- U.S. CPI expected to keep upward pressure on Treasury yields

- Treasury sees adequate demand for 3 and 10-year auctions and sells 30-year bonds today

- Democrats’ unwillingness to join a coalition will drag out Italian government talks

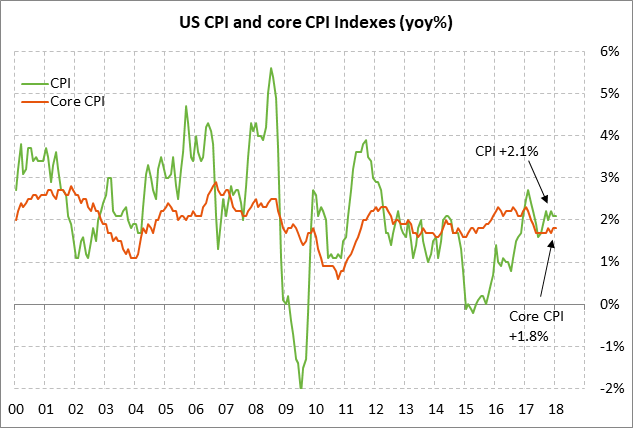

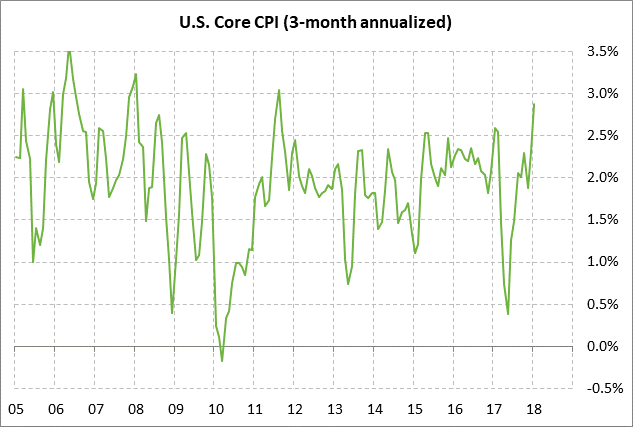

U.S. CPI expected to keep upward pressure on Treasury yields — The market consensus is for today’s Feb CPI report to ease to +0.2% m/m from Jan’s strong report of +0.5%, but base effects are expected to push the year-on-year figure up to match the 10-month high of +2.2% from Jan’s +2.1%. The expected report would produce 3-month annualized CPI growth of +3.8%, down from Jan’s 5-1/4 year high of +4.4% but still a high growth rate.

The consensus is for the Feb core CPI to also show a +0.2% m/m increase, down slightly from Jan’s +0.3% m/m. The consensus is for the Feb core CPI on a year-on-year basis to be unchanged from Jan at +1.8% y/y. The expected report would produce a 3-month annualized core CPI gain of +3.2%, which would be higher than Jan’s +2.9% and would be a new 3-1/2 year high.

Today’s CPI report is expected to be favorable in that inflation is expected to ease slightly on a month-on-month basis. However, the 3-month annualized figures are expected to remain strong and keep the pressure on the Fed to continue the current pace of its tightening program. The good news is that the Fed’s preferred inflation measure, the PCE deflator, remains tamer at +1.7% y/y headline and +1.5% y/y, both below the Fed’s +2.0% inflation target.

Today’s CPI report will not affect the market’s view that there is a 100% chance of an FOMC rate hike next week. However, a stronger-than-expected CPI report today would certainly push expectations higher for the Fed’s overall rate hike over the next two years. The current consensus is for an overall 72.5 bp rate hike in 2018 (2.9 rate hikes), slightly below the record high of 73.5 bp posted two weeks ago. The consensus is then for another 39.5 bp worth of rate hikes in 2019 (1.6 rate hikes), slightly below the record high of 40 bp posted last Friday.

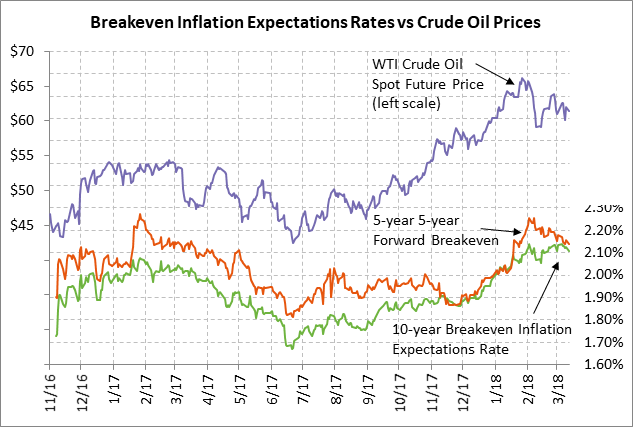

Meanwhile, market-based expectations for inflation have backed off slightly in the past several sessions, helped by last Friday’s news that Feb wage growth eased to +2.6% y/y from +2.8% in January. The 10-year breakeven inflation expectations rate on Monday eased to a 1-week low of 2.11%, which is 3.6 bp below the 3-1/2 year high of 2.146% posted in late-Feb.

The 10-year breakeven rate has also been held down in recent weeks by the fact that oil prices have backed off from their 3-1/4 year high posted in January. April crude oil is currently trading at $61.31, which is -8.0% below the 3-1/4 year nearest-futures high of $66.66 posted in late January.

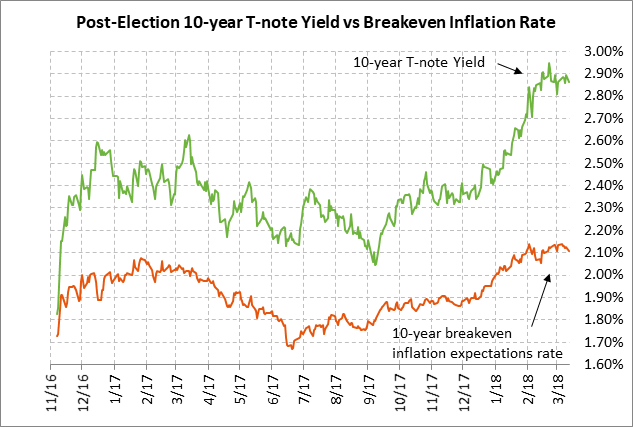

The fact that the breakeven rate has eased a bit in the past few sessions has taken some of the upward pressure off Treasury yields. The 10-year T-note yield on Monday closed mildly lower by -2.6 bp at at 2.868%, which is down by -8.6 bp from the 4-1/4 year high of 2.954% posted Feb 21.

Treasury sees adequate demand for 3 and 10-year auctions and sells 30-year bonds today — The Treasury today will sell $13 billion of 30-year T-bonds, completing this week’s $62 billion coupon package. Today’s 30-year bond will be the first reopening of the 3.00% bond of Feb 2048, which the Treasury first sold last month. Today’s 30-year bond was trading at 3.13% in when-issued trading late yesterday afternoon, which translates to an inflation-adjusted yield of 1.01% against the current 30-year breakeven inflation expectations rate of 2.12%.

The 30-year bond is a little below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.9% of the last twelve 30-year bond auctions, which is mildly below the average of 63.4% for all recent Treasury coupon auctions.

Treasury yields are currently high enough for the Treasury to get its securities sold, even in the larger amounts that have become necessary due to the U.S. government’s rising budget deficit. Monday’s sale of 3-year and 10-year T-notes drew decent demand. The 3-year T-note had a bid-cover ratio of 2.94 (slightly above the 12-auction average of 2.91) and the 10-year had a bid-cover ratio of 2.50 (mildly above the 12-auction average of 2.44). Meanwhile, foreign demand for Monday’s auctions was mixed. Indirect bidders took only 50.0% of the 3-year T-note auction, which was well below the 12-auction average of 54.4%. However, indirect bidders took 66.2% of the 10-year auction, which was well above the 12-auction average of 64.1%.

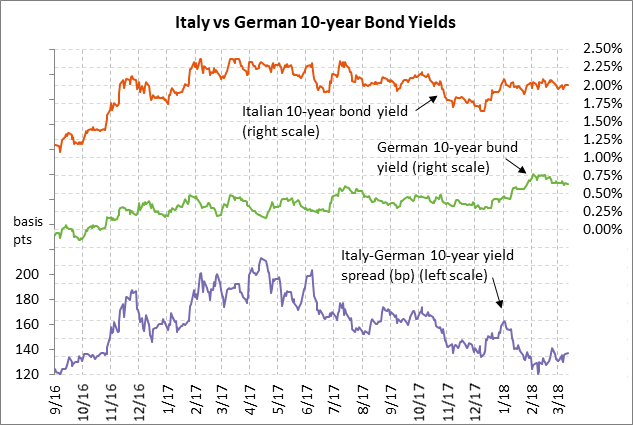

Democrats’ unwillingness to join a coalition will drag out Italian government talks — Italy’s Democratic Party met on Monday to try to chart a way forward. The party accepted the resignation of former Italian Premier Matteo Renzi and chose outgoing agriculture minister Maurizio Martina as their interim party leader. Mr. Marina proceeded to reiterate Mr. Renzi’s line that the Democrats will not enter a coalition with populist parties and therefore will also not agree to a coalition with either the Five Star Movement or with the center-right coalition (due to the two right-wing parties in that coalition).

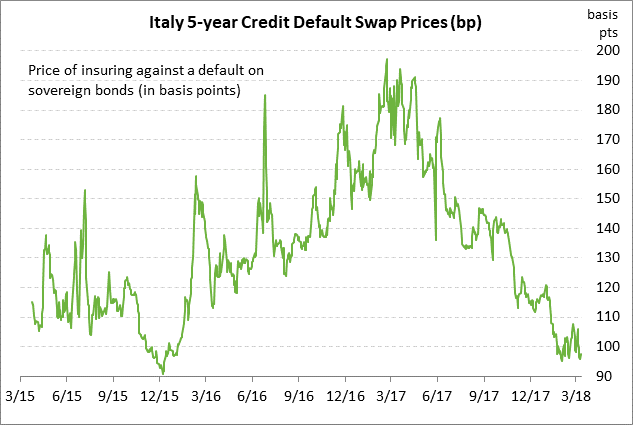

With the Democrats currently refusing to join a coalition, there is no obvious way for either Five Star or the center-right coalition to form a government. The parties will need to keep working on some type of compromise government, or Italian voters will have to go back to the polls. Monday’s news underscored that it is going to be a matter of weeks or months before Italy gets a stable government. The good news, however, is that the markets are displaying a remarkable degree of patience. The Italian 10-year bond yield spread over German bunds is currently at 137 bp, which is well below the levels of 180-200 seen last spring when the markets were afraid that the National Front could win the French elections.