- Weekly global market focus

- Congress has tax reform and health care on this week’s busy agenda

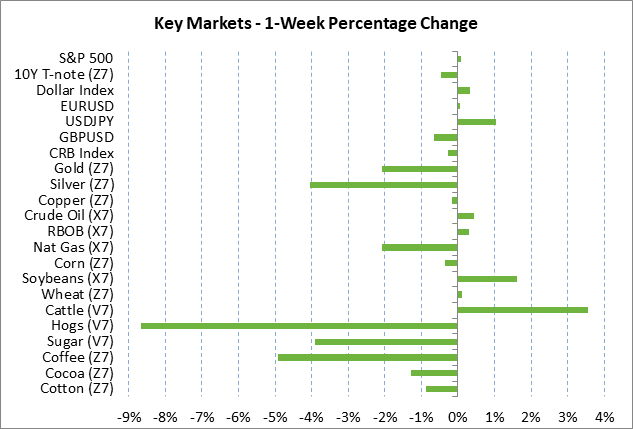

- T-note prices remain on the defensive after sharp 2-week sell-off

- U.S. stocks remain buoyant

- Merkel wins German election but faces a coalition-building challenge and new opposition from the right

Weekly global market focus — The U.S. markets this week will focus on (1) geopolitical concerns after the North Korean government late last week threatened to test a nuclear weapon in the Pacific ocean, which would represent a dangerous escalation of the crisis, (2) a heavy schedule of Fed speakers this week including Fed Chair Yellen on Tuesday with a keynote address at the NABE conference, (3) oil prices and any further strength in inflation expectations, (4) the Treasury’s sale of $101 billion of T-notes this week, (5) another light earnings week with reports from ten of the SPX companies, (6) this week’s new round of NAFTA talks in Ottawa, and (7) a busy U.S. economic calendar.

In Europe, the focus will be on (1) reaction to Sunday’s German election, (2) today’s comments by ECB President Draghi, and (3) the busy European economic schedule. Brexit talks are due to resume today. The UK markets today will react to the news late Friday that Moody’s downgraded the UK’s credit rating by one notch to Aa2 (two levels below triple A) due to the UK budget deficit and Brexit risks.

In Asia, the focus will be on expectations that Japanese Prime Minister Abe as soon as today may call a snap election, likely for late October. The Nikkei index last week rallied sharply to a new 2-year high due in part to hopes that Mr. Abe will be able to regain his political strength and continue to execute his stimulus and reform program.

In China, PMI reports will be released on Thursday and Friday. The markets are counting down to the National Party Congress that begins on Oct 18 where Chinese President Xi Jinping will further consolidate his power base and lay the groundwork for new initiatives later this year.

Congress has tax reform and health care on this week’s busy agenda — This will be a busy week for Congress during the last week of the fiscal year. The Senate has a deadline of this Saturday (Sep 30) to get an Obamacare repeal bill passed. Senate Majority Leader McConnell said last week that he plans to hold a vote this Wednesday on the Graham-Cassidy bill.

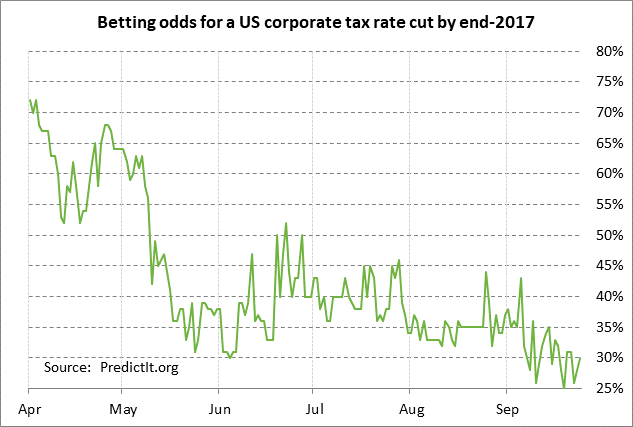

Regarding tax reform, Republican leaders have said that they will release their tax reform plan this week. Axios over the weekend reported that President Trump on Wednesday will give a speech in Indiana unveiling the Republican tax plan. The Washington Post last Friday night reported that the Republican plan contains a cut in the corporate tax rate to 20% from 35%, which would be better than talk of a cut to the mid-20’s. House Republicans plan to hold a half-day retreat on tax reform on Wednesday. The betting odds for a corporate tax rate cut by the end of 2017 remain low at 31%, according to PredictIt.org. Separately, Republicans this week will continue to work on trying to pass a nonbinding 2018 budget resolution that will provide the legislative vehicle for approving tax reform through the reconciliation process (which eliminates the threat of a Senate Democratic filibuster).

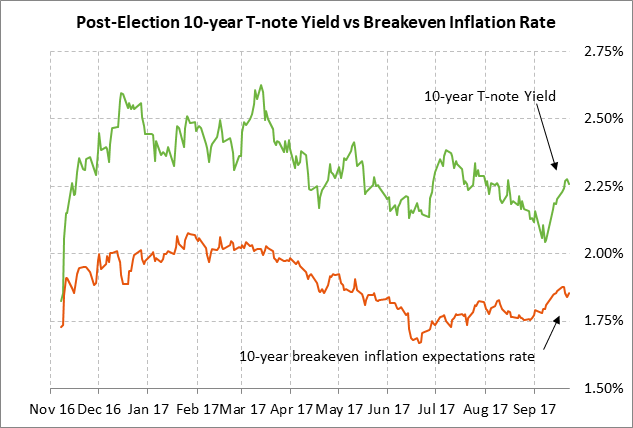

T-note prices remain on the defensive after sharp 2-week sell-off — T-note prices last week continued their sharp 2-week sell-off. The 10-year T-note yield last week rose by another +4.8 bp to 2.25%, adding to the previous week’s +15.2 bp surge. T-note prices have fallen sharply due to (1) increased expectations for Fed tightening, (2) some nervousness about the Fed’s balance sheet drawdown program that begins in October, and (3) a rise in inflation expectations.

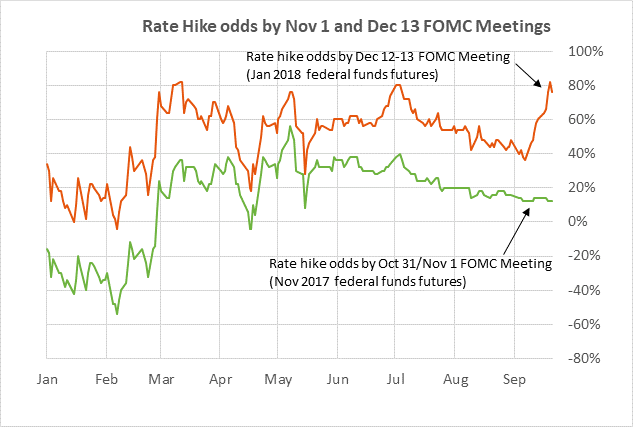

The odds for a Fed rate hike by December rose sharply to 76% last Friday (according to the Jan 2018 federal funds futures contract) from just 38% two weeks earlier due to (1) the recent rise in inflation expectations, and (2) the hawkish outcome of last week’s FOMC meeting after FOMC members left their Fed-dot forecasts unchanged for another rate hike by December and three rate hikes in 2018. Meanwhile, the 10-year breakeven rate has risen sharply by a net +10 bp in the past three weeks to 1.85% due to rising oil prices and the increase in the Aug CPI to +1.9% y/y from July’s +1.7%.

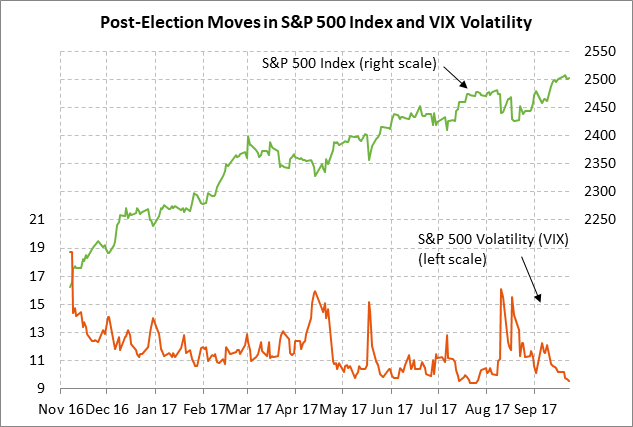

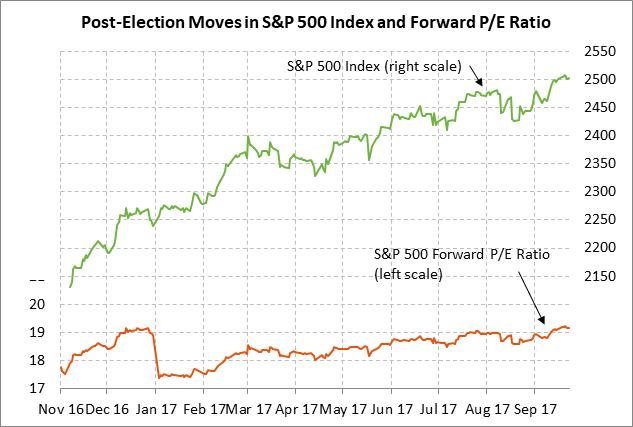

U.S. stocks remain buoyant — The S&P 500 index last Wednesday posted a new record high but closed the week just slightly higher by +0.08%. The stock market tone remains positive but stocks were undercut last week by (1) the increased expectation for Fed rate hikes, (2) the sharp 2-week rise in the 10-year T-note yield, (3) North Korean tensions, and (4) the modest recovery seen in the dollar index from the early-Sep 2-3/4 year low.

The focus in the stock market will soon turn towards earnings since Q3 ends this week. The market consensus for Q3 earnings is for a respectable increase of +6.2% y/y, according to Thomson I/B/E/S, down from Q2’s strong +12.3% pace. Earnings growth is then expected to improve to +12.2% in Q4 and +10.4% in Q1.

Merkel wins German election but faces a coalition-building challenge and new opposition from the right — Angela Merkel kept her job as Chancellor in Sunday’s election, but her party had a lackluster performance with about 32% of the vote, according to exit polls. That was the party’s second-worst showing since 1949. The other major establishment party, the Social Democrats, fared even worse with only 20% of the vote, its worst-ever result. The Social Democrats quickly ruled out a renewed coalition with Ms. Merkel’s CDU party, which prompted a -0.4% drop in the euro on Sunday night. That means that Ms. Merkel will now have to seek a tricky coalition with the pro-business Free Democrats and the Greens. The far-right Alternative for Germany (AfD) did surprisingly well in the election with about 13% of the vote, better than pre-election polling. The Afd now has a solid platform in the Bundestag to try to expand its political support and cause problems for Ms. Merkel.