- U.S. unemployment report will be mostly overlooked due to hurricane distortions

- Republicans make progress on tax reform vehicle

U.S. unemployment report will be mostly overlooked due to hurricane distortions — Today’s Sep unemployment report will be mostly overlooked by the markets due to the substantial disruptions caused in September by Hurricanes Harvey and Irma. Harvey made landfall in Texas on Aug 25 and Irma made landfall in Florida on Sep 10.

The market consensus is for a +80,000 increase in Sep payrolls, which would be well below Aug’s +156,000 and the 12-month trend average of +175,000. Wednesday’s Sep ADP report of +135,000, however, suggested that today’s payroll report may not be as weak as the consensus. The markets will be waiting to see if the Labor Dept in the unemployment report takes a stab at quantifying the number of job losses related to hurricane disruptions, although that is probably too difficult to discern at this point.

Regardless of today’s payroll figure, job growth should rebound fairly quickly in the next few months as businesses return to normal and as new jobs emerge for hurricane cleanup and rebuilding efforts.

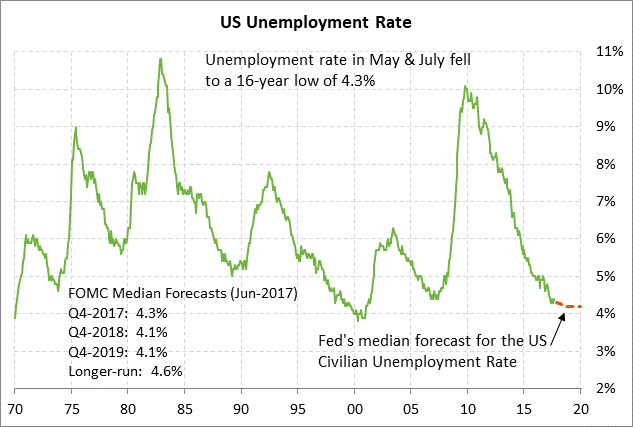

Meanwhile, today’s Sep unemployment rate is expected to be unchanged from Aug at 4.4%. The expected report of +4.4% would be just +0.1 point above the 16-year low of 4.3% posted earlier this year in May and July. The unemployment rate has already nearly fallen to the Fed’s forecast for an unemployment rate of 4.3% for late this year and of 4.1% in 2018-2019. In addition, the current unemployment rate of 4.4% is already below the Fed’s longer-run natural unemployment rate of 4.6%, which indicates that the Fed believes that the labor market is already tight and should be putting upward pressure on wages.

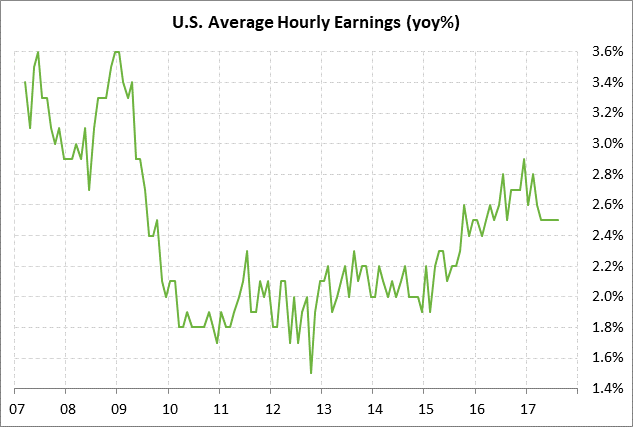

On the wage front, the consensus is for today’s Sep average hourly earnings report to show an increase of +0.3% m/m and +2.5% y/y following the Aug report of +0.1% m/m and +2.5% y/y. Wage growth has been stuck at +2.5% for the past five consecutive reporting months, down from the 8-year high of +2.9% y/y posted in Dec 2016. The Fed continues to be flummoxed by the lack of wage pressures despite the tight labor market.

Today’s hurricane-impacted labor market data is not likely to have much impact on the Fed’s near-term policy decisions. The market is discounting a negligible 12% chance of a Fed rate hike at its next meeting on Oct 31/Nov 1 since there will be no press conference by Fed Chair Yellen after that meeting. However, the market is discounting a substantial 86% chance of a Fed rate hike at the following meeting on Dec 12-13, which will, in fact, be followed by a Yellen press conference.

Republicans make progress on tax reform vehicle — Republicans on Thursday made progress on the tax reform process after the House approved a 2018 budget resolution, which will be the legislative vehicle for passing tax reform through the reconciliation process that sidesteps the possibility of a Senate Democratic filibuster. Meanwhile, the Senate Budget Committee on Thursday approved the Senate’s version of the budget resolution, which is expected to come to the Senate floor for a vote within the next two weeks or so. The two bills will then have to be reconciled into a single compromise bill and passed by both the House and the Senate.

The budget resolution by itself is non-binding and has little importance other than acting as the vehicle for tax reform. Senator Bob Corker this week noted that the budget resolution “is always a joke” and isn’t “worth the paper it’s written on.” But he added, “this is a vehicle to begin a debate on tax reform.” Regarding actual spending authority, the crunch will come on Dec 8 when the current continuing resolution expires and new spending authority will need to be passed to prevent a government shutdown.

On the tax reform bill itself, Congressional committees and Republican leaders are trying to grind out a package that satisfies the demands of all the factions within the Republican party. The discussion at present is focused on the extent to which the deduction for state and local taxes, which is worth $1.2 trillion over 10 years, can be eliminated to make room for tax cuts. The stock market will not be happy with the watering-down of pay-fors since that reduces the likelihood that the corporate tax rate can be cut as low as the intended target of 20%.

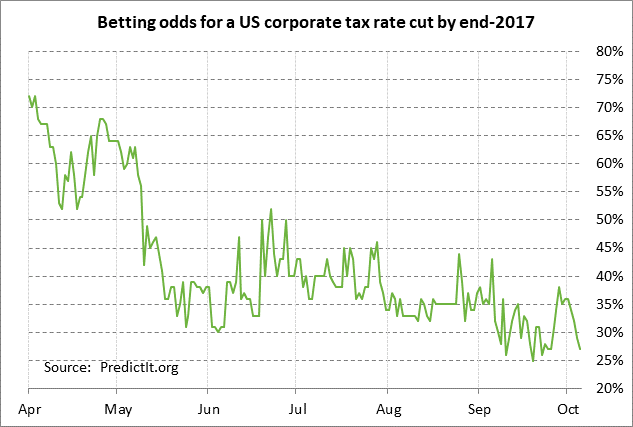

Even though Republicans have now launched their tax reform effort, the betting odds are still relatively dim for a deal by year-end. The betting odds at PredictIt.org are at only 27% for a corporate tax cut by year-end, which is just above the record low of 25% posted in mid-September. Bettors seem to believe that Republicans will get bogged down on tax reform as they did on healthcare due to factional infighting, or at least that a deal will not get done until 2018.

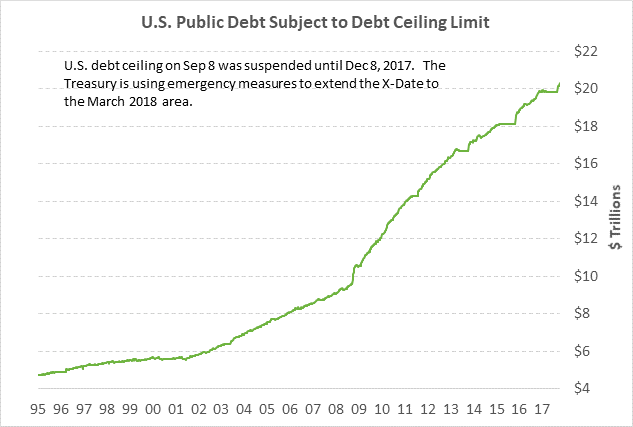

In any case, we believe the odds of a corporate tax cut by early 2018 are fairly good simply because passing a tax bill has become an existential issue for Republicans after their failure to repeal Obamacare. However, the final bill may disappoint the markets since it is likely to involve smaller-than-expected, and temporary, tax cuts due to (1) the difficulty of agreeing on pay-fors, and (2) demands by deficit hawks to avoid completely exploding the federal budget deficit. The U.S. national debt just went above $20 trillion and is likely to accelerate higher under the tax reform plan that is currently under consideration.