- SPX record high keeps valuations stretched

- ADP U.S. employment expected to be only temporarily undercut by hurricane forces

- U.S. ISM non-manufacturing index expected to edge higher

- Weekly EIA report expected to move closer to normalcy

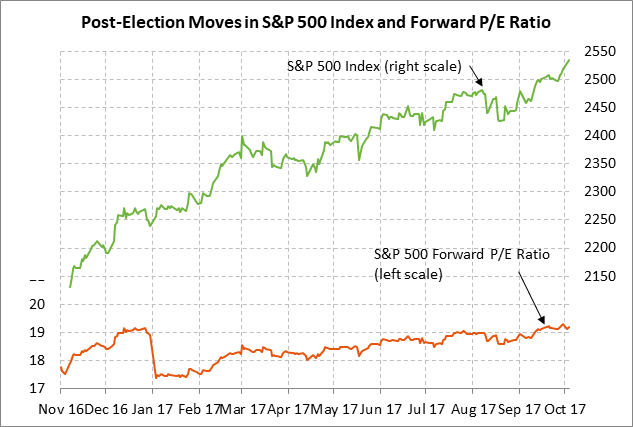

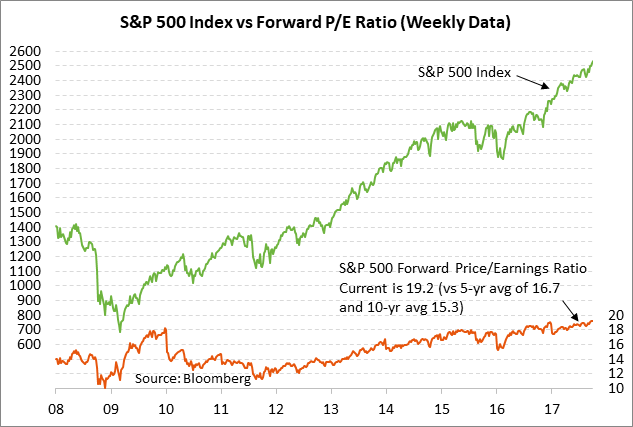

SPX record high keeps valuations stretched — The S&P 500 index on Tuesday extended its week-long upside breakout and posted a new record high, closing the day up +0.22%. The rally in stocks pushed the forward P/E for the S&P 500 index on Tuesday to 19.18, which was just below last Friday’s peak of 19.29. Last Friday’s forward P/E of 19.29 was the highest level in 15-1/2 years, i.e., since the dot.com era. This particular forward P/E figure is based on expected earnings for the calendar year of 2017.

The U.S. stock market continues to see strong support from (1) expectations for SPX earnings growth of about +11% in both 2017 and 2018, (2) expectations for an eventual corporate tax cut, (3) the firm U.S. economy and the much-improved global economy, (4) expectations for U.S. interest rates to remain generally low despite the Fed’s slow rate-hike regime, and (5) this year’s weakness in the dollar that has given exports and overseas earnings an upward bump.

High valuation levels are usually offered as a reason why stock prices should fall. However, there is also the possibility that stock prices could move sideways or even mildly higher, with the P/E ratio eventually coming down as earnings growth catches up with stock prices. In any case, there is little doubt that the stock market is priced for perfection and that the market is vulnerable on the downside to any sudden disappointments.

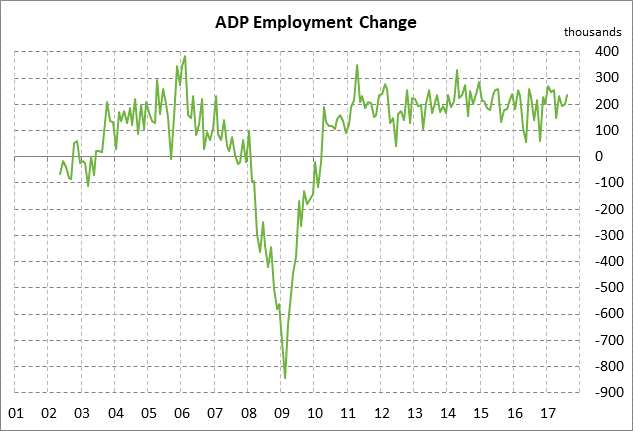

ADP U.S. employment expected to be only temporarily undercut by hurricane forces — The market consensus is for today’s Sep ADP employment report to show an increase of +143,000, down from August’s strong report of +237,000 and well below the 12-month trend average of +204,000. Today’s Sep ADP jobs figure will take a hit from Hurricanes Harvey and Irma, thus reducing its importance. However, job growth should quickly rebound due to the strong underlying jobs trend and due to increased employment for hurricane repairs. On the jobs front, the markets are eagerly awaiting Friday’s Sep unemployment report, which is expected to show a weak payroll increase of +80,000 and an unchanged unemployment rate of 4.4%.

The Fed will be looking past hurricane effects. The hurricanes are unlikely to deter the Fed from its apparent determination to raise the funds rate for the third time this year in December. The markets will be listening to Fed Chair Yellen’s speech this afternoon (3:15 PM ET) at a community banking conference in St. Louis to see if she has any comments on monetary policy. The markets are currently discounting the odds at 78% for a rate hike at the December 12-13 FOMC meeting, just slightly below the recent peak of 82%.

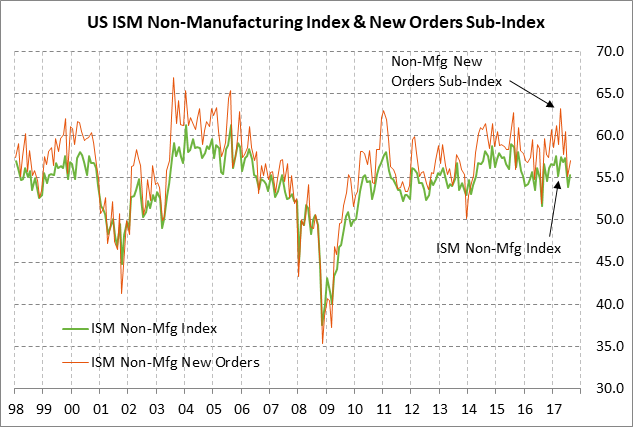

U.S. ISM non-manufacturing index expected to edge higher — The market consensus is for today’s Sep ISM non-manufacturing index to show a +0.2 point rise to 55.5, adding to Aug’s +1.4 point increase to 55.3. The index is in relatively strong shape at only -2.3 points below the 1-3/4 year high of 57.6 posted in February, illustrating optimism in the non-manufacturing sectors of the U.S. economy.

Today’s ISM non-manufacturing index is not likely to take much of a hit from Hurricanes Harvey and Irma considering that this past Monday’s ISM manufacturing index for September rose by a stronger-than-expected +2.0 points to post a new 13-year high of 60.8. U.S. business confidence remains strong due to (1) solid U.S. economic data, (2) much-improved overseas economic growth, (3) record highs in the U.S. stock market, and (4) hopes for corporate and personal tax cuts.

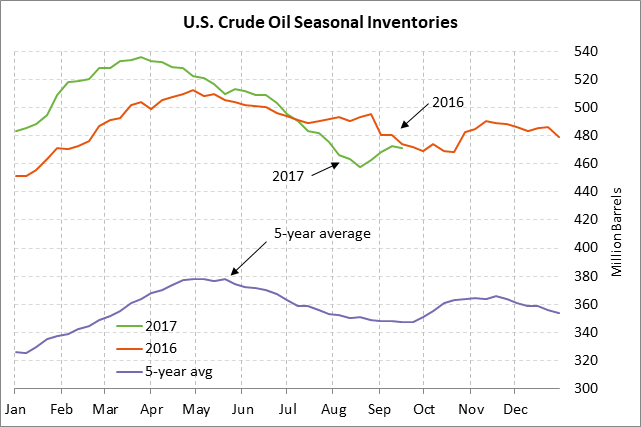

Weekly EIA report expected to move closer to normalcy — The market consensus for today’s weekly EIA report for the week ended Sep 29 is for a -500,000 bbl decline in U.S. crude oil inventories, a +1.0 million bbl rise in gasoline inventories, a -1.5 million bbl decline in distillate inventories, and a +0.8 point increase in the refinery utilization rate to 89.4%.

The U.S. petroleum data should be getting closer to normal now that it has been more than a month since Hurricane Harvey devastated the Texas oil industry. The refinery utilization rate has bounced back by +10.9 percentage points in the past two reporting weeks to 88.6%, but still has at least several points left to go to get back to normal seasonal levels. Refineries in other areas of the country have been running at full tilt and some have delayed maintenance in order to take advantage of the wide crack profit margins.

The recovery in refinery activity will boost crude oil demand and gasoline production, thus cutting crude oil inventories and boosting gasoline inventories. Gasoline inventories are currently mildly tight at -4.4% below the 5-year seasonal average, while crude oil inventories are +24.6% above average, higher than the +19.7% level seen just before Harvey made landfall on Aug 25.

U.S. oil production last week rose by +0.4% to a new 2-1/4 year high of 9.547 million bpd. U.S. oil production is likely to see some new upward movement in response to the recent surge in Nov WTI oil prices to a new 5-1/2 month nearest-futures high of $52.86 per barrel last week, although prices have since settled back to $50.42. Baker Hughes reported last Friday that the number of active oil rigs last week rose by 6 rigs to 750 rigs, the first increase in six weeks.