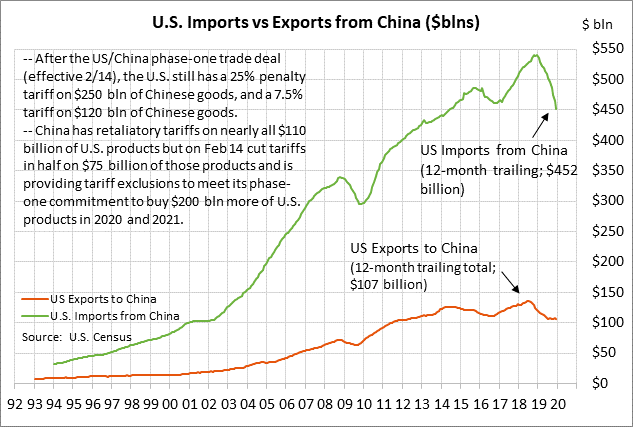

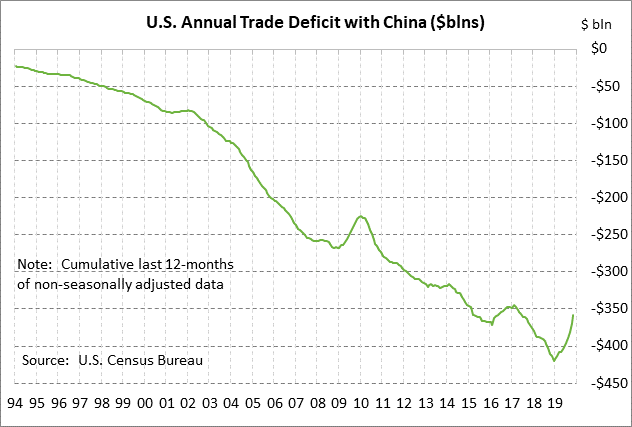

- US/China phase-one trade deal goes into effect today amidst doubts about Chinese purchase intentions

- U.S. Feb consumer sentiment expected to sag

- U.S. Jan retail sales expected to show a modest gain

- U.S. manufacturing production expected to slip

US/China phase-one trade deal goes into effect today amidst doubts about Chinese purchase intentions — The US/China phase-one trade deal goes into effect today, 30 days after it was signed on Jan 15. Effective today, the U.S. will cut its tariff in half from 15% to 7.5% on $120 billion of Chinese goods and China will cut its retaliatory tariffs in half on $75 billion of U.S. goods.

However, a hefty amount of penalty tariffs will remain in place after today. The U.S. will leave in place the 25% tariff on the original $250 billion of Chinese goods and a 7.5% tariff on $120 billion of Chinese goods. China will leave in place tariffs on about $110 billion of U.S. goods, with exemptions as necessary to fulfill its promises to purchase U.S. goods.

President Trump has said that the U.S. tariffs on Chinese goods will remain in place as leverage during the phase-two trade talks. President Trump has shown no urgency as yet to begin the phase-two talks and a phase-two deal does not seem likely until after the election. The markets are therefore expecting U.S. and China penalty tariffs to remain in place at least through the remainder of this year.

The big question regarding the phase-one trade deal continues to be whether China will live up to its promises to purchase $200 billion of extra U.S. goods during 2020-21. If not, President Trump may reimpose the tariffs and start a new round of conflict for US/China trade.

Chinese officials have said that the coronavirus is likely to slow Chinese purchases of U.S. goods, but they have also said they will meet the purchase requirements by year-end. Purchase delays are likely to frustrate President Trump, who needs the Chinese purchases during the current presidential campaign season to display what he got out of the trade deal.

For China’s part, the coronavirus could provide cover for delaying the purchases as long as possible as they wait to see if Mr. Trump is re-elected on November 3. If Mr. Trump is not re-elected, then China may no longer be on the hook for those purchases, depending on how a new Democratic president approaches trade relations with China.

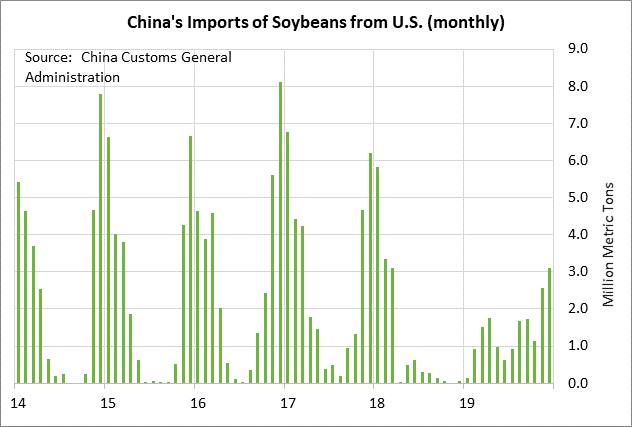

China, in the phase-one trade deal, agreed to buy an extra $200 billion of U.S. products during 2020-21 above a 2017 baseline. China agreed to buy at least $40 billion annually of U.S. agriculture and seafood products in 2020-21, more than the $29 billion record seen in 2013. China agreed to buy at least $30 billion of U.S. energy products (LNG, crude oil, coal) in 2020 and $46 billion in 2021. China agreed to buy at least $120 billion of U.S. manufactured products in 2020 and $132 billion in 2021. China agreed to buy at least $100 billion of U.S. services in 2020-21.

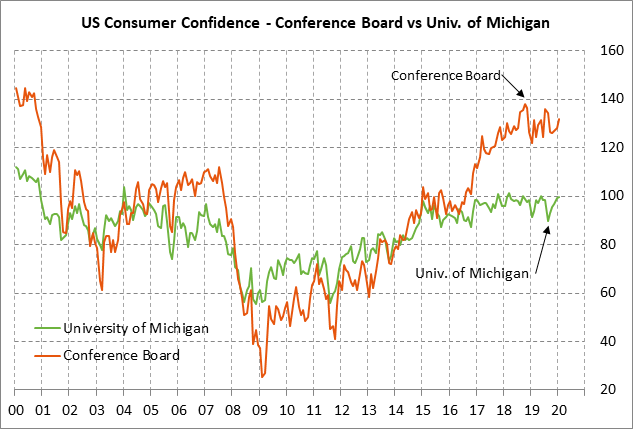

U.S. Feb consumer sentiment expected to sag — The consensus is for today’s preliminary-Feb University of Michigan U.S. consumer sentiment index to show a small -0.4 point decline to 99.4, reversing most of January’s +0.5 point increase to 99.8. The index in January was in good shape at only 1.6 points below the 16-year high of 101.4 posted in March 2018.

The sentiment index in January showed a small +0.5 point increase even though the news of the coronavirus started to emerge in mid-January. The question is whether the virus will cause significant weakness in consumer sentiment in February. On the plus side for consumer sentiment, the virus has not gained a foothold in the U.S. and the stock market has displayed its lack of concern by rallying to new record highs. However, the virus has yet to peak in China and the global economic damage has yet to be fully seen. Consumer sentiment in early February may also have been undercut by political uncertainty surrounding the Senate impeachment trial, which concluded with an acquittal on February 6.

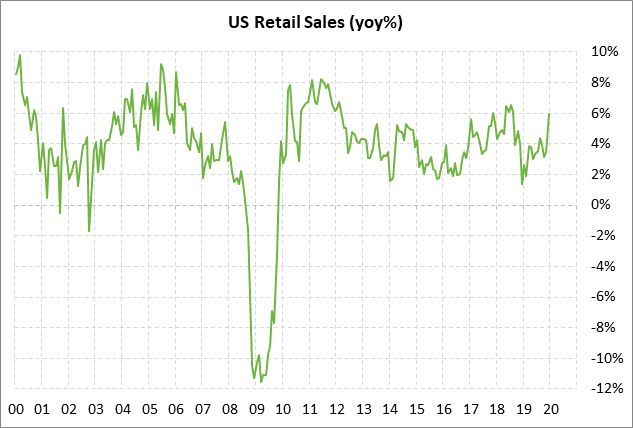

U.S. Jan retail sales expected to show a modest gain — The consensus is for today’s Jan U.S. retail sales to show an increase of +0.3% and +0.3% ex-autos following Dec’s report of +0.3% and +0.7% ex-autos. Retail sales in December showed a large year-on-year gain of +5.8% but that was mainly because of a low year-earlier base when retail sales plunged by -2.0% m/m in December 2018 due to a U.S. government shutdown, bad weather, the Q4-2018 plunge in stocks, and talk of a recession.

The U.S. economy continues to depend heavily on consumers to keep it afloat while business investment remains weak and the U.S. manufacturing sector remains in a recession. U.S. consumer spending contributed 1.20 points to the Q4 GDP report of +2.1%, although that was down from the hefty 2.12 point contribution in Q3 and 3.03 points in Q2.

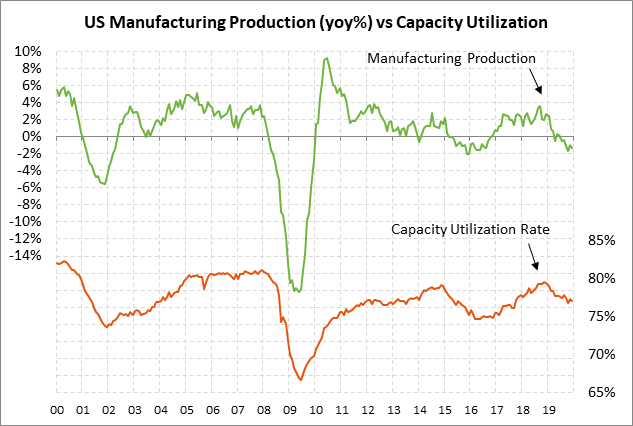

U.S. manufacturing production expected to slip — The consensus is for today’s Jan manufacturing production report to show a small decline of -0.1% after the +0.2% increase seen in December. The headline Jan industrial production report is expected to fall -0.2%, adding to Dec’s decline of -0.3%.

U.S. manufacturing production in Nov-Dec strung together back-to-back gains of +1.0% m/m and +0.2% m/m, which was a positive sign. However, manufacturing production on a year-on-year basis was down -1.3% y/y in December for the sixth consecutive year-on-year decline, indicating recessionary conditions in the U.S. manufacturing sector. On the brighter side, the ISM manufacturing index in January rose by +3.1 to 50.9, rising above 50 for the first time in 6 months, likely because of the US/China trade deal reached in mid-December. However, the manufacturing sector is now dealing with the sharp hit to the Chinese economy caused by the coronavirus.