- Weekly global market focus

- Markets wait to see if a U.S-Europe trade war begins this week

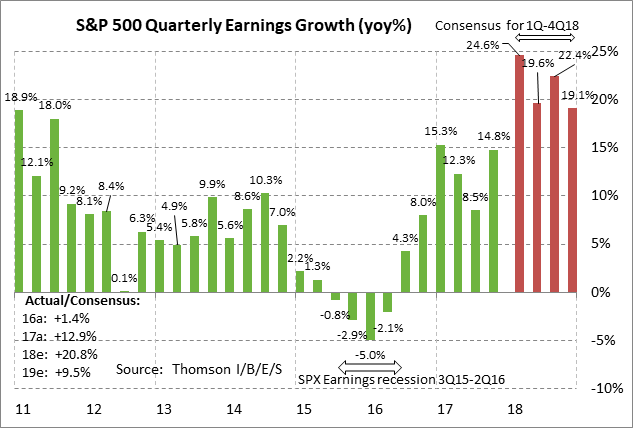

- Second heaviest earnings week expected to produce continued favorable results

- U.S. PCE deflator expected to show strength

Weekly global market focus — The U.S. markets this week will focus on (1) whether the U.S. and Europe engage in a tit-for-tat trade war as Europe’s temporary exemption from steel-aluminum tariffs expires today unless the U.S. grants an extension, (2) U.S.-Chinese trade tensions as Trump administration officials late this week travel to China to see if a negotiated solution can be reached, (3) the Tue-Wed FOMC meeting, which is expected to produce an unchanged policy, (4) Friday’s U.S. unemployment report, which is expected to show a solid U.S. labor market with a +195,000 gain in payrolls and a -0.1 point drop in the unemployment rate to a new 17-year low of 4.0%, (5) this week’s heavy dose of Q1 earnings with 147 of the S&P 500 companies scheduled to report, and (6) oil prices, which continue to see support from the very real chance that President Trump will abrogate the Iran nuclear agreement by his self-imposed deadline of May 12.

The European markets this week will key on U.S.-European trade tensions and economic data. Wednesday’s Eurozone Q1 GDP report is expected to ease to +2.0% (q/q annualized) from Q4’s +2.8% due in part to bad weather. Thursday’s April Eurozone CPI report is expected to ease to +1.3% y/y from March’s +1.6% and the core CPI is expected to edge lower to +0.9% y/y from March’s +1.0%. In Italy, the Democratic Party late this week is expected to decide whether to enter coalition talks with Five Star. The European markets are closed on Tuesday for May Day.

The Asian markets this week will focus on the U.S.-Chinese trade negotiations later this week. Chinese PMI data will be released on Tuesday and Thursday nights (ET). The Chinese markets will be closed for the May Day holiday on Monday and Tuesday. The Japanese markets will be closed for Golden Week holidays on Monday, Thursday and Friday.

Markets wait to see if a U.S-Europe trade war begins this week — US Commerce Secretary Wilbur Ross on Saturday said that the Trump administration plans to extend the temporary exemptions on steel-aluminum tariffs for certain countries that would otherwise expire today. Mr. Ross said the announcement about which countries will receive extensions will be made just before the exemptions expire at midnight Monday night.

If the Trump administration today does not extend the EU’s exemption and the steel-aluminum tariffs go into effect on Tuesday, then there is little doubt that the EU this week will go through with its threat to slap a retaliatory 25% tariff on a broad range of $3.5 billion worth of U.S. exports to Europe. Europe’s list of U.S. products that will be subject to the 25% retaliatory tariff includes (1) about 1 billion euros worth of U.S. consumer products such as clothes, cosmetics, motorcycles, and boats, (2) about 950 million euros worth of agricultural products such as orange juice, corn, bourbon whiskey and other ag products, and (3) about 850 million euros of industrial products including steel products.

The question then will be whether President Trump responds with a new round of tariffs on Europe for their retaliation, indicating a spiraling of trade tensions. When China announced its tariff retaliation on $50 billion of U.S. goods, Mr. Trump responded by saying he would slap tariffs on an additional $100 billion of Chinese goods.

Other countries that are waiting to see if they get an extension of the steel-aluminum tariffs include Australia, Brazil, and Argentina. South Korea has already received a permanent exemption tied to its agreement to a revised bilateral trade deal. An exemption for Mexico and Canada is tied with the NAFTA talks. Australia believes it has already received a permanent exemption.

Second heaviest earnings week expected to produce continued favorable results — This will be the second largest week for Q1 earnings (after last week’s peak) with 147 of the S&P 500 companies scheduled to report. Of the 267 SPX companies that have reported, 79.4% have announced above-consensus earnings, which is above both the long-term average of 64% and the 4-quarter average of 75%, according to Thomson I/B/E/S. Of reporting companies, 74.1% have announced above-consensus revenue, which is above both the long-term average of 60% and the 4-quarter average of 69%.

The market consensus is for Q1 SPX earnings growth of +24.6% (+2.7% ex-energy), which is better than expectations of +18.5% at the beginning of earnings season. The market is expecting strong earnings growth to continue with SPX earnings growth of +19.6% in Q2, +22.4% in Q3, and +19.1% in Q4, according to Thomson I/B/E/S. On a calendar year basis, the consensus is for earnings growth of 20.8% in 2018 and +9.5% in 2019.

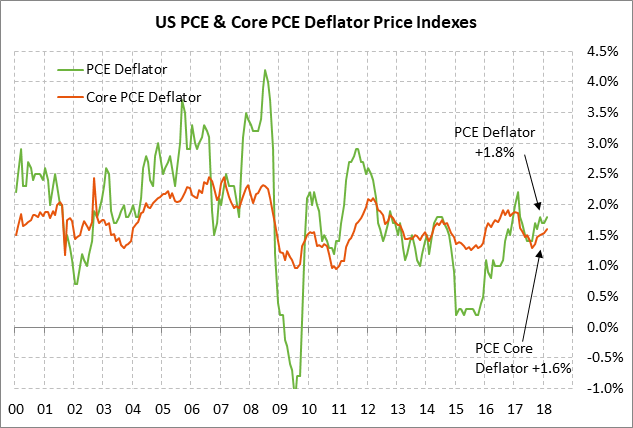

U.S. PCE deflator expected to show strength — Today’s PCE deflator is expected to show jumps in the year-on-year growth rates but that will mainly be due to a base effect from the year-ago drop in cell phone costs falling out of the year-on-year calculation. The consensus is for today’s Mar PCE deflator to jump to +2.1% y/y from Feb’s +1.8% and for the March core PCE deflator to jump to +1.9% y/y from Feb’s +1.6%.

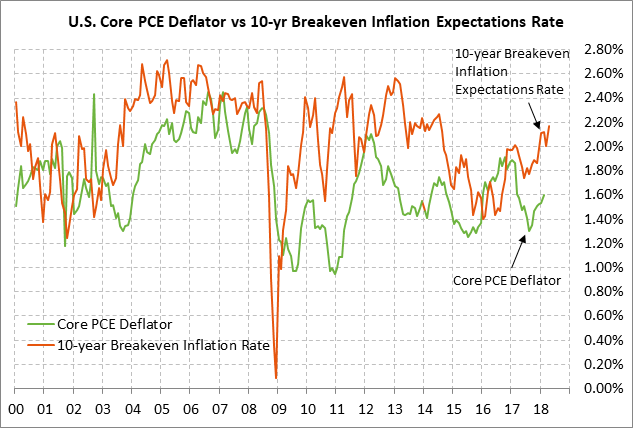

Even though the year-on-year figures are expected to jump to levels closer to the Fed’s +2.0% inflation target, the month-on-month increases are expected to be more subdued at unchanged for the headline figure and at +0.2% for the core figure. In any case, market-based expectations for inflation have risen substantially in recent months. The 10-year breakeven inflation expectations rate is currently at 2.17%, which is only 3 bp below last week’s 3-3/4 year high of 2.20% and is above the Fed’s +2.0% inflation target.