- Weekly U.S market focus

- Weekly European market focus

- Weekly Asian market focus

- U.S. stocks remain near the top of the recovery rally

Weekly U.S market focus — The U.S. markets this week will focus on (1) any market-moving news out of the 2-day G20 meeting of finance ministers and central bankers that begins today in Buenos Aries, (2) the FOMC meeting on Tue/Wed where the markets will mainly focus on the extent to which the Fed dots are raised since a +25 rate hike is already considered by the markets to be a 100% done deal, (3) whether Congress this week approves an omnibus spending bill to avert a government shutdown this Friday when the current continuing resolution expires, (4) the recent downgrade in expectations for Q1 U.S. GDP growth due to weak consumer spending, although last Friday’s U.S. economic reports were stronger than expected, (5) White House political uncertainty as President Trump over the weekend railed against the Mueller investigation and could announce more staff changes this week, (6) the Treasury’s sale on Thursday of $11 billion of 10-year TIPS, and (7) a light earnings week with 10 of the S&P 500 companies scheduled to report (including Oracle, FedEx, and Nike).

The markets are waiting to see if President Trump this week will exempt Europe from his steel and aluminum tariffs that take effect this Friday at midnight. If Europe is not exempted, Europe has prepared a retaliatory tariff package involving some $3.5 billion worth of U.S products. The Trump administration today is expected to officially release the guidelines by which U.S. companies can apply for an exemption from the tariffs on imported steel and aluminum.

On the trade front, the markets will also be watching for any news on impending Chinese retaliation for the U.S. steel and aluminum tariffs. The markets will also be watching for any news on the Trump administration’s preparation of a large retaliation package for Chinese IP violations. Politico reported last Tuesday that President Trump told U.S. Trade Advisor Lighthizer to raise the $30 billion proposed size of the retaliation package. Politico said the IP retaliation package could be announced as soon as this week but that the deadline might slip.

Weekly European market focus — In Europe, the focus will be on the Bank of England meeting on Thursday, which is expected to produce an unchanged policy rate but is also expected to lay the ground work for a rate hike in the next few months. The markets are discounting an 80% chance of a rate hike by May. Brexit will be a major focus this week as the UK tries to get the EU to sign off on a transition deal at the 2-day EU summit starting on Thursday, which would be a big step forward on Brexit for the UK.

The markets will be watching to see Vladimir Putin’s margin of victory for his fourth 6-year term as Russian president in Sunday’s election. Early returns pointed to a large Putin vote of around 73%, which would be higher than 64% in his last election in 2012 and turnout of about 60%, a little higher than the 2012 level.

Italy’s parliament will convene this Friday after the March 4 elections. Italy’s parties are trying to hash out whether it will be possible to form a governing coalition. The markets continue to watch with some concern about the influence of the populist League and Five Star parties.

Weekly Asian market focus — In Asia, the focus will be on China where the National People’s Congress (NPC) today is expected to confirm a new central bank chief. The Wall Street Journal on Sunday reported that current deputy PBOC governor Yi Gang will be named as the new central bank chief. If true, the markets would be pleased with that choice since Yi Gang already has long experience in helping to run the central bank and he is likely to continue the PBOC’s current policy direction.

The NPC on Sunday confirmed Xi Jinping’s second 5-year term as President on Sunday by a vote of 2,970 to 0. The 2-week NPC meeting wraps on Tuesday with a speech from President Xi Jinping and an annual press conference by Premier Li Keqiang. The Chinese government discouraged stock selling during the 2-week NPC meeting, which means the markets will be watching for any pent-up selling later this week after the NPC meeting ends.

In Japan, the markets will continue to assess the vulnerability of Prime Minister Abe as the scandal worsens over the news that the Ministry of Finance doctored documents related to the land purchase for a school that Mr. Abe and his wife promoted. Japanese Finance Minister Taro Aso will not attend this week’s G20 meeting amidst calls for his resignation over the matter. Japan will instead be represented at the G20 meeting by Vice Finance Minister Minoru Kihara.

The good news for the markets is that the Japanese parliament last Friday confirmed BOJ Governor Kuroda for another 5-year term, thus ensuring that the BOJ’s QE program and zero interest rate policy will continue regardless of how the Abe political scandal unfolds. BOJ Governor Kuroda will be attending this week’s G20 meeting as usual.

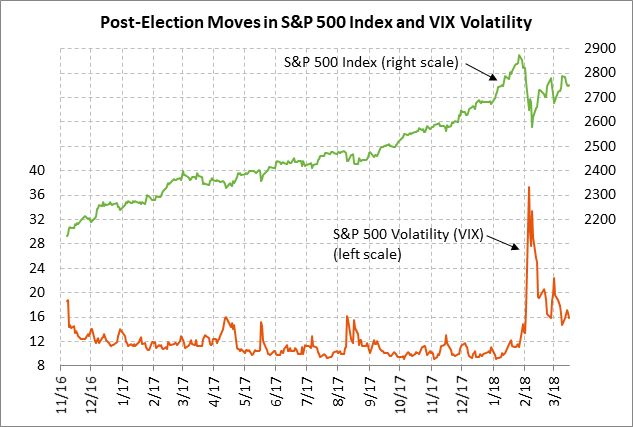

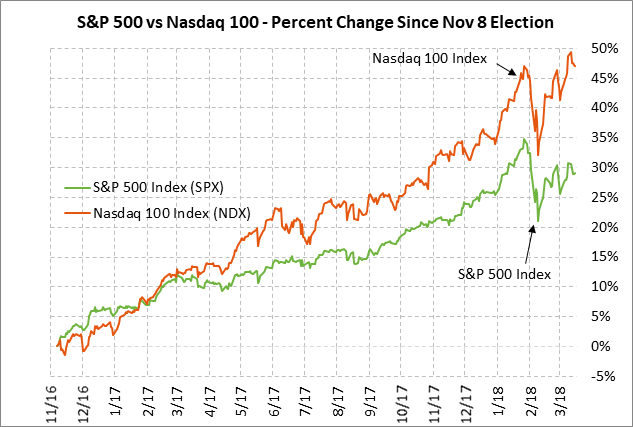

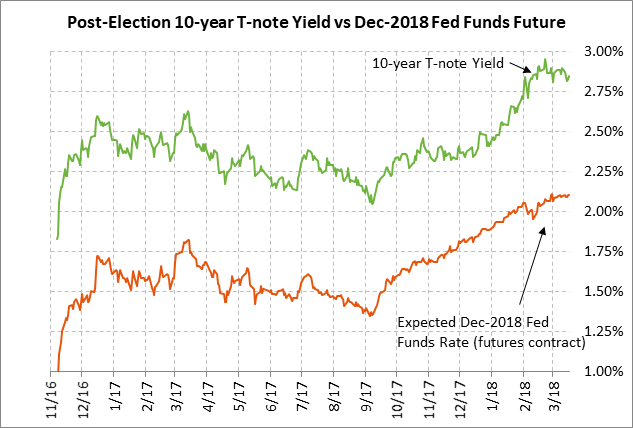

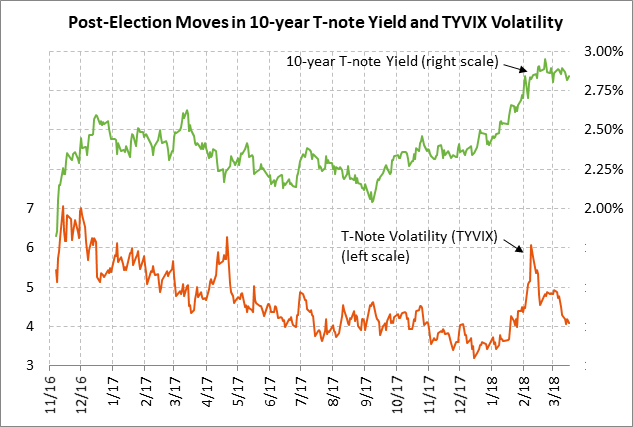

U.S. stocks remain near the top of the recovery rally — The S&P 500 index remains near the top of its Feb-March recovery rally, while the Nasdaq 100 index is in even stronger shape after posting a new record high last Tuesday. The U.S. stock market continues to be underpinned by expectations for a continued strong economy through year-end and by strong earnings growth. There is also some relief as the 10-year T-note yield has been subdued in the past several weeks as it traded sideways below the late-Feb 4-year high of 2.95%.

The stock market has so far been able to largely shake off concerns about a possible trade war and White House political uncertainty. The stock market this week will have to absorb a Fed rate hike on Wednesday and a likely hike in the Fed-dot forecasts for the funds rate over the next two years.