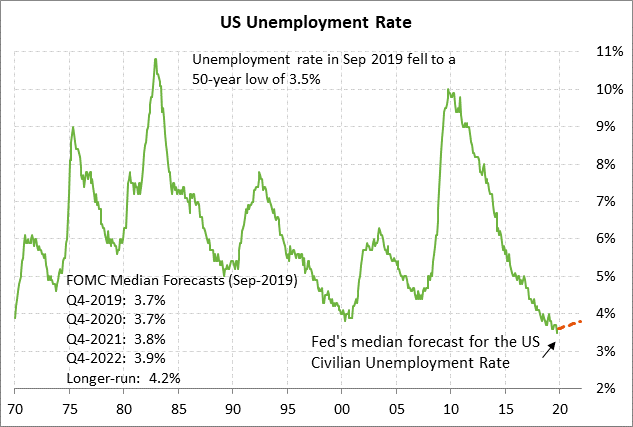

The consensus is for today’s Nov unemployment rate to be unchanged at +3.6%, which would be only +0.1 point above Sep’s 50-year low of +3.5%. Job growth has been strong enough to keep the unemployment rate near 50-year lows. However, the unemployment rate could begin to creep a bit higher if hiring slows, as expected.

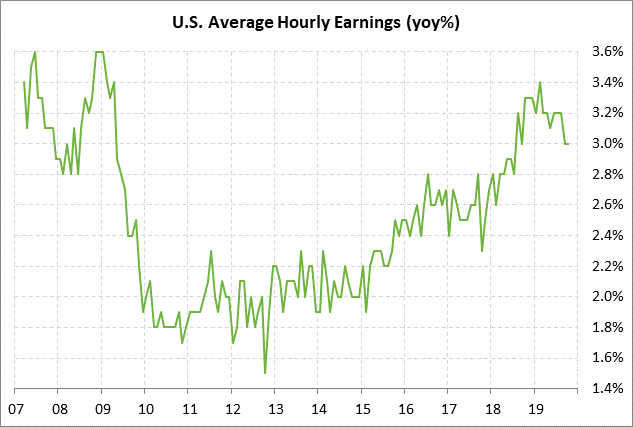

Meanwhile, wage growth has been modest and is not showing the strength that could be expected based on the tight labor market. The consensus is for today’s Nov average hourly earnings report to be unchanged at +3.0% y/y for the third consecutive month. The current hourly earnings growth rate of +3.0% is at a 15-month low and is down from the 10-year high of +3.4% seen back in February.

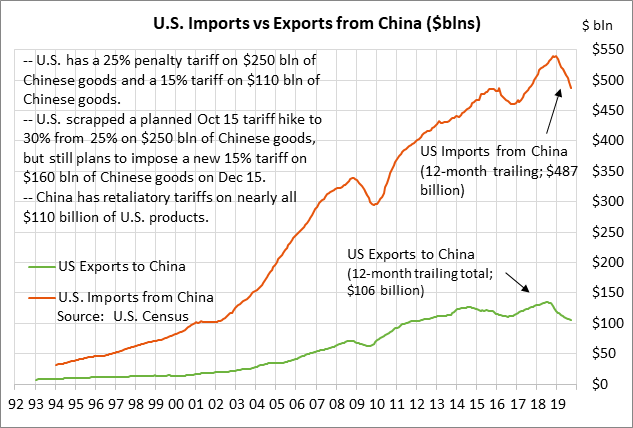

US/Chinese tariff deadline of Dec 15 is now just 6 business days away — There are now just 6 business days left before next Sunday’s Dec 15 tariff deadline when President Trump plans to slap a 15% tariff on the last $160 billion of Chinese goods. At that point, the U.S. would have a 25% tariff on $250 billion of Chinese goods and a 15% tariff on about $270 billion of Chinese goods, meaning there would be tariffs on virtually all Chinese goods imported into the United States. China already has tariffs on virtually all of the $110 billion of U.S. goods exported to China.

The U.S. and China negotiations by all accounts are hung up on the issues of ag purchases and tariff rollbacks. The Trump administration is trying to get China to commit ahead of time to buy $40-50 billion worth of U.S. ag products per year with a 2-year ramp-up. That would be more than double the $20 billion amount of U.S. ag products that China bought in 2017 before retaliatory tariffs cut those Chinese purchases to only $9 billion in 2018.

The U.S. is clearly making a big ask. The U.S. wants China to more than double its annual purchases of U.S. products in coming years even though China doesn’t know what quantity of ag products they will need. In addition, there is no way to know whether U.S. ag products in coming years might be much more expensive than ag products from other regions such as South America due to the various factors that affect ag-price differentials between countries such as weather, transportation costs, and currency fluctuations. There is also the problem that China is a hybrid Communist/capitalist country and can’t easily force private companies to buy products that might be against their interests.

Meanwhile, China is demanding rollbacks of existing tariffs. The Trump administration is loathe to provide any tariff rollbacks since that would reduce its bargaining power in any phase-two trade negotiation. Yet if the U.S. refuses to roll back any tariffs, then China gets nothing in return for its trade concessions. In that case, China has no real reason to make a deal except to try to head off new tariffs, which might come anyway.

The Wall Street Journal on Thursday reported that U.S. officials over the past few days have become less optimistic about a deal because the two sides remain at odds on ag purchases and tariff rollbacks. There is always a chance that the two sides will suddenly capitulate and reach a deal. At this point, however, the markets seem to be hoping for at least an extension of the talks and a deferral by Mr. Trump of the Dec 15 tariff.

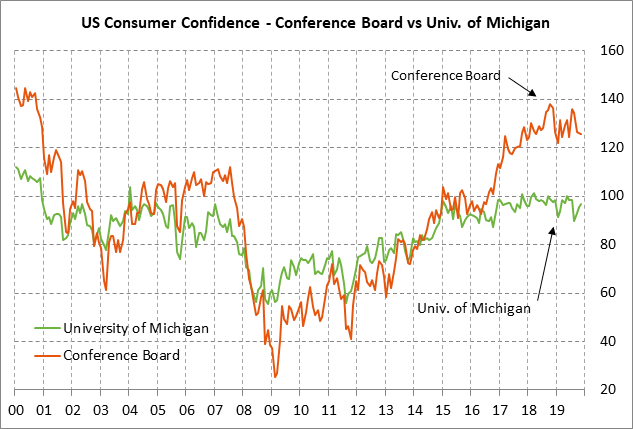

U.S. consumer sentiment index expected to tick higher — The market consensus is for today’s preliminary-Dec University of Michigan U.S. consumer sentiment index to show a +0.2 point gain to 97.0, adding to November’s +1.3 point increase to 96.8. The index fell to a 3-year low of 89.8 in August but has now risen for the last three consecutive months to November’s 4-month high.

While the recent strength in the University of Michigan’s consumer sentiment index has been encouraging, the Conference Board’s index has been headed lower, raising some concerns about consumers. The Conference Board’s consumer confidence index has fallen for the last four months (Aug-Oct) by a total of -10.3 points to post an 8-month low of 125.5 in November.

While U.S. consumer confidence is seeing support from the strong labor market and the record highs in the stock market, confidence is being undercut by trade tariffs, political uncertainty in Washington, and the slowdown in U.S. GDP growth.