- US/Mexico meetings will continue Thursday after “not nearly enough” progress

- Mnuchin will meet with PBOC Governor

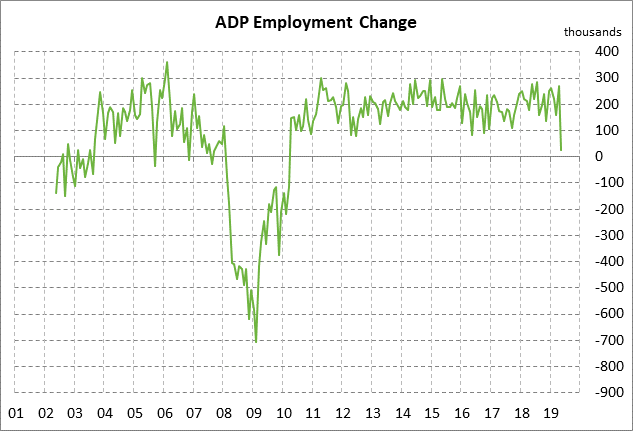

- Weak ADP report raises red flag for Friday’s payroll report

- Italian bonds take in stride EU disciplinary procedure

- ECB expected to announce TLTRO terms but no policy shifts

US/Mexico meetings will continue Thursday after “not nearly enough” progress — High-level US/Mexican talks on migration and tariffs will continue today after no agreement was reached on Wednesday. President Trump Wednesday evening tweeted that some progress was made in Wednesday’s meeting but “not nearly enough.” He said the talks would resume on Thursday. The talks in Washington include Mexican Foreign Minister Ebrard, Vice President Pence, U.S. Secretary of State Pompeo, acting Homeland Security Secretary McAleenan, and other U.S. and Mexican officials.

Mexican officials reportedly came to the meeting with a list of concessions, but they also came with demands for more U.S. support to address the migration crisis. They also came with news that Mexican officials have a list of U.S. products that will be hit with retaliatory tariffs if President Trump goes ahead with his plan to slap a 5% tariff on all Mexico imports on Monday.

President Trump earlier this week made it sound as though he had already decided to go ahead with Monday’s tariff, saying, “It’s more likely the tariffs go on and we’ll probably be talking during the time the tariffs are on.” Since then, however, Mr. Trump has been lambasted by Republican Senators who are calling on him not to impose the tariff on Mexican imports since that would be politically unpopular in their states and could also derail passage of the USMCA deal in Congress.

A US/Mexican deal is being hampered by the fact that President Trump is out of the country. Mr. Trump is staying in Ireland on Wednesday and Thursday nights at his Doonbeg golf club, making a day trip to France on Thursday for D-Day commemorations, according to the Washington Post. Mr. Trump is expected to return to Washington on Friday. Obviously, there will be no US/Mexican deal to avert the 5% tariff on Monday until President Trump decides for himself whether Mexico has made enough concessions to stop migration to the U.S.

Mnuchin will meet with PBOC Governor — Treasury Secretary Mnuchin this weekend will hold a bilateral meeting with PBOC Governor Yi Gang when they are both in Japan for the 3-day G20 meeting of finance ministers and central bankers, according to official announcements on Thursday.

With its choice of the PBOC Governor as Mr. Mnuchin’s meeting partner, China seems to be keeping a freeze on US/Chinese trade talks since Mr. Mnuchin is not meeting with China’s finance minister, his natural counterpart, and is meeting with an official who is only peripherally involved in the US/Chinese trade talks.

U.S. officials still seem to be hoping that Treasury Secretary Mnuchin this weekend might be able to break the ice with Chinese officials and get a definitive meeting set between Presidents Trump and Xi on the sidelines of the G20 summit on June 28-29 in Osaka, Japan. A Trump-Xi meeting still seems likely to take place, although China appears to be slow walking the confirmation of that meeting.

The markets are hoping that a Trump/Xi meeting can get US/Chinese trade talks back on track with a promise by Mr. Trump to defer his threat of a 25% tariff on another $300 billion of Chinese goods. If there is no Trump/Xi meeting, then it seems assured that President Trump will proceed with his 25% tariff on another $300 billion of Chinese goods and that China will retaliate with tariffs, a rare-earth export shutdown, blacklisting of U.S. companies, a travel slowdown, and a spate of negative rhetoric.

Weak ADP report raises red flag for Friday’s payroll report — The markets are on heightened alert for weakness in Friday’s May payroll report after Wednesday’s very weak May ADP employment report of +27,000, which was far below the consensus of +185,000 and was the weakest report in nine years. The report could mean that trade tensions are causing businesses to delay their hiring plans until the economic outlook becomes less muddled. Prior to Wednesday’s surprisingly weak ADP report, the consensus was for Friday’s payroll report to show a trend increase of +180,000 after April’s report of +263,000.

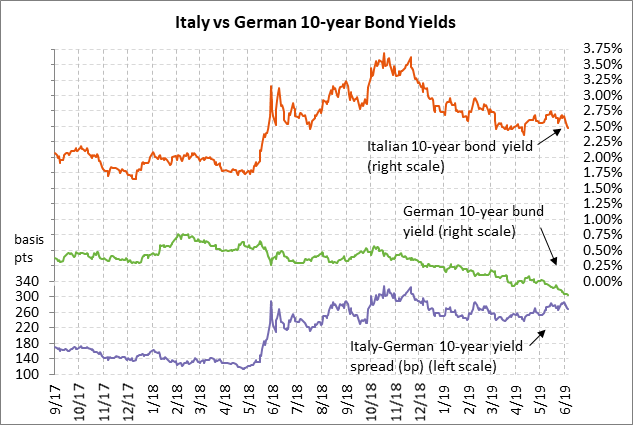

Italian bonds take in stride EU disciplinary procedure — The Italian 10-year bond yield on Wednesday fell by -5 bp to a 1-3/4 month low of 2.47%. The 10-year yield has now fallen by -28 bp from the mid-May 3-1/4 month high of 2.75%. After an initial mini-panic about the EU challenge to Italy’s budget, the Italian bond market is now taking the issue in stride even though the European Commission yesterday went ahead with its disciplinary review of Italy’s budget and debt levels.

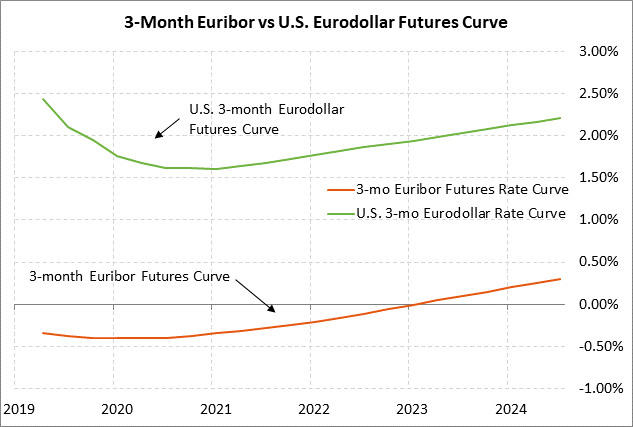

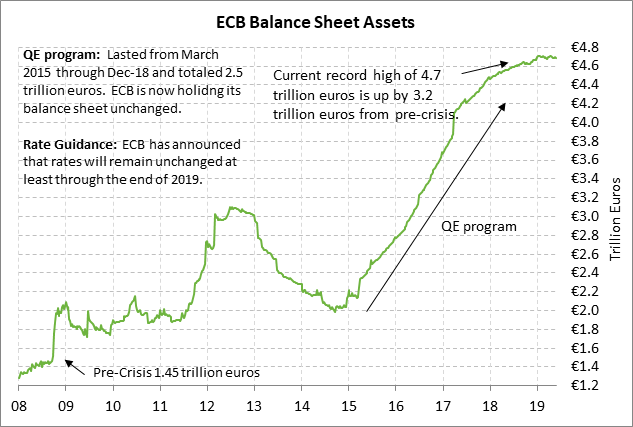

ECB expected to announce TLTRO terms but no policy shifts — The markets are expecting the ECB today to announce favorable terms on its long-term TLTRO-III loans to banks with a rate of -0.25% or less. The ECB will provide seven quarterly rounds of long-term 2-year loans to European banks starting in September. The ECB must roll-over expiring TLTRO-II loans that were granted four years ago or banks would have to find more expensive funding elsewhere.

The ECB today is expected to leave its guidance unchanged with its promise to leave rates unchanged until at least the end of 2019 and to keep its balance sheet constant “for an extended period of time past the date when it starts raising the key ECB interest rates.” However, there is an outside chance that the ECB could change the guidance so that it says there will be no rate hike until at least early 2021, leaving open the possibility of a rate cut. The market is currently discounting a -10 bp rate cut by July 2020.