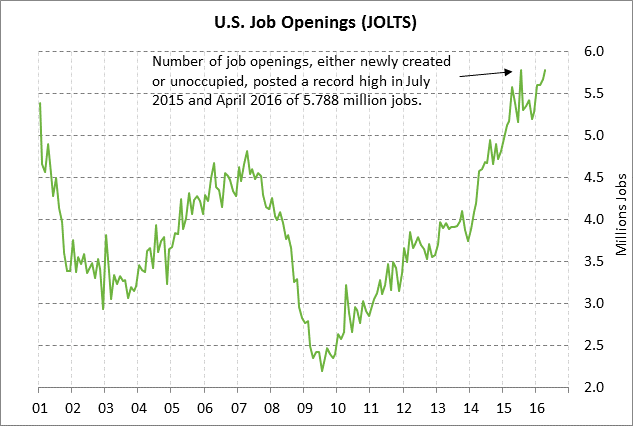

- JOLTS job openings expected to fall back from record high

- 10-year T-note auction to yield near 1.43%

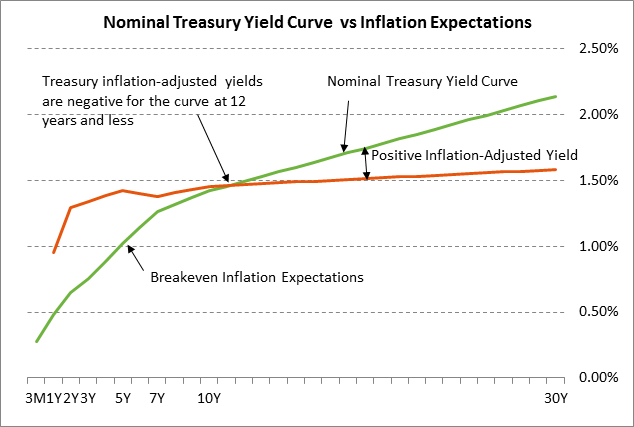

- Treasury curve of 12 years and less is below water

- Brexit process can move along more quickly with Theresa May becoming PM by Wed

- Abe victory ensures new fiscal stimulus

- Weekly EIA report

JOLTS job openings expected to fall back from record high — The market is expecting today’s May JOLTS job openings report to show a sharp decline of -288,000 to 5.500 million, more than reversing April’s +118,000 increase that matched the record high of 5.788 million originally posted in July 2015. The JOLTS job openings report is a leading indicator for the payroll figures since it provides the number of job openings available in the economy, most of which should eventually turn into actual job hires.

After a sharp -224,000 decline in Nov 2015, the JOLTS job openings series rose over the next five consecutive months (Dec-April) by a total of +590,000 to match the record high. The markets will be carefully watching today’s report to make sure that the sharp Dec-April rise in job openings wasn’t a fluke and that job openings remain strong. The markets were much more encouraged about the hiring situation after last Friday’s June payroll report of +287,000, which was far above market expectations of +180,000. Still, the 2-month average for May-June was weak at +147,000, which suggested that U.S. hiring has downshifted.

Slower payroll growth would not be surprising since (1) the U.S. economy is now near full employment, (2) businesses need to cut expenses in the midst of a year-long profit recession, and (3) businesses have reduced incentives to engage in new hiring with weak U.S. and overseas growth and with poor labor productivity and rising wages. However, if payroll growth can hold up near +175,000, the markets will be generally satisfied that the labor market is strong enough to keep supporting consumer confidence, income, and spending.

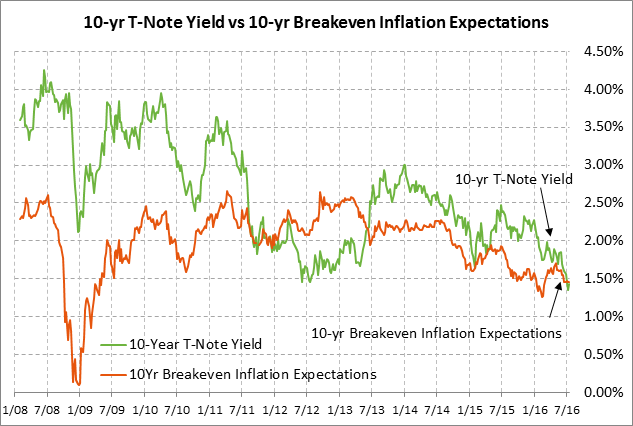

10-year T-note auction to yield near 1.43% — The Treasury today will sell $20 billion of 10-year T-notes in the second reopening of the 1-5/8% note of May 2026. The Treasury will then conclude this week’s $56 billion coupon package by selling $12 billion of reopened 30-year T-bonds on Wednesday.

Today’s 10-year T-note issue was trading at 1.43% in when-issued trading late yesterday afternoon, which translates to an inflation-adjusted yield of -0.03% against the 10-year breakeven inflation expectations rate of 1.46%. That means that investors, in return for locking up their cash in a T-note security for 10 years, can expect to lose -3 bp annually on their investment on an inflation-adjusted basis over the next 10 years if actual inflation ends up matching current 10-year inflation expectations of 1.46%.

The 12-auction averages for the 10-year are as follows: 2.63 bid cover ratio, $23 million in non-competitive bids, 4.4 bp tail to the median yield, 12.4 bp tail to the low yield, and 40% taken at the high yield. The 10-year is the second most popular security among foreign investors and central banks behind the 10-year TIPS security. Indirect bidders, a proxy for foreign buying, have taken an average of 63.1% of the last twelve 10-year T-note auctions, which is well above the average of 57.4% for all recent Treasury coupon auctions.

Treasury curve of 12 years and less is below water — In a remarkable development, the Treasury yield curve of 12 years and shorter is trading below inflation expectations. That is an unsustainable situation over the long run since investors will not buy securities forever in which they expect to lose money on an inflation-adjusted basis. Nevertheless, the current situation could last a matter of years since U.S. Treasury yields are being held down artificially by an extraordinarily easy Fed policy and by strong demand from overseas investors who face near-zero or negative sovereign yields at home.

Brexit process can move along more quickly with Theresa May becoming PM by Wed — The markets were pleased that Theresa May will become the new prime minister as early as Wednesday after her opponent, Energy Minister Andrea Leadsom, quit her challenge and eliminated the need for a full party member vote, which would have taken until September. The question now becomes when Ms. May might invoke Article 50 of the Lisbon EU Treaty to provide notice that the UK intends to leave the EU. Once the UK Article triggers Article 50, then the 2-year period will begin for negotiations, after which the UK can be expelled from the EU whether there is an exit agreement or not. The markets would like to get that 2-year period going as soon as possible. However, Ms. May earlier said she might not trigger Article 50 until next year.

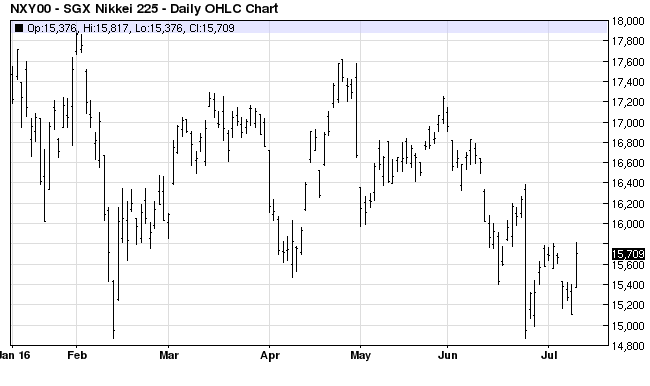

Abe victory ensures new fiscal stimulus — The Nikkei index on Monday rallied sharply by +4% after Prime Minister Abe’s ruling LDP party won a convincing victory in Sunday’s upper house election, thus ensuring that PM Abe can focus on new stimulus measures to help the economy. Mr. Abe on June 1 said that he will take “broad, bold” measures to support the economy that will include delaying the planned sales-tax increase. There have been reports that a new fiscal stimulus package could be as large as 20 trillion yen ($200 billion) in the current fiscal year. The new stimulus package could be announced as early as today. The LDP party won 56 of the 121 upper house seats in contention, giving Mr. Abe a ruling supermajority after including uncontested seats and the 14 seats won by junior coalition partner Komeito.

Weekly EIA report — The market consensus for Wednesday’s weekly EIA report is for a -3.5 million bbl decline in U.S. crude oil inventories, a -62,000 bbl decline in Cushing crude oil inventories, a -1.0 million bbl decline in gasoline inventories, unchanged distillate inventories, and a +0.5 point rise in the refinery utilization rate to 93.0%.