- Time is running out for stimulus negotiations ahead of Friday’s House recess

- Markets wait for any shift in polling following last night’s Trump-Biden debate

- Last ADP and payroll reports before the election are expected to show improvement

- U.S. GDP forecasts are being trimmed while today’s U.S. Q2 GDP is expected to be unrevised

Time is running out for stimulus negotiations ahead of Friday’s House recess — Time is quickly running out for a stimulus deal since the House is scheduled to leave Washington on Friday for a recess that will last until after the November 3 election. During the recess, House members could be called back to Washington at any time to vote on a stimulus bill. However, if there isn’t a deal this week, then the chances for a stimulus deal appear to be slim since Congressional attention after this week will focus mainly on campaigning.

House Speaker Pelosi and Treasury Secretary Mnuchin are scheduled to talk again today, extending their series of phone calls that began last Friday. Ms. Pelosi said after her call with Mr. Mnuchin on Tuesday that their talks have been “positive” and that “We’ll get back together tomorrow to see how we can find common ground.”

House Democrats have a $2.2 trillion stimulus bill they plan to approve before leaving Friday for their recess, if there isn’t a deal in the meantime on a smaller bill. President Trump has indicated he is willing go as high as $1.5 trillion on a stimulus deal, but it isn’t clear whether he could deliver on that idea since Senate Republicans do not want to go above $1 trillion. Speaker Pelosi seems unlikely to come down very far from her current offer of $2.2 trillion.

Stock investors will be unhappy if they have to wait until after the election for new talks on a stimulus bill. Moreover, there is no assurance that a stimulus bill could pass during the lame-duck session given how far the parties are apart and how the political climate could turn even nastier after the election.

Senate expected to pass CR today — The Senate today is expected to pass the continuing resolution to fund the U.S. government through Dec 11, which would avert a U.S. government shutdown on Thursday. The Senate yesterday voted on the procedural measure to bring the bill to the floor for a final vote by the wide margin of 82-8, indicating that the CR should easily pass the Senate today.

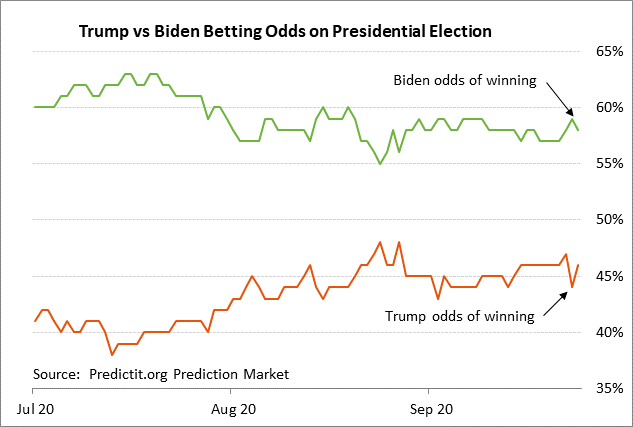

Markets wait for any shift in polling following last night’s Trump-Biden debate — The markets will be watching the polling and the betting odds to gauge reaction to last night’s Trump-Biden debate. The next debate will be next Wednesday’s Pence-Harris debate. There will then be two more presidential debates on Oct 15 and Oct 22. There are now only 34 days left until the November 3 election.

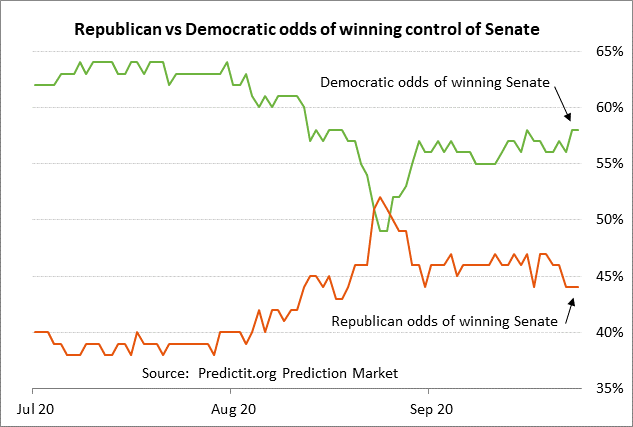

The betting odds going into last night’s debate were 58% for a Biden win versus 46% for a Trump win, according to PredictIt.com. The betting odds for control of the Senate are at 58% for the Democrats and 44% for the Republicans. The betting odds for control of the House are at 84% for the Democrats and 17% for the Republicans.

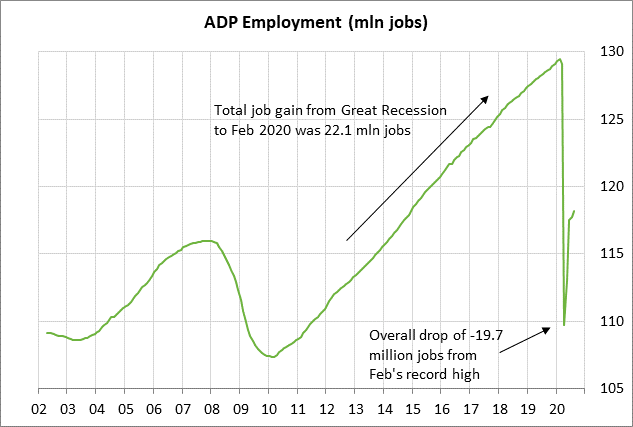

Last ADP and payroll reports before the election are expected to show improvement — Today’s ADP report and Friday’s payroll report will be the last set of monthly labor market reports before the November 3 election. While this week’s data is expected to show continued improvement, the U.S. labor market remains in dismal shape.

There are still 10.9 million more people on the unemployment rolls than before the pandemic, and the number of U.S. payroll jobs is still down by -11.5 million from the pre-pandemic level. Meanwhile, Friday’s Sep unemployment rate is expected to fall by -0.2 points to 8.2%, but that would still be more than double the pre-pandemic level of 3.5% and only 2 points below the worst level of +10.0% seen during the Great Recession.

The U.S. labor market has no real hope of fully recovering until there is an effective and widely-available vaccine that allows life to fully return to normal. Even then, job levels will lag because the huge number of bankruptcies and business closures means that many jobs will be permanently lost.

The consensus is for today’s Sep ADP report to show a gain of +648,000, adding to Aug’s recovery of +428,000. ADP jobs have so far recovered only 43% of the job losses seen this past spring from the pandemic economic shutdowns. ADP jobs have improved by +8.5 million from April’s low, but would have to rise by another 11.2 million to match February’s pre-pandemic record high.

U.S. GDP forecasts are being trimmed while today’s U.S. Q2 GDP is expected to be unrevised — The consensus is for today’s Q2 GDP to be left unrevised at -31.7% q/q annualized (-9.1% q/q). An unrevised Q2 report today would leave U.S. GDP down by a total of -10.4% in the first half of 2020, which qualifies as the worst recession in post-war history and much worse than the -4.1% peak-to-trough decline seen in the Great Recession in 2007-09.

Looking ahead the consensus is for a GDP gain of +15.1% q/q annualized (+3.6% q/q) in the current third quarter, which would recover less than a third of the first-half-2020 GDP decline.

Meanwhile, forecasts for Q4 GDP growth are fading due to the lack of a new stimulus bill. The consensus is for a rise of +5.0% q/q annualized (+1.2% q/q). However, JPMorgan last week cut its Q4 GDP estimate to only +2.5% (q/q annualized) from +3.5%, and Goldman Sachs halved its Q4 GDP forecast to +3.0% (q/q annualized) from +6.0%.

The GDP recovery in the second half of 2020 isn’t expected to come close to reversing the decline seen in the first half of 2020. Indeed, the consensus is that GDP growth in 2020 as a whole will fall by -4.4%. The market is then expecting only a partial recovery of +3.8% in 2021, stretching the final recovery of GDP into 2022 when GDP is expected to show a tepid increase of only +2.9%.