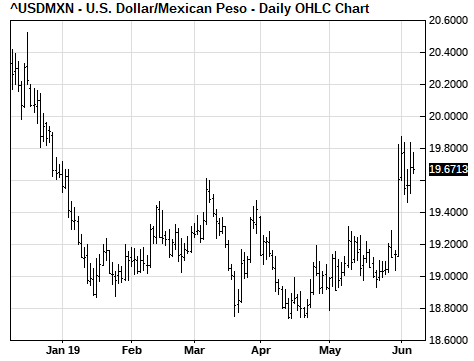

- Delay possible for Monday’s tariff on Mexico

- Markets wait to see if Mnuchin can nail down a Trump/XI meeting

- ECB takes dovish turn as Draghi says ECB is “determined to act” if situation deteriorates

- Markets on edge about today’s payroll report after weak ADP report

Delay possible for Monday’s tariff on Mexico — The U.S. stock market on Thursday was buoyed by a report that the Trump administration may be willing to delay Monday’s tariff on Mexican imports to allow more time to negotiate a migration agreement. Trump administration officials are reviewing an offer from the Mexican government on measures to curb migration. Yet there was no agreement in mid-level talks on Thursday. Vice President Pence late Thursday said that talks will continue on Friday but that the administration currently still plans to impose the tariff on Monday.

The situation may be on hold until President Trump returns today from his European trip and has a chance to review Mexico’s offer. The markets may be notified as to the status of Monday’s tariff by a tweet by President Trump either today or over the weekend.

The Trump administration has already drafted a new emergency declaration as a justification for the tariffs. Congress could block the emergency declaration and the tariffs but that would require a veto-proof two-thirds vote in both houses and that looks particularly doubtful in the House. Moreover, there isn’t enough time for Congress to vote before the tariff could go into effect on Monday.

Markets wait to see if Mnuchin can nail down a Trump/XI meeting — Treasury Secretary Mnuchin this weekend will hold a bilateral meeting with PBOC Governor Yi Gang when they are both in Japan for the G20 meeting of finance ministers and central bankers. Mr. Mnuchin will also have some contact with China’s finance minister since they are appearing together on a panel.

The markets are hoping that Mr. Mnuchin can get China to agree to a definitive meeting between Presidents Trump and Xi at the upcoming G20 summit on June 28-29 in Osaka, Japan. China seems to be slow-walking the scheduling of that meeting as a means to register its disapproval of President Trump’s handling of the US/Chinese trade relationship.

In some good news, President Trump on Thursday said that he will wait to decide on whether to impose the 25% tariff on another $300 billion of Chinese goods until after the G-20 summit when he will presumably meet with President Xi. Previously, Mr. Trump’s tariff decision point could have been as soon as mid-June since Mr. Trump in mid-May said China had only a month to make a deal. Mr. Trump’s new timeline means there is probably a decent chance that Presidents Trump and Xi at the G-20 meeting could get the trade talks back on track, assuming Mr. Trump agrees to hold off on the new round of tariffs.

On the other hand, if Mr. Trump goes ahead with the 25% tariff on another $300 billion of Chinese goods, then the U.S. at that point would have shot off nearly all its ammunition. The U.S. and Chinese economies would then be in full disengagement mode. China might then decide that it can’t do business with President Trump and decide to simply wait for the end of the Trump presidency. That would obviously be a worst-case scenario for the markets since there would be an all-out US/Chinese trade war at least until the end of President Trump’s first term in Jan 2021.

ECB takes dovish turn as Draghi says ECB is “determined to act” if situation deteriorates — ECB President Draghi at his press conference after Thursday’s ECB meeting made a forceful comment that the ECB “is determined to act in case of adverse contingencies.” He therefore essentially promised more ECB action if the Eurozone economy sinks due to global trade tensions or if inflation craters. Indeed, the ECB did take some action on Thursday by extending the promise for interest rates to stay at their present level at least until June 2020, six months longer than the previous date of December 2019. Mr. Draghi also mentioned that some ECB officials raised the possibility of interest rate cuts or a resumption of QE and he said there is “considerable headroom” for more QE.

On the new TLTRO-III loans that begin in September, the ECB was not as accommodative as the TLTRO-II loans but nevertheless set the rate to slide as low as 10 bp above the current deposit rate of -0.40%. The 2-year TLTRO-III loans to Eurozone banks will roll over the expiring TLTRO-II loans and will help keeping the Eurozone banking system fully and cheaply liquefied.

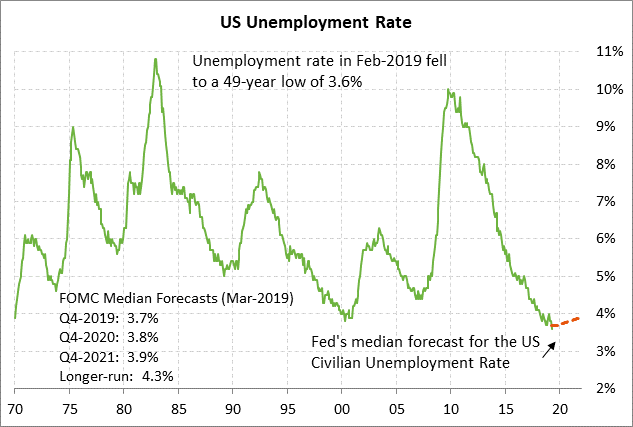

Markets on edge about today’s payroll report after weak ADP report — The market is nervous about today’s payroll report after Wednesday’s news that the May ADP report rose by only +27,000, which was far below expectations of +185,000 and was the weakest report in nine years. The consensus for today’s May payroll report is for a trend increase of +180,000 after April’s strong report of +263,000. Today’s May unemployment rate is expected to be unchanged from April’s 49-year low of 3.6%.

The weak May ADP report of +27,000 could mean that trade uncertainty is causing businesses to put their hiring plans on hold until the economic outlook becomes less muddled. Today’s payroll report will provide some evidence as to whether the ADP report was a fluke or whether there really was a big dip in hiring in May. If there was a big dip in hiring, that would validate the market’s recent worries that the economy is headed for a soft spot, if not a recession, and that the Fed will soon be cutting interest rates. The market is currently discounting -60 bp of rate cuts by the end of 2019 and a further -29 bp rate cut in 2020.

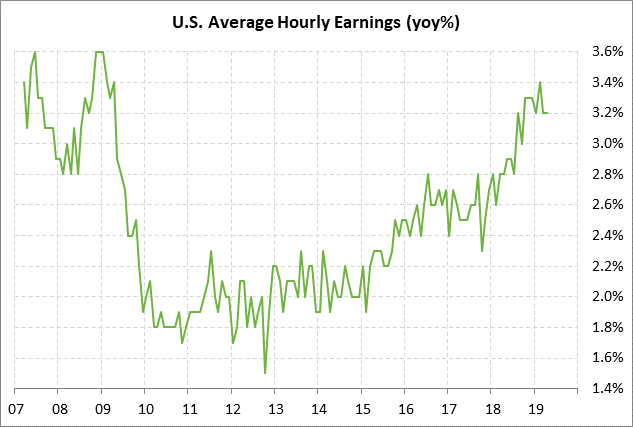

On the wage front, the consensus is for today’s May average hourly earnings report to be unchanged from April’s level of +3.2% y/y, which was just 0.2 points below the 10-year high of +3.4% posted in February.

Attachment file(s):