- Weekly market focus

- U.S. stock market remains at record high on earnings, economic data, and tax reform hopes

- Markets await Trump/Republican corporate tax plan

- 2-year T-note auction to yield near 1.19%

- Favorable Q4 earnings season winds down with focus on retailers

Weekly market focus — Market attention this week will focus on (1) any fresh details on Trump/Republican tax plans although Congress is on recess this week, (2) fine-tuning of Fed expectations with the release of the Jan 31/Feb 1 FOMC minutes on Wednesday and with four appearances by Fed officials this week, (3) European concerns as the French presidential election is now only nine weeks away and as the Greece bailout impasse continues, (4) the tail-end of Q4 earnings season with 50 of the S&P 500 companies scheduled to report this week, and (5) the Treasury’s sale this week of $101 billion of T-notes.

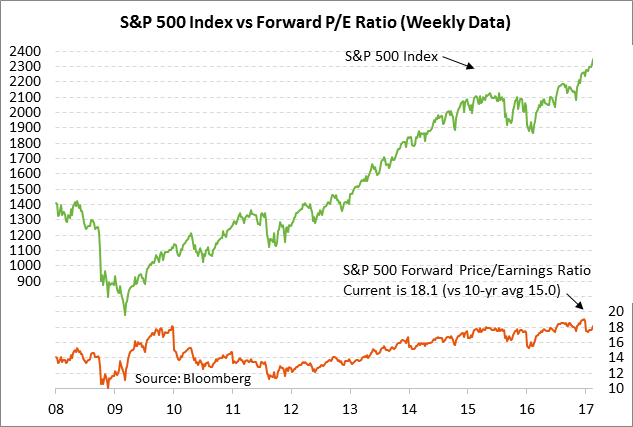

U.S. stock market remains at record high on earnings, economic data, and tax reform hopes — U.S. stock market sentiment comes into this week on a continued strong footing after the S&P 500 index last Friday closed at a new record high. The U.S. stock market took off on its latest up-leg on Feb 9 when Mr. Trump promised to announce a “phenomenal” tax plan in 2-3 weeks.

Since Mr. Trump’s statement, the Q4 earnings results have remained strong and the U.S. Jan retail sales ex-autos report of +0.8% was much stronger than market expectations of +0.2%, suggesting that the post-election surge in consumer confidence is translating into higher spending. Indeed, the Bloomberg U.S. Economic Surprise Index last Friday moved up to a 4-1/2 year high of 0.492 standard deviations, indicating that upside economic surprises are the best since March 2012. On the earnings front, stocks have been supported by the stronger-than expected Q4 earnings season and by expectations that SPX earnings in 2017 will show strong growth of +11% after two years of negligible earnings growth.

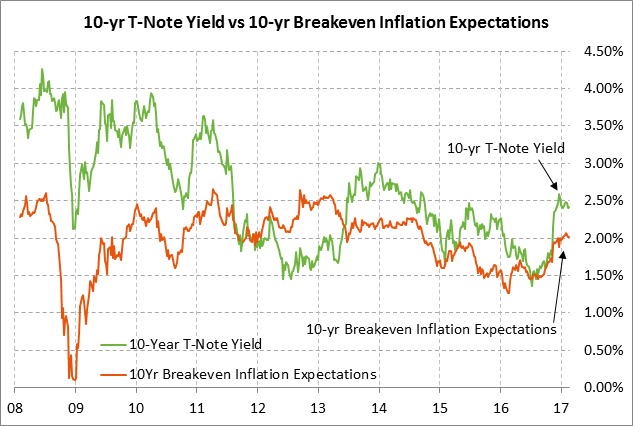

Meanwhile, March 10-year T-note futures prices rallied mildly late last week but remained within their narrow year-to-date trading range. The 10-year T-note yield last week fell back late to 2.41% and is currently near the middle of its 2-month trading range. T-note prices remain under pressure from strong U.S. economic data, the strength in stocks, and expectations for at least two Fed rate hikes this year. However, T-note prices have support from the slow progress of the Republican fiscal agenda and some safe-haven demand tied to European political concerns.

Markets await Trump/Republican corporate tax plan — The markets are hoping for some clarity on the tax-cut situation when President Trump next Tuesday delivers his address to a joint session of Congress. The markets suspect that Mr. Trump may announce his tax plan at that speech since the timing would line up with his statement on Feb 9 that he would release “something phenomenal in terms of tax” over “the next two or three weeks.”

A key question will be whether Mr. Trump’s tax plan includes the border adjustment tax plan that is being promoted by House Republican leaders. There has been strong opposition in the Senate to that measure, which suggests that Mr. Trump may not include that measure in his overall tax plan. Without the estimated $1.1 trillion in revenue over ten years from the border adjustment tax system, however, Republicans will not be able to cut the corporate tax rate to as low as their intended target of 20% (from the current 35%) unless they find other pay-fors or simply let the budget deficit and national debt rise.

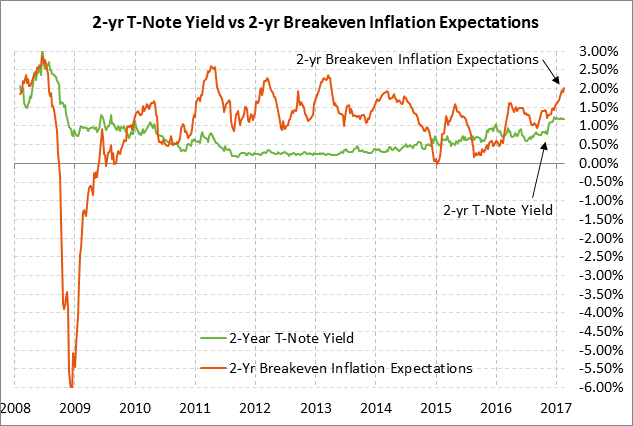

2-year T-note auction to yield near 1.19% — The Treasury today will sell $26 billion of 2-year T-notes. The Treasury will then continue this week’s $101 billion T-note package by selling $34 billion of 5-year T-notes and $13 billion of 2-year floating-rate notes on Wednesday, and $28 billion of 7-year T-notes on Thursday. The benchmark 2-year T-note last Friday closed at 1.19%, which translates to an inflation-adjusted yield of -0.82% against the current 2-year breakeven inflation expectations rate of 2.01%.

The 12-auction averages for the 2-year are as follows: 2.69 bid cover ratio, $168 million in non-competitive bids, 3.7 bp tail to the median yield, 15.9 bp tail to the low yield, and 58% taken at the high yield. The 2-year is the least popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buying, have taken an average of only 42.6% of the last twelve 2-year T-note auctions, well below the average of 59.1% for all recent Treasury coupon auctions.

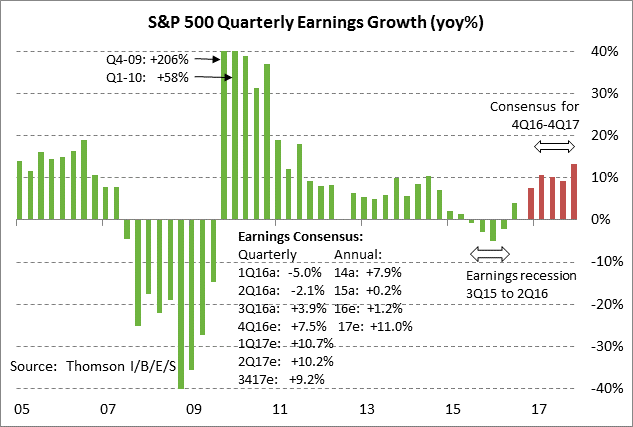

Favorable Q4 earnings season winds down with focus on retailers — Q4 earnings season is winding down with 50 of the S&P 500 companies scheduled to report this week. Notable reports this week include Wal-Mart, Home Depot, and Macy’s today; HP and L Brands on Wednesday; and Kohls, GAP and Nordstrom on Thursday.

The market consensus is for Q4 SPX earnings growth of +7.5% y/y, according to surveys by Thomson I/B/E/S. Q4 earnings have so far been positive with 68.7% of the 409 reporting SPX companies having beaten earnings expectations, mildly above the long-term average of 64.0% but below the 4-quarter average of 71%. Regarding revenue, only 49.8% of reporting SPX companies have beaten revenue expectations, below the long-term average of 59% and the 4-quarter average of 51%.

Looking ahead, the market is expecting a sharp pickup in earnings growth in 2017 with growth of +10.7% in Q1, +10.2% in Q2, +9.2% in Q3, and +13.3% in Q4. On a calendar year basis, the market consensus is for an improvement in SPX earnings growth to +11.0% in 2017 from the paltry growth rates seen in the last two years (i.e., +0.2% in 2015 and +1.2% in 2016). SPX earnings growth just turned positive in the second half of 2016 after the earnings recession seen from mid-2015 through mid-2016.