- Squeaker on House Obamacare vote sparks worries about general Republican agenda

- U.S. existing home sales expected to fall slightly from 10-year high

- FHFA U.S. house price index expected to show another solid gain

- Weekly EIA report expected to show +2.7 mln bbl rise in crude oil inventories

Squeaker on House Obamacare vote sparks worries about general Republican agenda — The stock market on Tuesday fell sharply due in part to concerns about whether the House on Thursday will be able to pass Speaker Ryan’s Obamacare repeal-and-replace bill. Some conservatives are still vowing to vote against the bill even after a personal appeal from President Trump on Tuesday morning.

The stock market is hoping that the House can pass the bill and then move on to the corporate tax reform bill, which is of much more direct importance to the stock market. If Speaker Ryan cannot get the current Obamacare bill passed, then he will have to go back to the drawing board on stripping out major provisions that will change the entire character of his bill. That would slow down the ability of the House to move on to corporate tax reform. The markets are also concerned that the difficulties that the Congressional Republicans are having on Obamacare may be a precursor to similar problems on corporate tax reform.

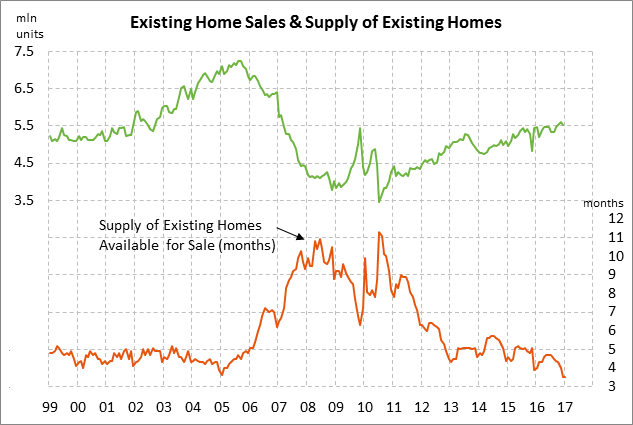

U.S. existing home sales expected to fall slightly from 10-year high — The market consensus is for today’s Feb existing home sales report to fall by -2.4% to 5.56 million, backing off slightly from the 10-year high of 5.69 million posted in the previous month of January. The rise in home sales to a 10-year high in January was particularly impressive given that it is somewhat difficult to even find an acceptable home to buy due to the tight supply of homes on the market. In January, the supply of homes on the market was extremely tight at a record low of 3.5 months worth of sales.

The strength in home sales is currently being seen in both single family homes and multi-family units, illustrating across-the-board demand. Specifically, sales of single family homes in January posted a 10-year high of 5.04 million units while Jan multi-family sales were just below December’s 10-year high.

While home demand is currently very strong, the question is whether demand will start to soften due to higher mortgage rates. The 30-year mortgage rate last week rose by +9 bp to 4.30%, which was just -2 bp below the 3-year high of 4.32% posted in late December. We suspect the rise in mortgage rates will only mildly hurt home sales because many potential home buyers realize that mortgage rates are still at attractively-low levels and will only rise in coming years as the Fed raises interest rates. That means that buying a home now is still likely to be a better deal than waiting and paying even higher mortgage rates later.

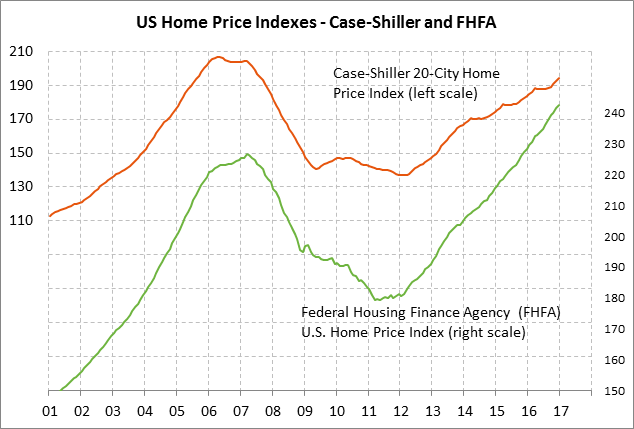

FHFA U.S. house price index expected to show another solid gain — The market consensus is for today’s Jan FHFA house price index to show another solid increase of +0.4% m/m, matching December’s increase. The FHFA index is up sharply by +6.2% y/y and by +35% from the housing-bust low posted in March 2011.

The sharp rise in home prices is being driven by very strong demand as well as by tight supplies. As mentioned earlier, the supply of existing homes on the market is currently at a record low of 3.5 months. There have recently been anecdotal reports about how bidding competition is sometimes producing a final home sales price in excess of the asking price. Higher mortgage rates may cool demand slightly, but until more homes come on the market to satisfy demand, U.S. home prices are likely to keep on rising.

U.S. home builders are responding to the strong home demand and rising home prices by ramping up construction of new homes. U.S. housing starts were strong in February at only -2.4% below the 9-1/2 year high of 1.320 million units posted in Oct 2016. U.S. home builders are in a very optimistic mood as seen by the fact that the National Association of Home Builders’ housing market index in February rose sharply by +6 points to a new 12-year high of 71.

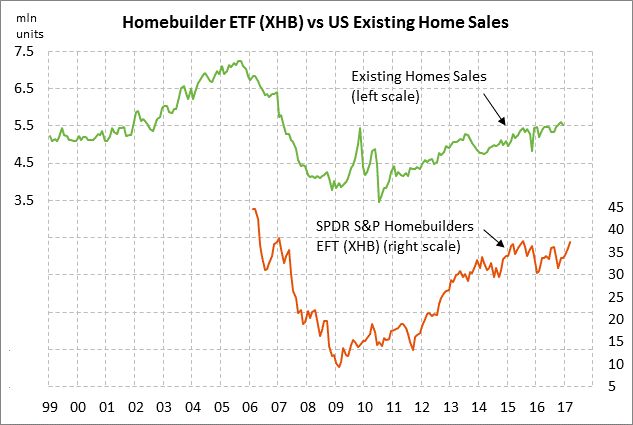

The stock prices of U.S. housing companies have done very well in the past several months due to the strong housing market and the post-election euphoria. The SPDR S&P Homebuilder ETF (XHB) fell sharply by -1.6% yesterday due to the decline in the broad market. However, XHB posted a 1-1/2 year high just last week and is still up by +15% since the November election.

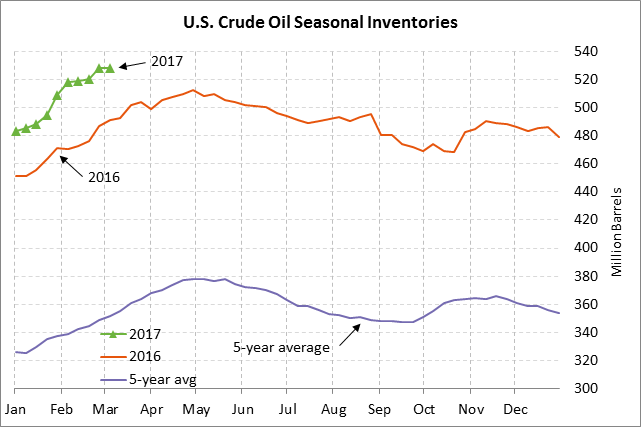

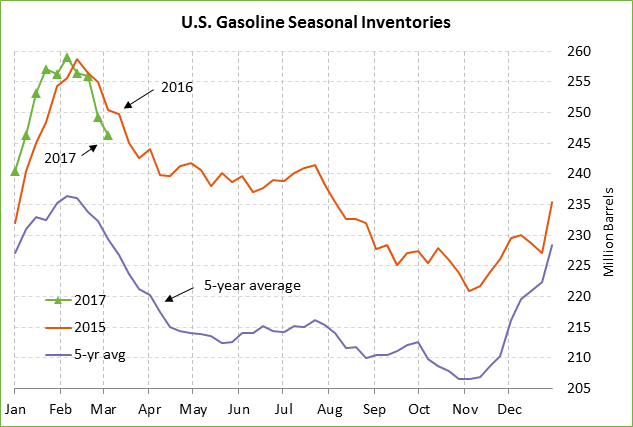

Weekly EIA report expected to show +2.7 mln bbl rise in crude oil inventories — The market consensus for today’s weekly EIA report is for a +2.7 million bbl rise in U.S. crude oil inventories, a -2.4 million bbl decline in gasoline inventories, a -1.5 million bbl decline in distillate inventories, and a +0.2 point rise in the refinery utilization rate to 85.3%.

The U.S. oil market remains in a massive glut with U.S. crude oil inventories just slightly below the record high of 528.393 million barrels posted in the week of March 3. U.S. crude oil inventories are +37.4% above the 5-year seasonal average. Product inventories are also plentiful with gasoline inventories at +5.6% above the 5-year seasonal average and distillate inventories at +19.7% above average.

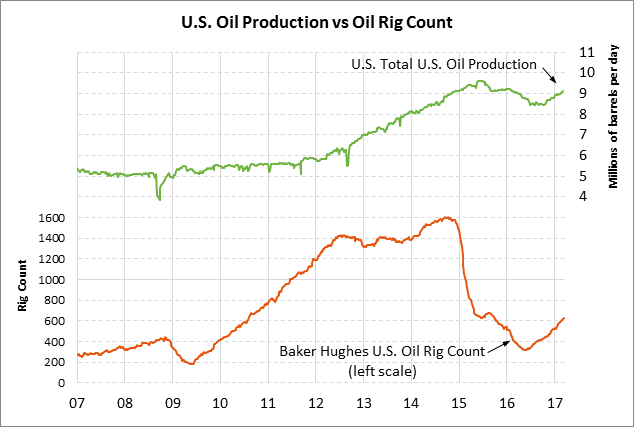

Meanwhile, U.S. oil production continues to rise and has not been negatively impacted as yet by the sharp 11% sell-off in oil prices seen the end of February. U.S. oil production in last week’s EIA report rose by +0.2% to post a new 1-year high of 9.109 million bpd. U.S. oil production has now risen by +8% since last July. U.S. oil production is likely to keep rising in coming weeks due to the sharp increase in the number of new oil wells. The number of active U.S. oil wells last week rose by another 14 wells to a 1-1/2 year high of 631 wells, twice the number of active wells seen just 10 months ago.