- Weekly global market focus

- Fed chair announcement could come at any time

- T-notes remain on the defensive

- Stocks remain strong on tax reform boost

Weekly global market focus — The U.S. markets this week will focus on (1) the possible announcement this week of President Trump’s choice of the next Fed chair, (2) any progress on tax reform as the House may simply pass the same 2018 budget resolution that the Senate passed last Thursday as the legislative vehicle for tax reform, (3) any new provocations from North Korea, (4) the peak Q3 earnings week with 186 of the S&P 500 companies scheduled to report, and (5) the Treasury’s sale of $103 billion of T-notes.

In Europe, the focus is on the Catalonia independence situation and on Thursday’s ECB meeting. The market consensus is that the ECB on Thursday will announce that it will continue its QE program in the first nine months of 2018 with monthly purchases of 30 billion euros, half the current amount of 60 billion euros. The ECB is also expected to leave open the option of continuing QE past Q3-2018 if necessary. The market consensus is that the ECB will not start raising interest rates until Q1-2019.

The Spanish Senate is expected to start meeting on Tuesday and vote on Thursday or Friday to approve Prime Minister Rajoy’s call for using Article 155 of the Spanish constitution to strip Catalonia of its regional autonomy and take direct control of the region. The Spanish government plans to sack the Catalan president and political leaders and call new elections within 6 months.

However, the Catalan parliament this week, before Article 155 is activated by the Spanish Senate, could declare independence. At that point, Prime Minister Rajoy might decide to arrest Catalan President Puigdemont, who could face up to 30 years in prison if convicted of rebellion.

The resolution of the Catalan independence movement by using Article 155 is arguably a positive outcome for the markets since it at least imposes a legal resolution of the matter even if that resolution isn’t accepted on the street.

In Asia, the focus in on Japanese Prime Minister Abe’s decisive victory in yesterday’s national election and on the conclusion midweek of the Chinese Communist Party Congress. The markets are waiting to see if Chinese President Xi Jinping launches any new initiatives such as a revived deleveraging campaign after he consolidates his power in the Party Congress.

Prime Minister Abe on Sunday appeared to maintain his party’s two-thirds super-majority in parliament, which was a strong outcome. The yen traded lower early Monday on the idea that PM Abe’s victory means that the BOJ will be able to maintain is super-easy monetary policy. The election outcome was also positive for Japanese stocks, although the Nikkei index has already rallied sharply by 11% in the past 6 weeks on expectations for a positive election showing by PM Abe. That means that the Japanese stock market could now be due for some corrective action.

Fed chair announcement could come at any time — President Trump this week could announce his pick for the new Fed chair position since it appears that he has finished interviewing candidates for the position. Mr. Trump in any case is expected to announce his decision by next Friday when he leaves for his Nov 3-14 Asian trip.

President Trump in an interview with Fox Business News taped last Friday for release on Sunday and Monday said that, “Most people are saying it’s down to two — Mr. Taylor and Mr. Powell. I also met with Janet Yellen, who I like a lot, I really like her a lot. So I have three people that I’m looking at, and there are a couple of others. I’d say I will make my decision very shortly.”

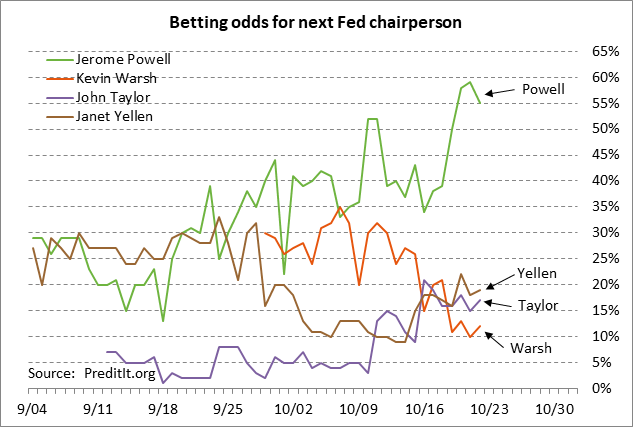

Fed Governor Powell last week became the clear leader in the betting odds at PredictIt.org after Politico’s report last Thursday that Mr. Powell is the “leading candidate” and he is favored by Treasury Secretary Mnuchin, who is leading the search. As of late Sunday afternoon, the odds were 55% for Powell, 19% for Yellen, 17% for Taylor, 12% for Warsh, and 4% for Cohn.

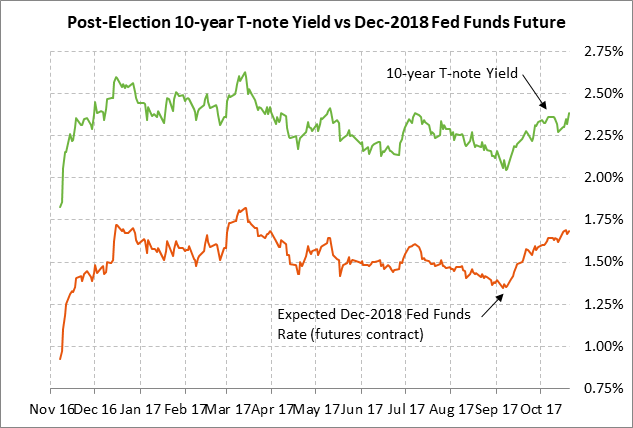

T-notes remain on the defensive — T-note prices remain on the defensive after the Senate made progress on tax reform last Thursday by passing a 2018 budget resolution. T-notes also remain on the defensive with (1) an almost-certain Fed rate hike in December, and (2) the continued possibility that President Trump could nominate noted hawk John Taylor as the new Fed chair. In addition, the 10-year breakeven inflation expectations rate last Friday rose by +1 bp to 1.87%, which is just -3 bp below the recent 5-1/2 month high of 1.90%.

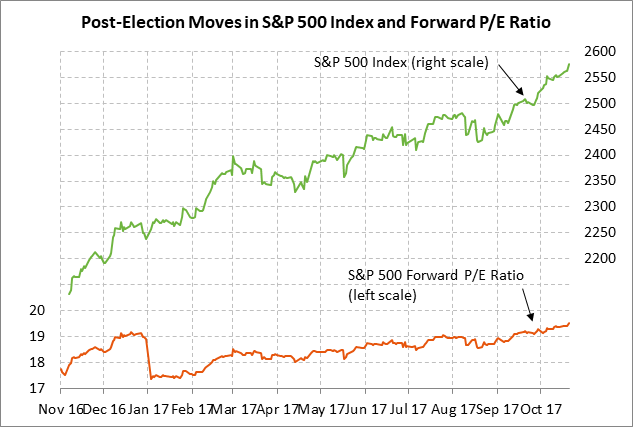

Stocks remain strong on tax reform boost — The S&P 500 index last Friday rallied to another new record high, supported by the improved chances for tax reform after the Senate’s passage late last Thursday of a 2018 budget resolution. Stocks also continue to see support from (1) generally firm U.S. economic data, (2) positive earnings expectations, and (3) carry-over support from strength in overseas stocks. On the negative side, interest rates are seeing upside pressure and valuations remain stretched with the SPX forward P/E last Friday reaching a new high for the year of 19.53.

This is the peak Q3 earnings week with 186 of the S&P 500 companies scheduled to report. Notable reports include AT&T, GM, Caterpillar on Tues; Boeing, Coca-Cola, Visa on Wed; and Alphabet, Amazon, Microsoft on Thursday. The market consensus is for Q3 SPX earnings growth to dip to +4.2% y/y from +10.1% in Q2, according to Thomson Reuters I/B/E/S. However, the consensus is for earnings growth to then improve to +12.5% in Q4 and +11.0% in Q1. On a calendar year basis, the consensus is for SPX earnings growth of +11.1% in 2017 and +11.7% in 2018.