- FOMC’s unchanged hawkish bias surprises the markets

- Unemployment claims will see first distortions from Irma

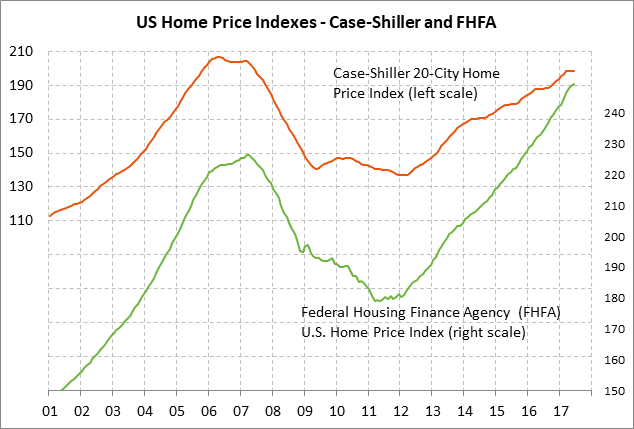

- U.S. FHFA house price index expected to show continued strength

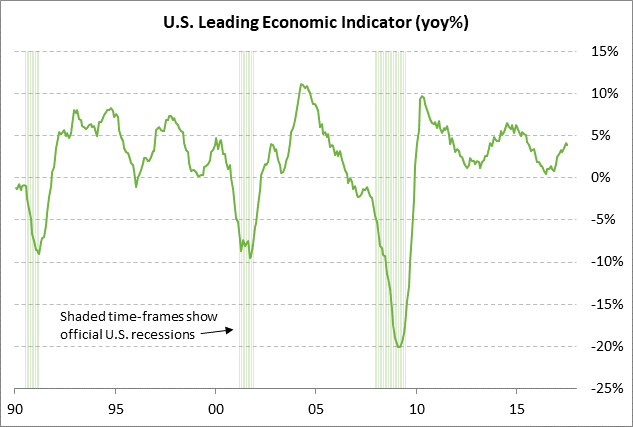

- U.S LEI expected to reach 2-1/4 year high

- 10-year TIPS auction

FOMC’s unchanged hawkish bias surprises the markets — The markets were surprised by Wednesday’s hawkish outcome of the FOMC meeting. The immediate result was a 14-tick sell-off in Dec 10-year T-note prices and a +0.9% rally in the dollar index. The FOMC results also produced a 2-5 bp tightening of the federal funds rate futures curve for the 2018 contracts and a 5-6 bp tightening for the 2018 contracts.

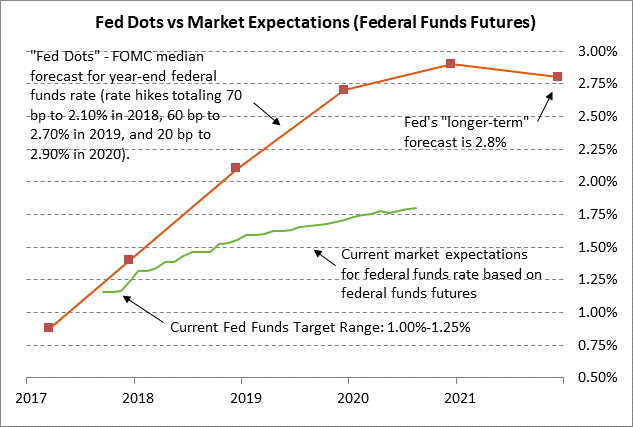

The T-note market reacted bearishly to the FOMC meeting because (1) the FOMC left intact its Fed-dot forecasts for the 2017-18 funds rate and did not cut those forecasts as the markets had hoped, (2) the Fed said the recent hurricanes are unlikely to have any medium-term implications for the national economy, and (3) the FOMC raised its 2017 GDP forecast to +2.4% from +2.2%.

The markets were left facing a Fed that seems intent on going through with its +25 bp rate hike in December and with three more rate hikes in 2018, which is a much more hawkish pace than the market expects. On the more dovish side, the Fed-dot forecast for long-term funds rate was cut to 2.75% from 3.00%, which indicated that the Fed now thinks the funds rate will eventually settle at 2.75% rather than 3.00%. The Fed’s announcement that its balance sheet reduction program will begin in October was fully in line with market expectations and had little impact.

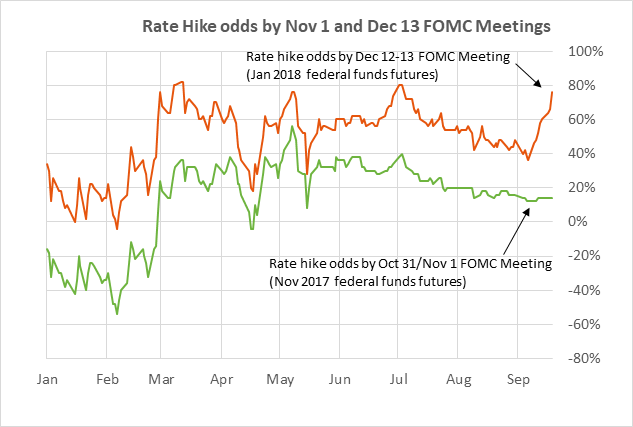

The FOMC meeting caused the market to largely give up its dovish hopes that the Fed would be forced to delay a December rate hike due to low inflation and/or hurricane damage. Indeed, the market raised the odds for a December rate hike to 76% from 66% the previous day and from a low of 36% on Sep 8. The markets are now facing a Fed that (1) is engaged in quantitative tightening by reducing its balance sheet at an accelerated rate through 2018, and (2) seems intent on raising its funds rate target four times over the next 1-1/4 years.

Now that the Fed has a near-term monetary policy plan in place, market attention will turn to who will be the next Fed Chair. Ms. Yellen’s term as Chair expires in February and President Trump will need to make an appointment within the next couple of months to leave time for the Senate confirmation process. The horse race has opened up to a much wider field after the WSJ recently reported that White House economic advisor Gary Cohn’s odds of becoming the next Fed Chair dimmed substantially after his criticism of President Trump’s Charlotte comments.

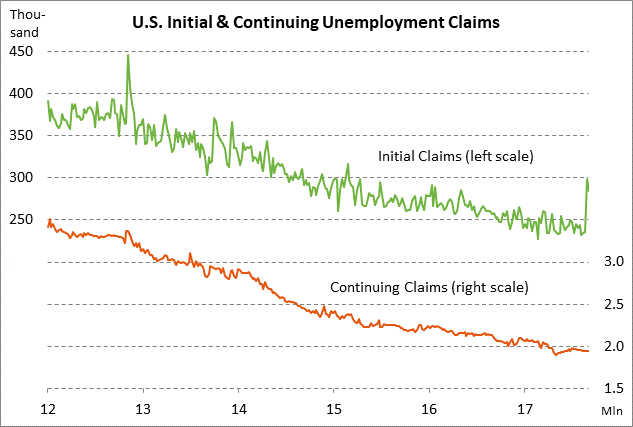

Unemployment claims will see first distortions from Irma — Today’s initial unemployment claims report for the week ended Sep 15 will see the continued effects from Hurricane Harvey, which made landfall in Texas on Aug 25. In addition, today’s initial claims report for the first time will see the effects of Hurricane Irma, which made landfall in Florida on Sep 10. The surge in initial claims from hurricane disruptions provides somewhat of a proxy for gauging the extent of business disruptions and economic fall-out from Hurricanes Harvey and Irma.

The initial claims series showed a sharp +62,000 increase in the week ended Sep 1 and then fell by -14,000 in the week ended Sep 8, leaving the series up by a net +48,000 on Hurricane Harvey. The continuing claims series has yet to see much influence from hurricane distortions and is currently only +45,000 above the 29-year low of 1.899 million posted in May. The market consensus is for today’s initial claims report to show an increase of +16,000 to 300,000 and for continuing claims to show a +31,000 increase to 1.975 million.

U.S. FHFA house price index expected to show continued strength — The market consensus is for today’s July FHFA house price index to show a solid gain of +0.4% m/m, improving from June’s small increase of +0.1%. U.S. house prices have been strong this year and were up sharply by +6.5% y/y in June. The FHFA index has now risen by a total of +39% from the housing-bust trough seen in March 2011. U.S. home prices continue to see strength from strong demand and mildly tight supplies. August’s 4.2 month supply of existing homes on the market was much tighter than the 7-8 month level that the National Association of Realtors says is consistent with stable prices.

U.S LEI expected to reach 2-1/4 year high — The market consensus is for today’s Aug leading indicators report to show a +0.3% m/m increase, thus matching July’s increase. On a year-on-year basis, today’s Aug LEI is expected to strengthen to +4.3% y/y from July’s +3.9%, which would be a new 2-1/4 year high.

The LEI has shown solid increases all this year, which bodes well for near-term GDP growth. GDP improved to a solid increase of +2.6% in Q2 from Q1’s poor pace of +1.2%. However, the Atlanta Fed’s GDPNow forecast for Q3 GDP growth sank to a low of +2.2% due to incoming economic data, which is far below the forecast of +4.0% at the beginning of the forecasting period in August.

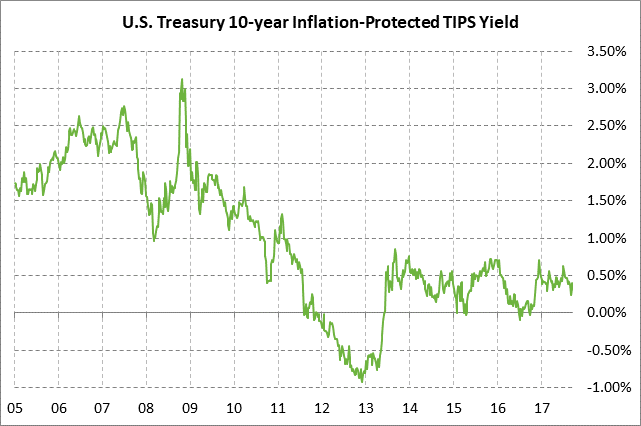

10-year TIPS auction — The Treasury today will sell $11 billion of 10-year TIPS in the first reopening of the 3/8% 10-year TIPS of July 2027, which the Treasury first sold back in July. The benchmark 10-year TIPS late Wednesday was trading at 0.36%. The 12-auction averages for the 10-year TIPS are as follows: 2.34 bid cover ratio, $22 million in non-competitive bids, 6.7 bp tail to the median yield, 15.8 bp tail to the low yield, and 58% taken at the high yield. The 10-year TIPS is the most popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buying, have taken an average of 67.6% of the last twelve 10-year TIPS auction, which is far above the average of 60.9% for all recent Treasury coupon auctions.