- Weekly global market focus

- U.S. ISM manufacturing index expected to back off from Aug’s 6-1/4 year high on hurricane disruptions

- T-note prices remain on the defensive

- Stock market sees continued support from tax cut hopes

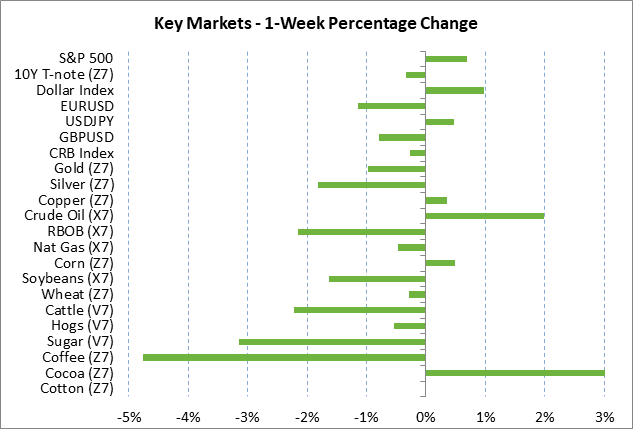

Weekly global market focus — The U.S. markets this week will focus on (1) Friday’s Sep payroll report (expected +85,000), which will see hurricane disruptions, (2) Fed policy as a raft of Fed officials speak this week, including Fed Chair Yellen on Wednesday, and as the Trump administration steps up its selection process for the next Fed chairperson, (3) any progress in Congress on the Republicans’ tax reform plan and on passing the 2018 budget resolution, (4) ongoing North Korean tensions as Secretary of State Tillerson said that the U.S. is now talking directly with North Korea, (5) Nov oil prices, which rallied by another +1.99% last week and kept upward pressure on inflation expectations, and (6) another light earnings week with only 8 of the S&P 500 companies schedule to report.

President Trump said last Friday that he will be making a decision over the next 2-3 weeks on who will be the next Fed chairperson. The markets were undercut last Friday by news that Mr. Trump interviewed former Fed Governor Kevin Warsh for the position, whom the markets believe would be more hawkish than Ms. Yellen. Mr. Trump has so far also interviewed Ms. Yellen, Gary Cohn, and Fed Governor Jerome Powell. The betting odds for the next Fed chair, according to PredictIt.com, are as follows: Kevin Warsh 31%, Jerome Powell 25%, Janet Yellen 18%, Gary Cohn 14%, John Taylor 6%, Glenn Hubbard 2%, John Allison 2%, and Larry Lindsey 1%.

The U.S. House of Representatives this week is expected to approve the 2018 budget resolution that will be the legislative vehicle for approving the eventual tax reform plan through the reconciliation process. The Senate Budget Committee this week will mark up the 2018 budget resolution, preparing for a floor vote. The resolution is non-binding and should be able to get approved by Congress without too much trouble, meaning the resolution’s importance for the markets is limited.

In Europe, the focus will be on (1) this week’s fairly busy economic calendar, (2) Thursday’s release of the account of the Sep 14 ECB meeting, (3) Spain’s crackdown over the weekend on the Catalan independence vote, (4) negotiations by Angela Merkel to form a new government after the Green Party on Saturday voted to allow its party leaders to negotiate participation in a new coalition government. The ECB at its meeting in three weeks (Oct 26) is expected to announce its plans for tapering its QE program in 2018. In the UK, the focus is on the Conservative Party’s 4-day annual conference that began yesterday and runs through Wednesday. The markets will continue to watch the interplay between Prime Minister May and her ministers on Brexit positions.

In Asia, the Chinese markets are closed this week for the mid-autumn festival holiday. There are now only 2-1/2 weeks until the twice-a-decade Party Congress begins on Oct 18 in which Chinese President Xi Jinping will consolidate his grip on power. Monday’s Japanese Q3 Tankan report is expected to show steady confidence among large manufacturers and a small improvement in confidence in the non-manufacturing industry. The Australian central bank is expected to leave its monetary policy unchanged at its meeting on Tuesday. India’s central bank at its meeting on Wednesday is also expected to leave its policy unchanged.

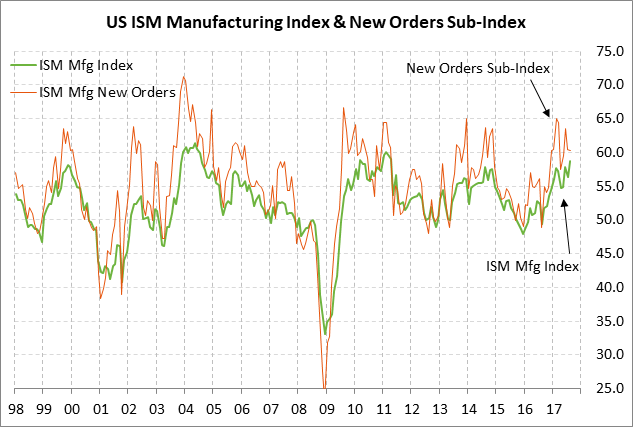

U.S. ISM manufacturing index expected to back off from Aug’s 6-1/4 year high on hurricane disruptions — The market consensus is for today’s Sep ISM U.S. manufacturing index to show a -0.8 point decline to 58.0, reversing about one-third of August’s +2.5 point increase to 58.8. Today’s ISM manufacturing index is expected to be dented by business disruptions from Hurricanes Harvey and Irma. However, manufacturing confidence is expected to remain generally strong, just below the 6-1/4 year high of 58.8 posted in August. U.S. manufacturing confidence remains strong due to the firm U.S. economy and strong overseas sales prospects due to the weak dollar and improved overseas growth. The ISM manufacturing new orders sub-index has fallen by -3.2 points in the last two months but remains strong at 60.3, which is just -4.8 points below the 8-year high of 65.1 posted in February.

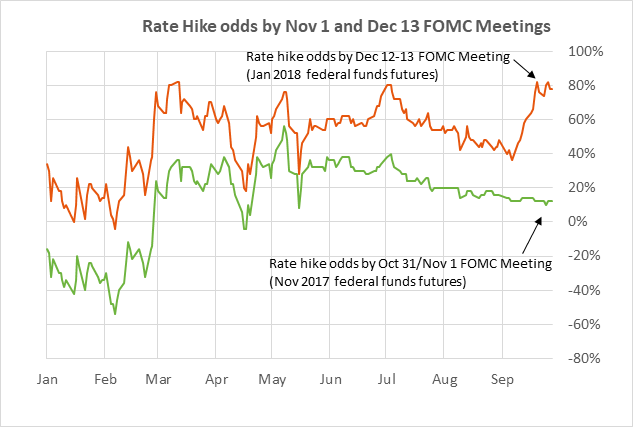

T-note prices remain on the defensive — Dec T-note prices last Thursday fell to a new 2-1/2 month low and closed the week near the bottom of the sharp month-long sell-off. T-note prices received some support from last Friday’s news that the Aug core PCE deflator eased to match the 6-1/4 year low of +1.3% y/y. Still, sentiment in the T-note market remains bearish due to (1) the Fed’s hawkish intent to raise interest rates again in December and three times in 2018, (2) this week’s beginning of the Fed’s balance sheet reduction program, and (3) the recent climb in U.S. inflation expectations sparked mainly by strong oil prices. The chances for a Fed rate hike by December were little changed last week at 78%, according to fed funds futures.

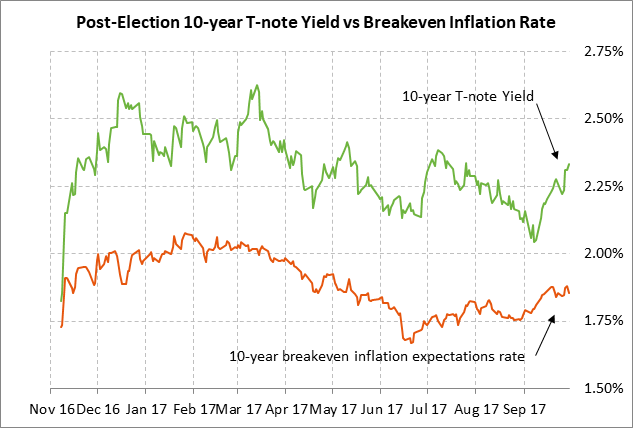

Stock market sees continued support from tax cut hopes — The stock market last week continued to see support from the increased chances for a corporate tax cut as Congress gets down to business on filling in the details of the plan. There was also some relief on the North Korean front last week after there were no new North Korean provocations. The stock market last week was largely able to shake off the bearish factors of (1) the new 1-1/2 month high in the dollar index and the +0.98% weekly close, and (2) the rise in the 10-year T-note yield to a new 2-3/4 month high and the +8 bp weekly close at 2.33%. The U.S. stock market is mainly focus on the Republican tax plan and on the upcoming Q3 earnings season where SPX earnings are expected to rise +6.2%, according to Thomson Reuters I/B/E/S.