- Weekly global market focus

- Little chance of a FOMC rate hike this week

- Peak SPX earnings week arrives

- U.S. PCE core deflator expected unchanged but inflation expectations rise to 3-1/4 year high

Weekly global market focus — The U.S. markets this week will focus on (1) the Tue/Wed FOMC meeting, which is expected to produce an unchanged monetary policy at Janet Yellen’s last meeting before Jerome Powell takes over as the new Fed Chair this Saturday, (2) President Trump’s State of the Union address on Tuesday evening in which he expected to outline his latest infrastructure plan, (3) the peak earnings week with 119 of the S&P 500 companies scheduled to report, (4) the prospects for NAFTA where the latest negotiating round will wrap up today with a meeting among trade ministers, (5) a full slate of U.S. economic reports capped by Friday’s Jan payroll report (expected +180,000 after Dec’s +148,000), and (6) Wednesday’s Treasury refunding announcement where the Treasury is expected to announce an increase in its auction sizes to cover a larger U.S. budget deficit.

This will be a short work week for Congress since Republicans and Senate Democrats will depart on Wednesday for their respective policy retreats. Nevertheless, the markets will be watching for any progress in Congress on a budget agreement ahead of next Thursday’s (Feb 8) expiration of the latest continuing resolution. President Trump in his State of the Union address on Tuesday night will not announce a U.S. withdrawal from NAFTA, according to media reports citing White House sources.

In Europe, the focus will be on a heavy slate of economic data including GDP reports on Tuesday and CPI reports on Wednesday. The markets will be watching to see if Catalonia’s parliament on Tuesday raises the ire of the Spanish central government by voting to reappoint Carles Puigdemont as its regional president even though he is a fugitive in exile and is subject to arrest if he returns to Spain. IG Metall, Germany’s largest union, is expected to call 1-day strikes this week at industrial giants such as Siemens and Daimler to press its demands for higher wages. The markets are also watching Italian politics as the national election is now just 5 weeks away on March 4.

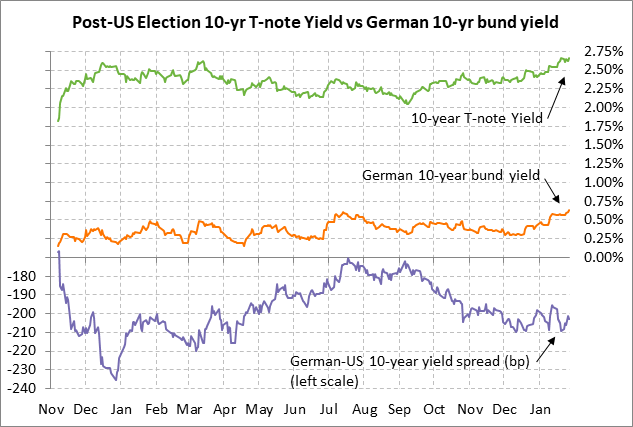

The European markets this week will focus on Eurozone bond yields as the German 10-year bund yield last Thursday rose to a 2-year high of 0.64% and closed the week up +6 bp at 0.63%. The German bund yield has risen sharply by 30 bp in the past six weeks due to (1) strong Eurozone economic data, (2) expectations for the ECB to end its QE program by year-end, and (3) carry-over weakness from the sharp decline in U.S. bond prices.

In Asia, this week’s focus will be on a full slate of Japanese economic data and on Wednesday evening’s China s Jan Caixin manufacturing PMI report (expected unchanged at 51.5 after Dec’s +0.7 to 51.5). Asian stock markets remain strong with the Shanghai Composite index last Friday posting a new 2-year high and with the Nikkei index last Tuesday posting a new 26-1/4 year high.

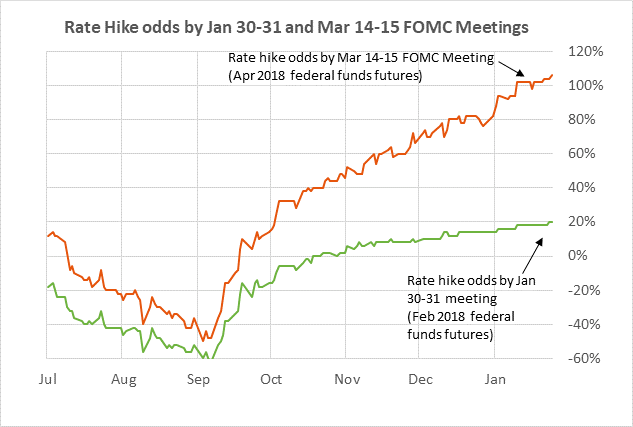

Little chance of a FOMC rate hike this week — The federal funds futures market is discounting only a 20% chance that the FOMC at its Tue/Wed meeting will raise its funds rate target by another +25 bp. The FOMC just raised its funds rate target range by +25 bp to 1.25-1.50% at its last meeting on Dec 12-13, meaning it would be too soon for another rate hike. However, the market is discounting a 100% chance for the first +25 bp rate hike of the year at the next FOMC meeting on March 20-21.

The market is discounting an overall +65 bp rate hike in 2018, which amounts to a bit more than 2-1/2 rate hikes. That is still mildly more dovish than the Fed-dot prediction for three rate hikes in 2018.

Peak SPX earnings week arrives — This is the peak week for Q4 earnings season with 119 of the S&P 500 companies scheduled to report. Notable reports this week include McDonalds and PulteGroup on Tuesday; Facebook, Microsoft, Ebay, AT&T and PayPal on Wednesday; Alphabet, Amazon, Apple, Visa, Mastercard, and UPS on Thursday; and Exxon Mobil and Merck on Friday.

Q4 earnings have thus far been very strong. Of the 133 SPX companies that have reported, 80% have reported above-consensus earnings, well above the long-term average of 64% and the 4-quarter average of 72%, according to Thomson I/B/E/S. Even better, 82% of the reporting companies have announced above-consensus revenue, much better than the long-term average of average of 60% and the 4-quarter average of 63%.

The consensus is for Q4 SPX earnings growth of +13.2% y/y (+10.7% ex-energy), which is better than expectations of +12.0% as of Jan 1, according to Thomson I/B/E/S. Looking ahead, the markets are expecting very strong SPX earnings growth in 2018 of +16.7% in Q1, +16.4% in Q2, +18.2% in Q3, and +15.4% in Q4. On a calendar year basis, the consensus is for earnings growth in 2018 to improve to +16.5% from +12.3% in 2017.

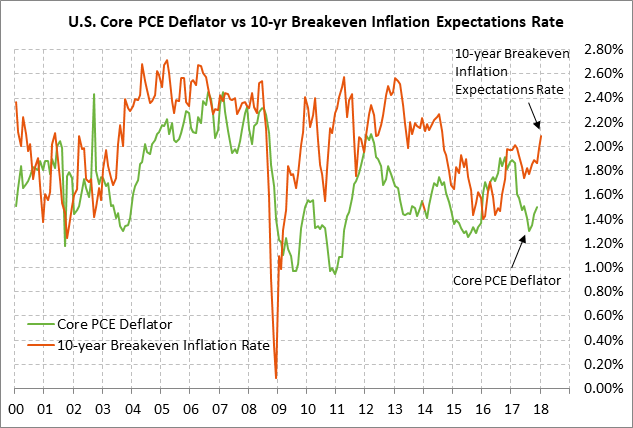

U.S. PCE core deflator expected unchanged — The market consensus is for today’s Dec PCE deflator to ease slightly to +1.7% y/y from Nov’s +1.8% y/y. However, the Dec core PCE deflator is expected to be unchanged from Nov’s +1.5% y/y.

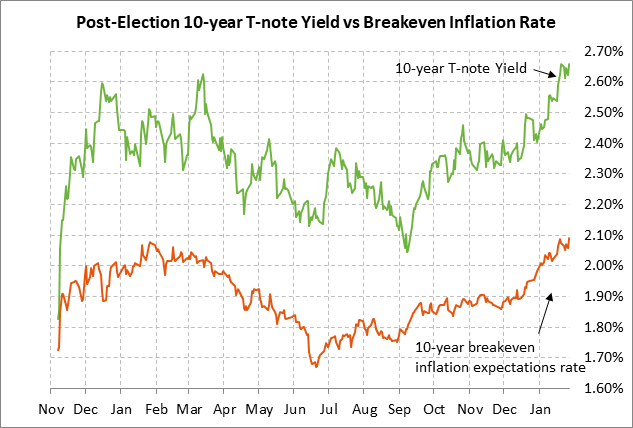

The PCE deflator, which is the Fed’s preferred inflation measure, remains subdued and is not flashing any inflation warnings as yet that could cause the FOMC to accelerate its rate-hike regime. Today’s headline PCE deflator is expected to ease to +1.7% and remain below the Fed’s +2.0% inflation target, while the core PCE deflator is expected to remain even lower at +1.5% y/y. However, market-based measures of inflation present greater concern since the 10-year breakeven rate last Friday rose to a new 3-1/4 year high of 2.095%, which is above the Fed’s +2.0% inflation target.

Weekly global market focus — The U.S. markets this week will focus on (1) the Tue/Wed FOMC meeting, which is expected to produce an unchanged monetary policy at Janet Yellen’s last meeting before Jerome Powell takes over as the new Fed Chair this Saturday, (2) President Trump’s State of the Union address on Tuesday evening in which he expected to outline his latest infrastructure plan, (3) the peak earnings week with 119 of the S&P 500 companies scheduled to report, (4) the prospects for NAFTA where the latest negotiating round will wrap up today with a meeting among trade ministers, (5) a full slate of U.S. economic reports capped by Friday’s Jan payroll report (expected +180,000 after Dec’s +148,000), and (6) Wednesday’s Treasury refunding announcement where the Treasury is expected to announce an increase in its auction sizes to cover a larger U.S. budget deficit.

This will be a short work week for Congress since Republicans and Senate Democrats will depart on Wednesday for their respective policy retreats. Nevertheless, the markets will be watching for any progress in Congress on a budget agreement ahead of next Thursday’s (Feb 8) expiration of the latest continuing resolution. President Trump in his State of the Union address on Tuesday night will not announce a U.S. withdrawal from NAFTA, according to media reports citing White House sources.

In Europe, the focus will be on a heavy slate of economic data including GDP reports on Tuesday and CPI reports on Wednesday. The markets will be watching to see if Catalonia’s parliament on Tuesday raises the ire of the Spanish central government by voting to reappoint Carles Puigdemont as its regional president even though he is a fugitive in exile and is subject to arrest if he returns to Spain. IG Metall, Germany’s largest union, is expected to call 1-day strikes this week at industrial giants such as Siemens and Daimler to press its demands for higher wages. The markets are also watching Italian politics as the national election is now just 5 weeks away on March 4.

The European markets this week will focus on Eurozone bond yields as the German 10-year bund yield last Thursday rose to a 2-year high of 0.64% and closed the week up +6 bp at 0.63%. The German bund yield has risen sharply by 30 bp in the past six weeks due to (1) strong Eurozone economic data, (2) expectations for the ECB to end its QE program by year-end, and (3) carry-over weakness from the sharp decline in U.S. bond prices.

In Asia, this week’s focus will be on a full slate of Japanese economic data and on Wednesday evening’s China s Jan Caixin manufacturing PMI report (expected unchanged at 51.5 after Dec’s +0.7 to 51.5). Asian stock markets remain strong with the Shanghai Composite index last Friday posting a new 2-year high and with the Nikkei index last Tuesday posting a new 26-1/4 year high.

Little chance of a FOMC rate hike this week — The federal funds futures market is discounting only a 20% chance that the FOMC at its Tue/Wed meeting will raise its funds rate target by another +25 bp. The FOMC just raised its funds rate target range by +25 bp to 1.25-1.50% at its last meeting on Dec 12-13, meaning it would be too soon for another rate hike. However, the market is discounting a 100% chance for the first +25 bp rate hike of the year at the next FOMC meeting on March 20-21.

The market is discounting an overall +65 bp rate hike in 2018, which amounts to a bit more than 2-1/2 rate hikes. That is still mildly more dovish than the Fed-dot prediction for three rate hikes in 2018.

Peak SPX earnings week arrives — This is the peak week for Q4 earnings season with 119 of the S&P 500 companies scheduled to report. Notable reports this week include McDonalds and PulteGroup on Tuesday; Facebook, Microsoft, Ebay, AT&T and PayPal on Wednesday; Alphabet, Amazon, Apple, Visa, Mastercard, and UPS on Thursday; and Exxon Mobil and Merck on Friday.

Q4 earnings have thus far been very strong. Of the 133 SPX companies that have reported, 80% have reported above-consensus earnings, well above the long-term average of 64% and the 4-quarter average of 72%, according to Thomson I/B/E/S. Even better, 82% of the reporting companies have announced above-consensus revenue, much better than the long-term average of average of 60% and the 4-quarter average of 63%.

The consensus is for Q4 SPX earnings growth of +13.2% y/y (+10.7% ex-energy), which is better than expectations of +12.0% as of Jan 1, according to Thomson I/B/E/S. Looking ahead, the markets are expecting very strong SPX earnings growth in 2018 of +16.7% in Q1, +16.4% in Q2, +18.2% in Q3, and +15.4% in Q4. On a calendar year basis, the consensus is for earnings growth in 2018 to improve to +16.5% from +12.3% in 2017.

U.S. PCE core deflator expected unchanged — The market consensus is for today’s Dec PCE deflator to ease slightly to +1.7% y/y from Nov’s +1.8% y/y. However, the Dec core PCE deflator is expected to be unchanged from Nov’s +1.5% y/y.

The PCE deflator, which is the Fed’s preferred inflation measure, remains subdued and is not flashing any inflation warnings as yet that could cause the FOMC to accelerate its rate-hike regime. Today’s headline PCE deflator is expected to ease to +1.7% and remain below the Fed’s +2.0% inflation target, while the core PCE deflator is expected to remain even lower at +1.5% y/y. However, market-based measures of inflation present greater concern since the 10-year breakeven rate last Friday rose to a new 3-1/4 year high of 2.095%, which is above the Fed’s +2.0% inflation target.