- Weekly global market focus

- Trump calls off Mexican tariffs

- Trade focus returns to China

- Fed policy expectations turn even more dovish

- JOLTS report expected to extend March’s surge

Weekly global market focus — The U.S. markets this week will focus on (1) relief that President Trump late Friday called off the tariffs on Mexican imports that were scheduled to begin today, (2) the 3-week run-up to an expected Trump-Xi meeting in late June and whether the two presidents can get trade talks back on track with a deferral of a new 25% tariff on $300 billion on Chinese goods, (3) Fed policy ahead of next week’s FOMC meeting after last Friday’s weak May payroll report of +75,000 provided the Fed with hard evidence of some economic weakness, (4) oil prices, which remain on the defensive above last week’s 5-month low that was posted on trade war concerns and doubts about the OPEC+ commitment to stick to production cuts into 2H2019, (5) this week’s U.S. economic data that includes CPI and retail sales reports, (6) the Treasury’s sale of 3-year, 10-year and 30-year securities, and (7) M&A news with Sunday’s announcement that United Technologies will buy Raytheon in a $50+ billion all-stock deal.

In Europe, the focus will be on the EU’s budget row with Italy as EU finance ministers at their meeting on Thursday will discuss whether Italy should eventually be fined for non-compliance with EU fiscal rules. Key economic events this week include (1) comments by ECB President Draghi on Wednesday at an ECB conference, (2) Tuesday’s Eurozone June Sentix investor confidence index (expected -3.3 to 2.0 after May’s +5.6 to 5.3), and (3) Thursday’s Eurozone April industrial production report (expected -0.4% m/m after March’s -0.3%).

In the UK, Conservative Party MPs on Thursday will hold their first vote to whittle down the large number of candidates running to become the new Conservative Party leader and Prime Minister. Boris Johnson is the odds-on favorite to become the next Prime Minister with a betting probability of 74%, far ahead of second-place Jeremy Hunt at 8%, according to PredictIt.org. A series of additional votes will be taken next week to choose two candidates to be presented to the full Conservative Party membership across the country. A new Prime Minister is expected to be appointed in the week of July 22. The markets remain nervous about Boris Johnson’s expressed willingness for a no-deal Brexit if Europe will not revise the withdrawal agreement to his liking.

In Asia, the markets are focused on Chinese stocks and the yuan ahead of the expected Trump-Xi meeting at the end of June. There is a series of Chinese economic data this week including the CPI and PPI on Tuesday night, and the May industrial production and retail sales reports on Thursday night.

Trump calls off Mexican tariffs — In some very good news for the markets, President Trump late Friday said that his threatened tariff on all Mexican imports would be “indefinitely suspended” since the U.S. and Mexico reached an agreement on migration. The Mexican peso rallied +1.8% in early trading on Sunday in response to the news.

However, the markets are still somewhat nervous that the threat of a tariff on Mexican imports could return sometime down the road since Mr. Trump said the tariff was only “suspended” and not completely canceled. In addition, there was some uncertainty about Mr. Trump’s apparent reference to some side agreement whereby he said Mexico agreed to buy large amounts of U.S. farm products, which Mexican officials over the weekend said didn’t exist. In addition, Mr. Trump on Sunday tweeted that if there isn’t the “great cooperation” between the U.S. and Mexico that he expects, then “we can always go back to our previous, very profitable, position of Tariffs – But I don’t believe that will be necessary.”

Trade focus returns to China — Now that the Mexican tariff threat has passed, market attention is focused back on US/Chinese trade relations. There was no significant news out of Treasury Secretary Mnuchin’s meeting with PBOC Governor Yi Gang on Sunday. Mr. Mnuchin simply tweeted that they had a “candid” and “constructive” talk on trade issues. Earlier, Mr. Mnuchin on Saturday said, “If they want to come back to the table and have a real agreement, we will negotiate. If not, we’ll go forward with our plan” to impose more tariffs.

President Trump last week said that he will wait until he meets with President Xi at the G-20 meeting on June 28-29 before deciding on whether to proceed with his threat to slap a 25% tariff on another $300 billion of Chinese goods. The markets are hoping that Presidents Trump and Xi at their late-June meeting can get the trade talks restarted and that Mr. Trump will defer his tariff threat.

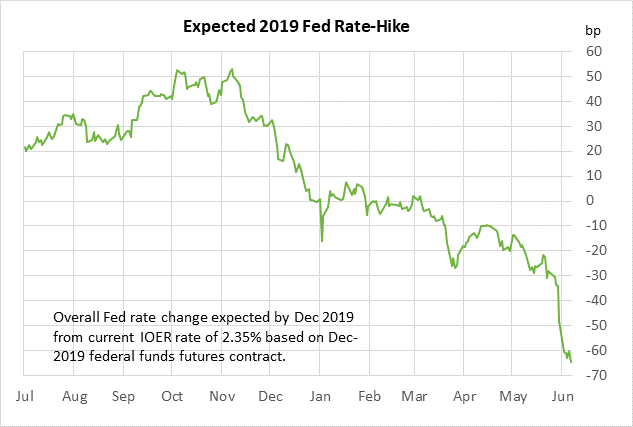

Fed policy expectations turn even more dovish — Market expectations for Fed rate cuts reached a new high last Friday with the market now expecting 64.5 bp of easing (i.e., 2.6 rate cuts) through the end of this year and a further 25.5 bp of easing in 2020 (i.e., one rate cut). Last Friday’s weak payroll report of +75,000 (vs expectations of +180,000) provided evidence to suggest that business confidence and hiring have finally taken a decisive hit from the U.S. trade war and from worries about higher costs and disrupted supply chains. The market is discounting a 25% chance of a rate cut at the FOMC’s meeting next week (June 18-19) and an 83% chance of a rate cut at the July 30-31 FOMC meeting.

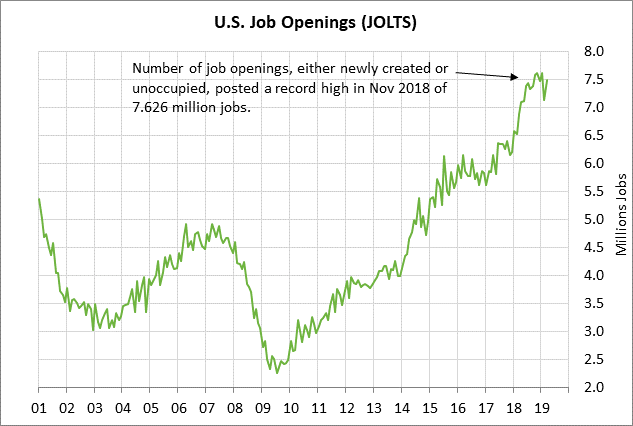

JOLTS report expected to extend March’s surge — The consensus is for today’s April JOLTS job openings report to show a small increase of +8,000 to 7.496 million, adding to March’s big +346,000 increase to 7.488 million, which would be just moderately below November’s record high of 7.626 million. A firm JOLTS report today would take some of the sting out of last Friday’s weak May payroll report of +75,000 since it would suggest that the hiring pipeline is still relatively strong and that May’s weak payroll report represented just a temporary hiring dip.