- Markets will remain on edge through Brexit vote

- Housing starts expected to show small decline but remain generally strong

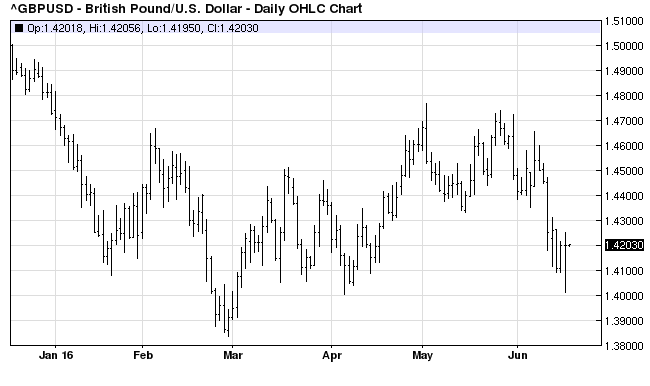

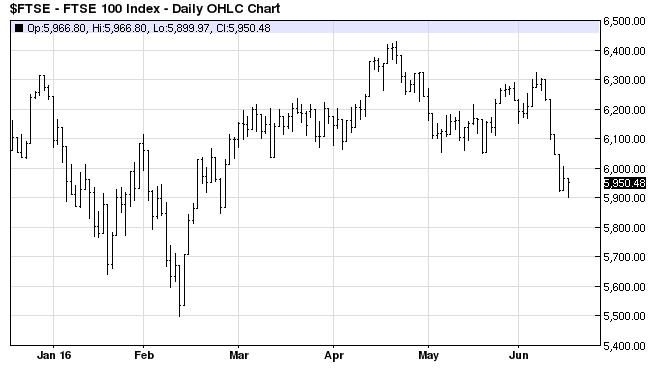

Markets will remain on edge through Brexit vote — The global markets in the past two weeks have become much more worried about next Thursday’s Brexit vote as the polls show that the “Leave” vote has gained momentum in the past two weeks. So far in June, sterling is down by -2.9% against the dollar and by -3.7% against the euro, and the UK FTSE 100 stock index is down -5.1%. In addition, the iShares MSCI European Financial ETF is down -9.4% so far in June and the EuroStoxx 600 Banks Index is down -15.8% at a 4-year low, illustrating the downward pressure on European banks from the Brexit threat.

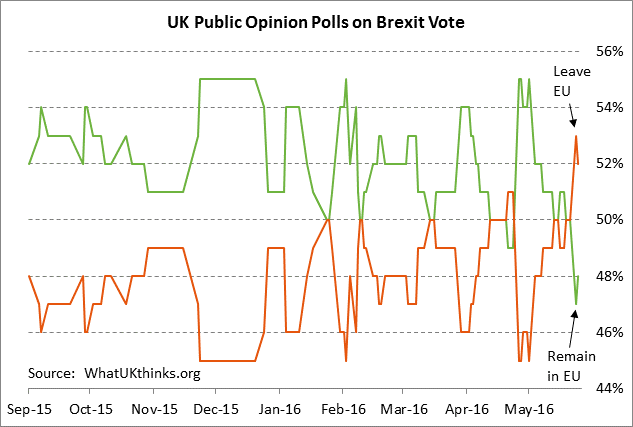

Recent public opinion polls have given a slight advantage to the “Leave” although some still have the “Remain” vote in the lead. The “poll of polls” run by WhatUKThinks.org currently has the Leave camp ahead at 52% versus 48% for the Remain camp.

Meanwhile, the betting odds still heavily favor the “Remain” outcome with oddschecker.com showing an average betting line of 11/18 (62% probability) for “Remain” versus 13/8 (38%) for Leave. While a 62% outcome for “Remain” is still fairly strong, it is down from 78% as recently as May 23. The Leave odds have risen sharply from 22% on May 23 to the current level of 38%. Bettors continue to believe that the public opinion polls are simply wrong.

Even though the polls are tight, the Remain faction hopes that there will be a last-minute break among undecideds to Remain as people get cold feet about the unknown outcome of Brexit. Yesterday’s shocking murder of UK MP Jo Cox may also cause a last-minute break to the “Remain” status quo. A last-minute swing to the safety of the status quo would be similar to what happened with the Scottish independence vote in 2014 when Scotland voted to stay in the UK by the fairly wide margin of 55%-45%. The undecided vote on the Brexit remains very large at 15% of voters, according to a YouGov survey, and the undecideds will clearly determine the outcome of the referendum.

If the UK does vote to leave the EU, then a UK recession seems likely due to post-EU business and consumer uncertainty, a steep drop in business investment in the UK, and an outflow of businesses from the UK to remain within the EU trading bloc. The BOE on Thursday in its post-policy-meeting statement said that Brexit may mean “a materially lower path for growth and a notably higher path for inflation” as well as a rise in unemployment. The BOE also said that, “The outcome of the referendum continues to be the largest immediate risk facing U.K. financial markets, and possibly also global financial markets.” UK Chancellor of the Exchequer George Osborne said this week that reduced trade and investment from Brexit would leave a 30 billion pound “black hole” in the UK budget that would have to be filled by either higher taxes or cuts in health, education, and defense spending.

The markets are worried about what Brexit might do to the UK economy and banking system but they are even more worried about what Brexit might mean for Europe. Deutsche Bank Chairman Paul Achleitner made an apt comment this week by saying that Brexit would be an “economic disaster for the UK and a political disaster for the EU.” The Eurozone can ill-afford any fresh political forces that might result in the Eurozone finally spinning apart altogether. The ECB managed to contain the Eurozone debt and banking crisis but Brexit could cause the situation to start slipping away from the ECB again if investor confidence is sufficiently shaken.

The good news is that the UK has its own currency and is not part of the Eurozone, meaning Brexit would not involve a Eurozone country giving up the euro to return to its own currency. A country exiting the Eurozone would represent a much more serious threat to Europe. A Brexit vote would simply result in a downgrade of the UK’s trade, labor, and immigration relationship with Europe. On that basis, a Brexit vote in theory should be a relatively localized event that shouldn’t have major global repercussions.

However, the global economy remains wounded and investor confidence is very brittle, meaning it might not take much to kick off another crisis in investor confidence. In any event, after next Thursday’s Brexit vote occurs, the markets will at least know one way or another whether the UK will be leaving the EU and investors will be able to quickly gauge the extent of the fall-out.

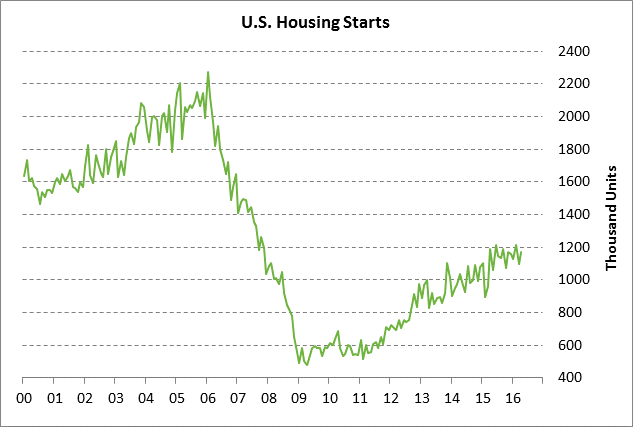

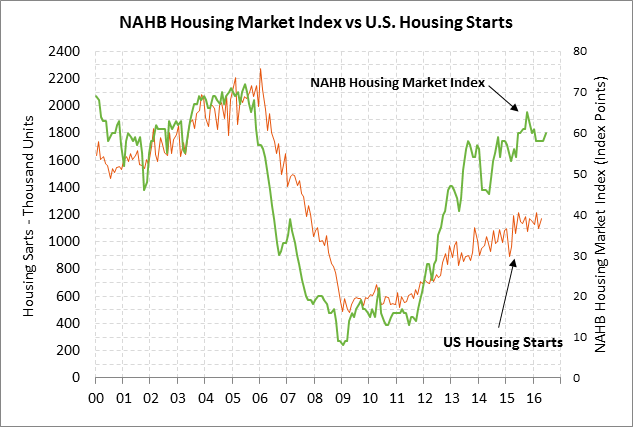

Housing starts expected to show small decline but remain generally strong — The market is expecting today’s May housing starts report to show a -1.9% decline to 1.150 million, giving back part of April’s +6.6% increase to 1.172 million. May building permits, by contrast, are expected to rise by +1.3% to 1.145 million, adding to April’s +4.9% increase to 1.130 million and providing some positive leading indicator data for housing starts in June and July. Yesterday’s June NAHB housing market index rose by +2 points to 60, which is only 5 points below the 10-year high of 65 posted in Oct 2015, indicating that U.S. home builder confidence strengthened in June.

The U.S. housing starts series is in generally strong shape considering that the April level of 1.172 million units was only -3.4% below the 8-1/2 year high of 1.213 million units posted in June 2015. Housing starts continue to see support from low mortgage rates, strong home sales, the tight supplies of new homes on the market, and rising new home prices for buildings.