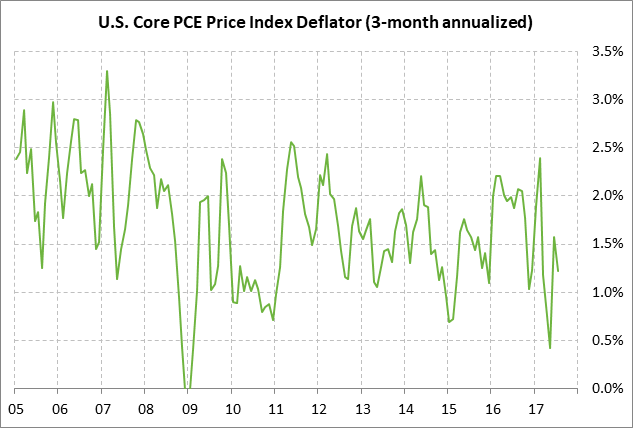

- Fed’s preferred inflation measure expected to tick higher but remain below target

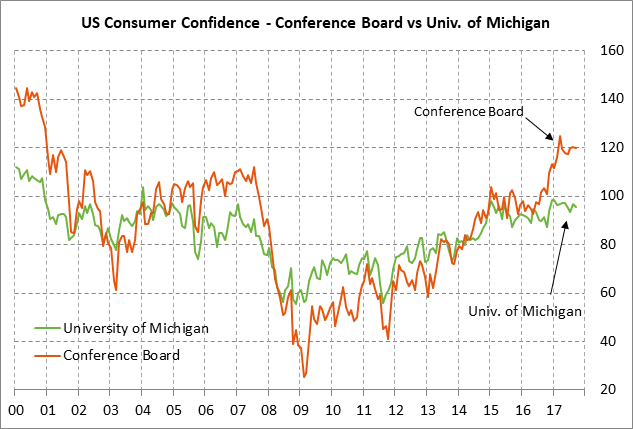

- Final-Sep U.S. consumer sentiment index expected to show no revision from -1.5 point drop

- T-note yields surge to 2-month high on inflation expectations, a tight Fed, and possible tax cuts

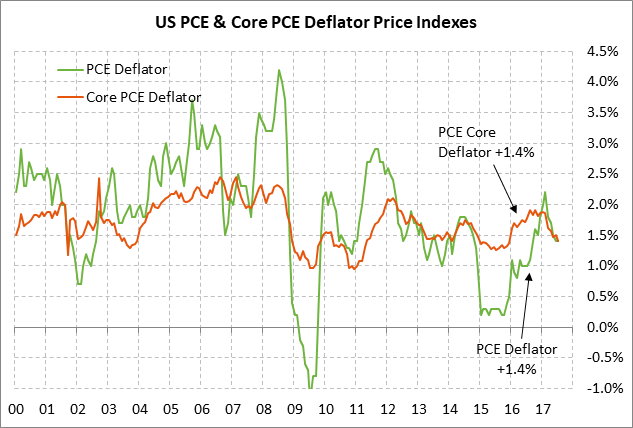

Fed’s preferred inflation measure expected to tick higher but remain below target — The market consensus is for today’s Aug PCE deflator to show a slight uptick to +1.5% y/y from July’s +1.4%, although the Aug core deflator is expected to be unchanged from July’s +1.4% y/y.

Both the headline and core deflators fell substantially this spring from the highs posted earlier this year. The headline deflator posted a 5-1/4 year high of +2.2% y/y in February and the core deflator posted a 5-year high of +1.9% in Jan-Feb. The decline in the deflators to the current level of +1.4% y/y leave the Fed’s preferred inflation measures well below the Fed’s medium-term inflation target of +2.0%.

The only good news for the Fed in meeting its +2.0% inflation goal is that the deflators likely bottomed out in June-July and might start to recover. Inflation will see some upward pressure over the near-term from (1) the +19% rally in WTI crude oil prices since June’s low, and (2) Hurricanes Harvey and Irma that will put some upward price pressure on recovery-related products and services. However, inflation in general is expected to remain tame in coming months, thus causing some Fed officials to remain reluctant to raise interest rates.

Final-Sep U.S. consumer sentiment index expected to show no revision from -1.5 point drop — The market consensus is for today’s final-Sep University of Michigan U.S. consumer sentiment index to be left unrevised from the early-Sep level of 95.3. That would leave the index down by -1.5 points from the August level.

Even after the early-Sep decline of -1.5 points to 95.3, the index remains in strong shape at only -3.2 points below the 13-1/2 year high of 98.5 posted in January. U.S. consumer sentiment took somewhat of a hit in early September due to Hurricanes Harvey and Irma and possibly due to North Korean tensions. However, U.S. consumer confidence in general remains strong due to (1) the firm labor market and economy, (2) record highs in the stock market, (3) rising consumer income, and (4) continued hopes for a personal tax cut.

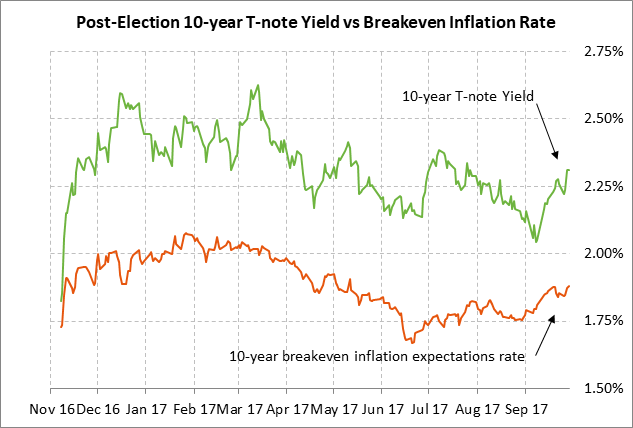

T-note yields surge to 2-month high on inflation expectations, a tight Fed, and possible tax cuts — The 10-year T-note yield in the past three weeks has surged by +30 bp to a 2-month high of 2.31% from the post-election low of 2.01% posted in early September. There may be some consolidation over the near-term, but we look for T-note yields to see continued upward pressure in coming weeks.

The 10-year T-note yield fell to a post-election low of 2.01% in early September as the market focused on (1) low inflation, (2) deferred expectations for Fed rate hikes, and (3) fears about hurricane damage. However, the T-note yield then surged as September wore on due to (1) rising inflation expectations, (2) less-than-expected hurricane damage, (3) the hawkish outcome of the Sep 19-20 FOMC meeting, and (4) revived talk about a Republican tax cut for either late this year or early 2018.

A key factor behind the September surge in T-note yields has been the sharp +14 bp rise in the 10-year breakeven inflation expectations rate to the current level of 1.88% from the 2-month low of 1.74% posted in late August. Inflation expectations have risen due to (1) September’s +8% rally in crude oil prices, (2) the rise in the Aug CPI to +1.9% y/y from June’s low of +1.6%, and (3) ideas that inflation will be pushed higher if Republicans are successful in approving a tax cut bill.

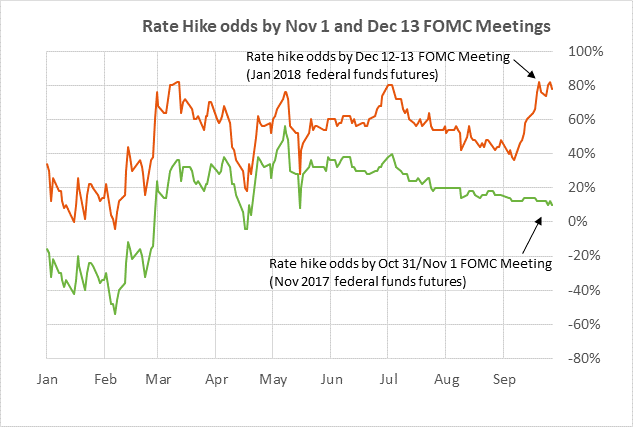

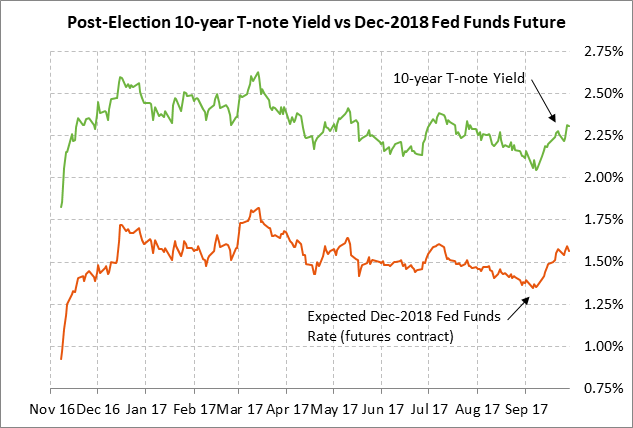

T-note yields have also been pushed higher by accelerated expectations for Fed rate hikes through 2018. The FOMC at its Sep 19-20 meeting reaffirmed the Fed-dot forecasts for another rate hike by December and three rate hikes in 2018. The chances for a Fed rate hike by this December have risen to the current level of 78% from a low of 36% in early September shortly before Hurricane Irma was about to hit Florida. The markets are now taking the Fed more seriously about its intent to execute its plan for four more rate hikes through the end of 2018 due to the rise in inflation expectations and the firm U.S. economy. U.S. GDP rose by +3.1% in Q2 and is expected to stabilize at a firm +2.2% in the second half of 2017.

T-note yields are also on the rise after the Fed confirmed an October start date for its balance sheet reduction program. The Fed has claimed that its program will be like watching paint dry, but the fact remains that the Fed is stepping back as a big buyer in the Treasury market, which means weaker overall demand for Treasury securities.

The 10-year T-note yield has also been pushed higher this week by increased optimism that Republicans might be able to pass a tax reform plan. The 9-page Republican plan was long on tax-cut details but short on the details about how to pay for those tax cuts, encouraging market ideas that Republicans will be tempted to rely in part on temporary 10-year tax cuts that allow a budget-busting tax plan. The U.S. national debt just moved above the $20 trillion level and will be headed much higher if the Republican tax plan isn’t deficit neutral. T-note yields may need to rise to lure investors into taking the higher risk of financing a U.S. national debt that is accelerating higher.