- Weekly global market focus

- Tariff threats will continue to dominate the markets

- Stock and bond markets see volatility on Trump tariff news and weak payroll report

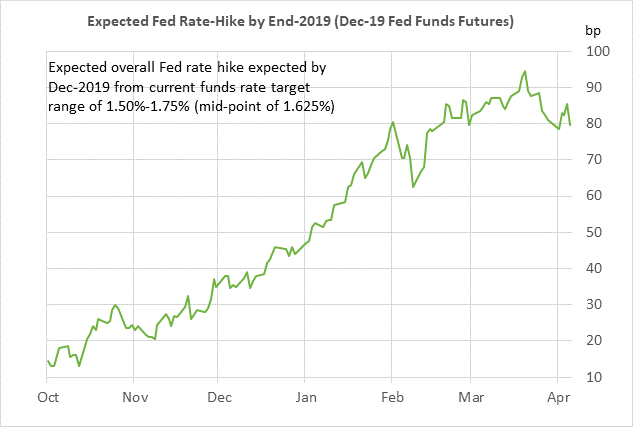

Weekly global market focus — The U.S. markets this week will focus on (1) whether the Trump administration launches any new tariff threats against China and whether China announces any further retaliatory measures, (2) concern about tech sector regulation as Facebook CEO Zuckerberg will testify before Congressional committees on Tuesday and Wednesday, (3) the beginning of Q1 earnings season with 7 of the S&P 500 companies scheduled to report earnings this week, (4) Wednesday’s release of the March 20-21 FOMC meeting minutes and further analysis of whether the trade turmoil may soften the Fed’s rate-hike regime, (5) any tightening of the U.S. inflation outlook with Wednesday’s March CPI expected to rise to +2.4% y/y from Feb’s +2.2% (March core CPI expected +2.1% y/y from +1.8%), (6) the Treasury’s sale this week of $64 billion of 3-year, 10-year and 30-year securities, and (7) oil prices as John Bolton, vitriolic critic of the Iran nuclear agreement, is scheduled to become President Trump’s new security advisor effective today, replacing H.R. McMaster.

In Asia, the focus will be on Chinese President Xi Jinping’s speech on Tuesday at the annual Boao Forum for Asia (sometimes called Asia’s Davos) and whether he addresses the U.S.-Chinese tariff dispute. Chinese economic news this week includes loan, CPI, and trade data. The Chinese mainland stock market today will reopen after having been closed for a holiday last Thursday-Friday during some of the worst trade tariff news. However, the Hong Kong Hang Seng last Friday was able to close +1.11% higher after Thursday’s Hong Kong holiday.

In Europe, the focus will be on economic data with key reports including Monday’s German Feb trade report (Feb exports expected +0.4% m/m) and Thursday’s Feb Eurozone industrial production report (expected +0.1% m/m after Jan’s -1.0%). The markets will also be watching another round of talks this week in Italy about the nearly intractable process of forming a new government.

Tariff threats will continue to dominate the markets — The markets this week will remain on edge about trade threats as they wait to see how U.S. Trade Representative Lighthizer responds to President Trump’s call late last Thursday to consider tariffs on another $100 billion of Chinese imports as punishment for China’s announcement last Wednesday of tariff retaliation on $50 billion of U.S. goods. China on Friday responded to President Trump’s new tariff threat with a promise to “follow suit to the end and at any cost, and will firmly attack using countermeasures.” The Trump administration’s list of $50 billion worth of Chinese imports subject to 25% tariffs, which was released last Tuesday, is currently on hold since it is in the 60-day public comment period.

The stock market fell sharply on Wednesday and again Friday on trade tariff news. Trump administration officials tried to soothe the markets by saying that there will be negotiations and noting that the tariffs will not go into effect at least until after the 60-day comment period.

However, neither the U.S. or China seem particularly interested in talks at present. White House Economic Advisor Larry Kudlow last Friday said serious talks with China “have not really begun” and that the U.S. has not even given China a detailed list of demands about how they could avoid the tariffs on $50 billion of goods. The White House’s new theme is that there will be some short-term pain in the expectation of gaining some longer-term advantage. Treasury Secretary Mnuchin last Friday admitted there is “a level of risk” that the dispute could spiral into a full trade war.

The markets are also nervous about the fate of NAFTA. President Trump last week said that he wanted to get a NAFTA agreement in principle done quickly so he could announce it this week in Peru when he attends the Summit of the Americas on Friday. That lit a fire under the NAFTA talks last week but even an agreement in principle by this week seems unlikely given the number of product and service sectors that still need to be agreed upon.

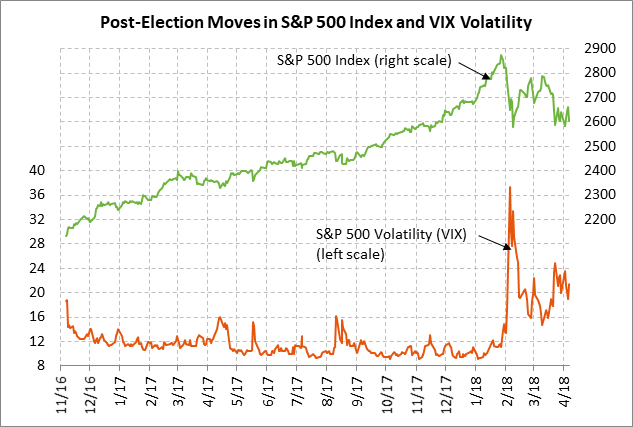

Stock and bond markets see volatility on Trump tariff news and weak payroll report — The S&P 500 index last Friday fell sharply by -2.19% after President Trump late Thursday threatened to slap tariffs on another $100 billion of Chinese imports, upping the ante after China responded with equal-sized tariffs to President Trump’s 25% tariff on Chinese products. China doesn’t even have $150 billion of U.S. imports for applying tariffs but China can retaliate in other ways such as by clamping down on U.S. companies producing and selling in China and potentially even curbing its holdings of U.S. Treasury securities.

The markets have been trying to stay positive through the tariff news, trying to convince themselves that a negotiated agreement will head off the tariffs. However, it is worth noting that the U.S. tariffs on steel-aluminum and China’s tariff retaliation on $3 billion worth of U.S. products have already gone into effect. China has not yet announced specific retaliation for earlier U.S. tariffs on Chinese solar and washing machines. Moreover, neither the U.S. or China seem eager to show any interest in serious negotiations. We suspect that The Trump administration may end up issuing even more threats before China gets worried enough to hold serious talks.

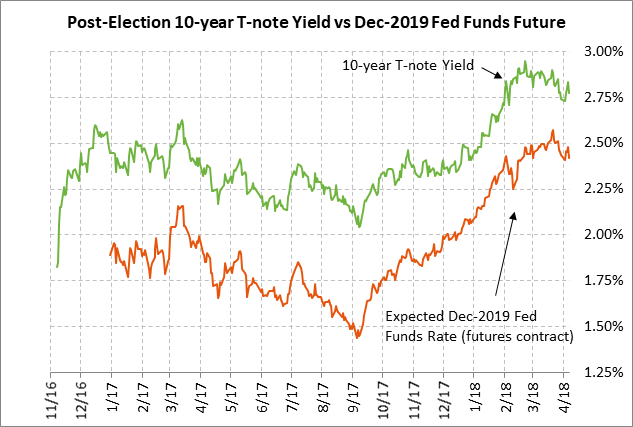

The T-note market last Friday found support from the trade turmoil and the weak March payroll report of +103,000 (vs expectations of +185,000). The weak payroll report was largely due to weather factors and some payback after Feb’s sharp gain of +326,000, but the report nevertheless constituted a piece of weak U.S. economic data. The T-note market was a little disappointed after Fed Chair Powell on Friday said it is too early to worry about trade tariffs, which suggested that the Fed is not yet going to pull its rate-hike punches due to the trade turmoil.