- U.S. consumer sentiment remains strong but will be dented by hurricanes

- U.S. retail sales remain key for U.S. GDP

- U.S. industrial production expected to show a small increase

- Sterling rallies sharply to new 1-year high after BOE’s explicit rate-hike warning

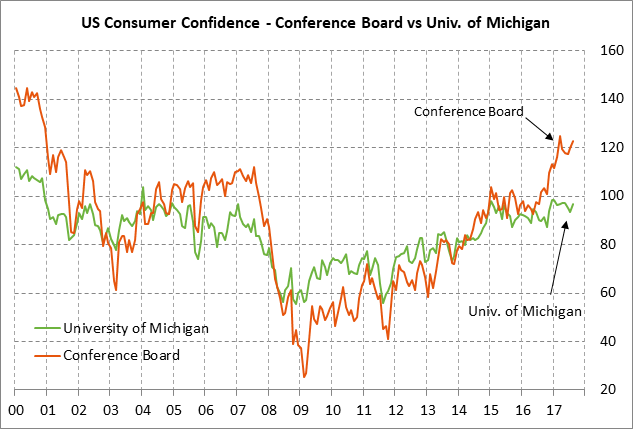

U. S. consumer sentiment remains strong but will be dented by hurricanes — U.S. consumer confidence in August was in strong shape, although down from the post-election euphoria levels. Specifically, the University of Michigan U.S. consumer sentiment index in August was only -1.7 points below the 13-1/2 year high of 98.5 posted in January. The consensus is for today’s preliminary-Sep report to show a -1.7 point decline to 95.1, reversing half of August’s +3.4 point increase to 96.8. Consumer sentiment is expected to take at least a temporary hit in September from Hurricanes Harvey (landfall on Aug 25) and Irma (landfall on Sep 10).

U.S. consumer confidence continues to see strength due to (1) the firm U.S. economy and labor market, (2) rising household wealth with the recent record high in the stock market and with rising home prices, (3) continued low interest rates and mortgage rates, (4) low gasoline prices (ex-Harvey), and (5) hopes for a personal tax rate cut.

However, U.S. consumer confidence has settled back from post-election levels mainly because of the slow Republican growth agenda and now because of hurricane damage. Other negative factors for U.S. consumer confidence include (1) geopolitical tensions with North Korea, (2) White House political uncertainty, and (3) the prospects for steadily higher interest rates over the next few years as the Fed raises its funds rate target.

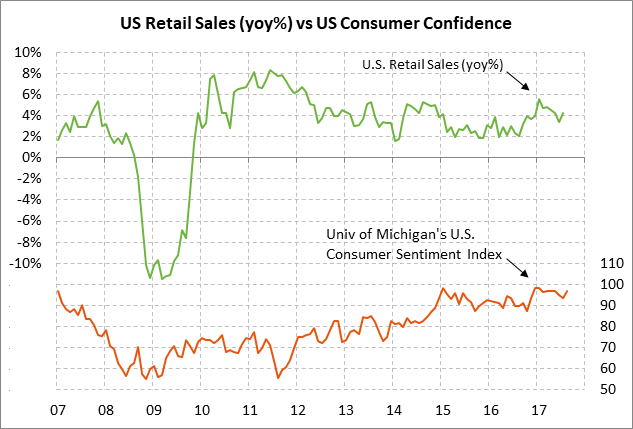

U.S. retail sales remain key for U.S. GDP — Excluding fluctuations in vehicle sales, today’s Aug retail sales report is expected to show another strong increase of +0.5%, matching July’s +0.5% increase. However, today’s headline retail sales report is expected to be weak at +0.1% (following July’s strong +0.6% increase) because of the sharp -4.0% drop in vehicle sales to a 3-1/2 year low of 16.03 million units that has already been reported for August.

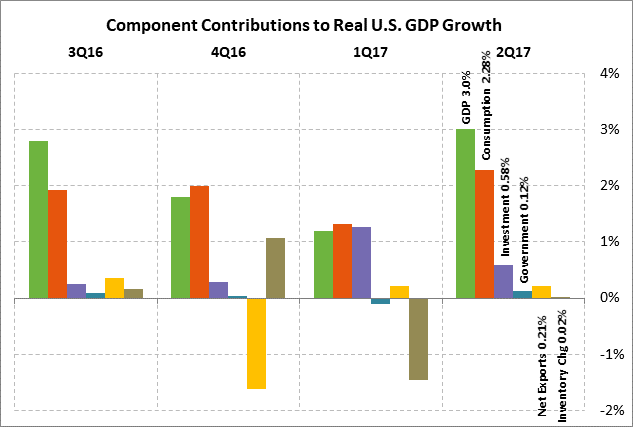

U.S. retail sales finally perked up in July after being generally weak earlier in the year. Retail sales showed a strong +1.1% increase in January but then showed an average monthly increase of only +0.1% from February through June. The good news, however, is that consumer spending on services has been strong this year and that has helped to offset the weakness in retail goods. Personal consumption contributed a paltry 1.32 points to the Q1 GDP report of +1.2%, but then perked up to contribute a strong 2.28 points to the Q2 GDP report of +3.0%.

U.S. personal spending continues to be the main driver of the U.S. economy. Business investment saw an upward spike in Q1 with a contribution of 1.27 points to GDP, but then fell back to 0.58 points in Q2. In 2016, business investment contributed an average of only +0.18 points to GDP. The economy in short remains highly dependent on consumers.

Aside from hurricane effects, U.S. consumer spending is seeing support from (1) relatively strong personal income gains stemming from rising wages and nearly full employment, (2) strong consumer confidence, and (3) rising household wealth from the strong stock market and home prices. Harvey and Irma will hurt consumer confidence, but should nevertheless boost retail sales as homeowners and businesses buy products to replace damaged goods and repair their homes and places of business.

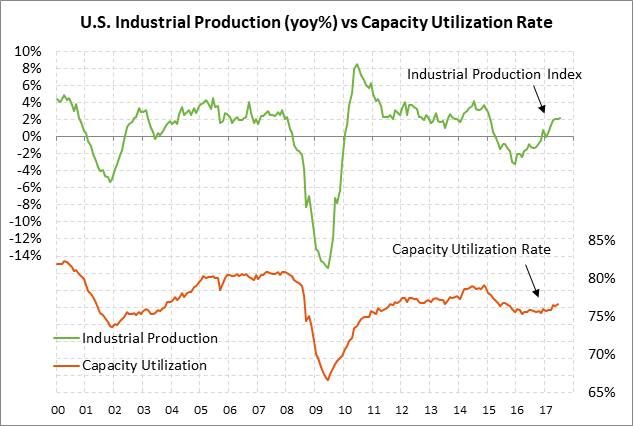

U.S. industrial production expected to show a small increase — The market consensus is for today’s Aug U.S. industrial production report to show an increase of only +0.1% following July’s weak report of +0.2%. Excluding the mining and utility sectors, the Aug manufacturing production report is expected to show a solid increase of +0.4% after July’s -0.1% decline. Hurricane Harvey made landfall on Aug 25 but will have most of its impact, along with Hurricane Irma, on the September data.

Industrial production this year has improved due to (1) fairly solid U.S. economic growth, and (2) stronger exports, which have improved due to stronger economic growth overseas and this year’s sharp decline in the dollar. Industrial production on a year-on-year basis improved to a 2-1/2 year high of +2.2% y/y in July.

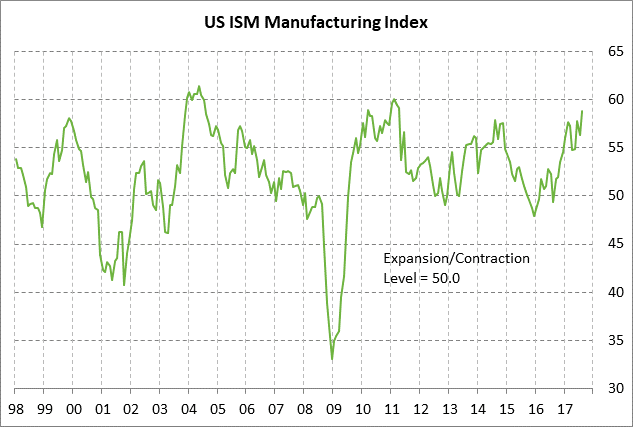

Confidence in the U.S. manufacturing sector is strong as seen by the fact that the ISM manufacturing index in August rose to a 6-1/4 year high of 58.8, the highest level since mid-2011. The ISM manufacturing new orders index in August was also strong at 60.3, illustrating a full pipeline of orders that will support manufacturing activity in coming months.

Sterling rallies sharply to new 1-year high after BOE’s explicit rate-hike warning — Sterling on Thursday rallied sharply to post a new 1-year high, closing the day up +1.88 cents (+1.42%) at $1.3399. Sterling was already on a roll due to increased expectations for a BOE rate hike after Tuesday’s news that the Aug UK CPI rose to match May’s 5-1/4 year high of +2.9% y/y and the Aug ore CPI rose to a 5-3/4 year high of +2.7% y/y. UK inflation continues to be pushed higher by Brexit-related weakness in sterling, putting pressure on the BOE to curb inflation pressures by raising the base rate from its current low level of 0.25%.

The Bank of England in Thursday’s post-meeting minutes issued an explicit rate hike warning by saying that the majority of policymakers believed that “some withdrawal of monetary stimulus was likely to be appropriate over the coming months in order to return inflation sustainably to target.” The reference to “coming months” made the November meeting live for a rate hike with the market now discounting a 50% chance for a rate hike at that meeting. The market brought forward a 100% chance of a rate hike to Feb 2018 from Feb 2019 last week.