- Weekly global market focus

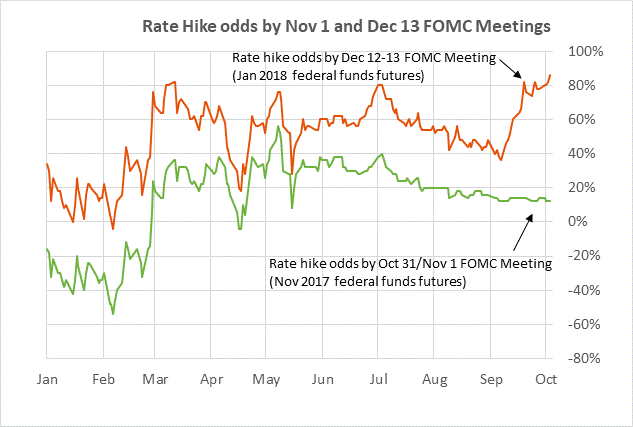

- T-note prices remain under pressure as Fed rate-hike expectations reach new high

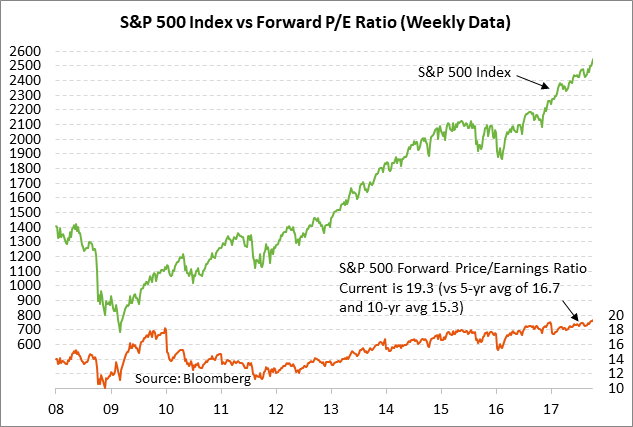

- Stock prices remain buoyant

Weekly global market focus — The U.S. markets this week will focus on (1) geopolitics as the markets wait to see if North Korea conducts another missile test, (2) any news on President Trump’s progress in choosing a new Fed chairperson, (3) the reaction of petroleum and natural gas prices after Hurricane Nate made landfall on Sunday near New Orleans as a Category 1 hurricane, (4) any progress by Republicans on formulating a tax reform package, (5) FOMC policy with the release of the Sep 19-20 meeting minutes on Wednesday and with nine different speaking engagements by Fed officials this week, (6) the Treasury’s sale on Wednesday and Thursday of $56 billion of 3, 10 and 30-year securities, and (7) the beginning of Q3 earnings week with 11 of the S&P 500 companies scheduled to report.

This week’s U.S. economic calendar is light with the focus on Friday’s Sep CPI and retail sales reports, which are both expected to be boosted by hurricane effects. Friday’s Sep CPI is expected to show an increase to +2.3% y/y from Aug’s +1.9% due to higher gasoline prices, and the core CPI is expected to edge higher to +1.8% y/y from Aug’s +1.7%. Friday’s Sep retail sales report is expected to surge by +1.6% m/m due to strong hurricane-related vehicle sales, but ex-autos sales are also expected to be strong at +0.9%.

The petroleum markets are on edge as President Trump is tentatively scheduled to give a speech on Thursday in which he will reportedly announce that he will refuse to certify Iran’s compliance with the nuclear agreement, a decision that must be made by this Sunday’s (Oct 15) deadline. Such a decision would open a 60-day window for Congress to vote to reimpose nuclear-related sanctions on Iran. However, Congress is not expected to reimpose those sanctions and is instead expected to simply let the 60-day period lapse, leaving the U.S. still firmly within the Iran nuclear deal. On a separate track, Mr. Trump could still effectively remove the U.S. from the Iran deal by refusing to waive sanctions against Iran by an upcoming deadline of Jan 12.

The European markets are on edge as they wait to see if Catalonia’s parliament will unilaterally declare independence when they are due to meet on the Tuesday. Catalonia’s parliament was originally scheduled to meet on Monday but Spain’s Constitutional Court blocked that session, prompting the delay until Tuesday. Over the weekend, there was a large public demonstration of several hundred thousand people against independence and a growing number of large banks and companies based in Catalonia are threatening to move their headquarters to ensure that they remain within the Spain and the EU. Catalan President Carles Puigdemont on Sunday said he will nevertheless move ahead with declaring independence. Spanish Prime Minister Rajoy has yet to indicate whether he will use a provision of the constitution to assume full political control of Catalonia and prevent any independence moves by the regional government, which could eliminate the short-term independence threat but could also cause civil unrest and stoke more resentment against the Spanish central government over the long run.

The Asian markets will focus on today’s reopening of the Chinese markets, which were closed all last week for the Golden Week holidays. The Hong Kong Hang Seng index, which was open three days last week, closed the week up +3.28%, which suggests that China’s mainland stocks today should play catchup with a rally. Chinese stocks in Hong Kong last week were boosted by the Oct 1 news that reserve requirements on Chinese banks will be reduced in 2018 based on a variety of criteria, which will free up bank lending capacity. Chinese economic reports this week include Thursday night’s Sep trade report (exports expected+9.8% y/y after Aug’s +5.6%) and Sunday’s Sep CPI (expected +1.6% y/y vs Aug’s +1.8%).

In Japan, the focus is mainly on politics and the future of Abenomics. Campaigning officially begins on Tuesday for the general election on Oct 22. The markets are waiting to see if Tokyo Governor Yuriko Koike will run for parliament under her Party of Hope banner, which would likely drain supporters away from Prime Minister Abe’s Liberal Democratic Party. The Japanese markets are closed on Monday for a national holiday.

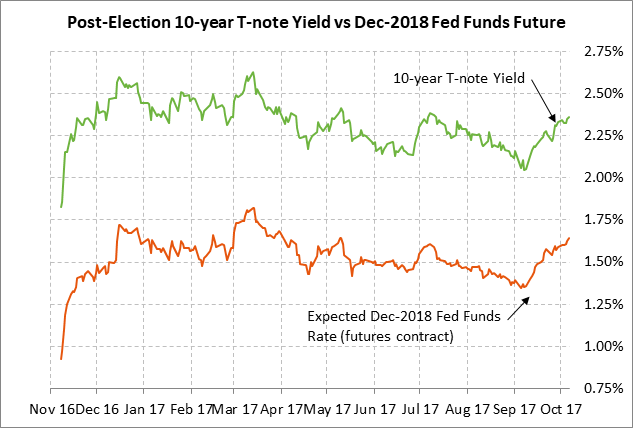

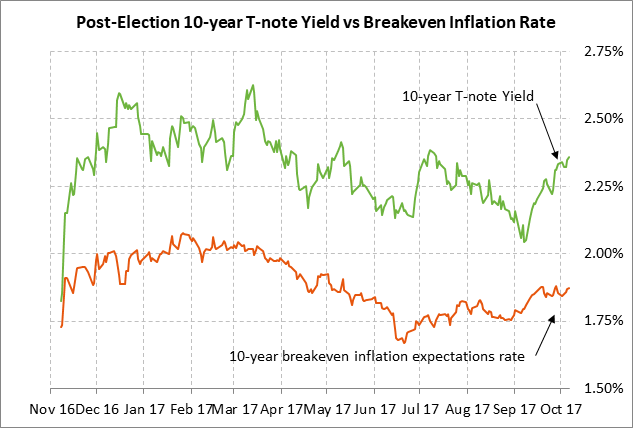

T-note prices remain under pressure as Fed rate-hike expectations reach new high — The 10-year T-note yield last Friday rose to a new 5-month high of 2.40% but then backed off to close the day up +2 bp at 2.36%. T-note prices were pressured mainly by Friday’s news that Sep average hourly earnings rose to +2.9% y/y, thus matching December’s 8-1/2 year high. If wages are starting to show the effects of a tight labor market, then the Fed will almost certainly move ahead with December’s rate hike. Friday’s -33,000 decline in Sep payrolls was largely ignored as the result of hurricane distortions since employment in the household survey surged by +906,000 and since the Sep unemployment rate fell to a new 17-year low of 4.2%. In another negative factor for T-note prices, the 10-year breakeven inflation expectations rate last Friday rose by +0.5 bp to 1.874%, which was just mildly below the late-Sep 5-month high of 1.89%.

Stock prices remain buoyant — The S&P 500 index last Thursday posted a new record high and closed just mildly below that level on Friday. The U.S. stock market continues to see underlying support from (1) optimism about the U.S. and global economies, and (2) strong earnings expectations. Stocks continue to shake off negative factors that include (1) high valuation levels with the SPX forward P/E at 19.31 (vs the 5-year average of 16.7 and the 10-year average of 15.3), and (2) the Fed’s hawkish policy intentions. The main focus is now on Q3 earnings season with notable reports this week including JP Morgan Chase and Citigroup on Thursday and Bank of America and Wells Fargo on Friday. Q3 earnings growth is expected at 4.9%, according to Thomson I/B/E/S.