- EU grants UK only a 6-month Brexit extension

- Minutes show most FOMC members are not thinking about rate cuts

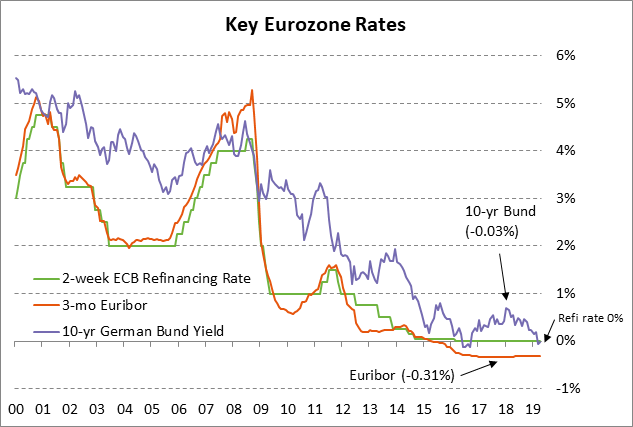

- ECB meeting is in line with expectations

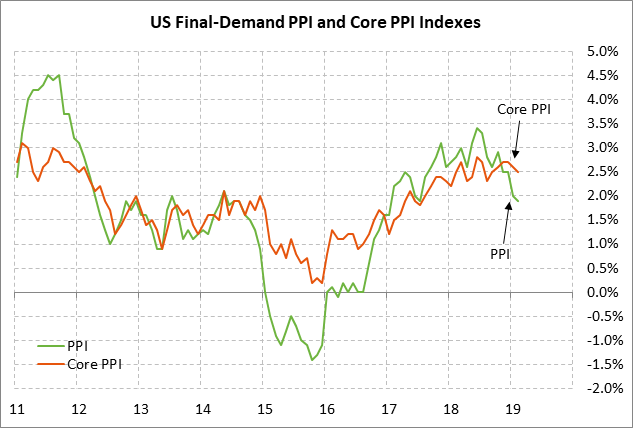

- U.S. core PPI expected to ease slightly

- 30-year T-bond auction to yield near 2.89%

EU grants UK only a 6-month Brexit extension — EU leaders at their emergency summit yesterday granted the UK an extension of the Brexit deadline until only October 31, 2019, shorter than the initial focus on December 2019 or March 2020. The shorter deadline was due to French President Macron’s demand for a shorter extension to prevent a weakening of EU institutions. The extension is the so-called “flextension,” which means that the UK can leave the EU earlier than October 31 if the UK Parliament approves the Brexit withdrawal agreement.

Prime Minister May will now focus on trying to get the UK Parliament to approve the Brexit withdrawal agreement before May 22, which would allow the UK to cancel elections that must now be held on May 23 for the European Parliament. Ms. May in coming days will continue her discussions with the Labour party if see if there is some compromise language on the political declaration that could attract enough Labour votes to push the Brexit withdrawal agreement over the line. The Conservative-Labour talks have shown little progress thus far, but Ms. May reportedly told European leaders that there has been more progress than has been made public.

The Brexit extension until October is good news for the markets since there now won’t be any threat of a chaotic no-deal Brexit until at least October. However, the ongoing Brexit uncertainty will still be a negative for the UK and Eurozone economies. In addition, if the Conservative-Labour talks fail, then Ms. May might have to admit that Parliament is hopelessly deadlocked on Brexit and she might have to call a snap election, thus increasing UK political uncertainty.

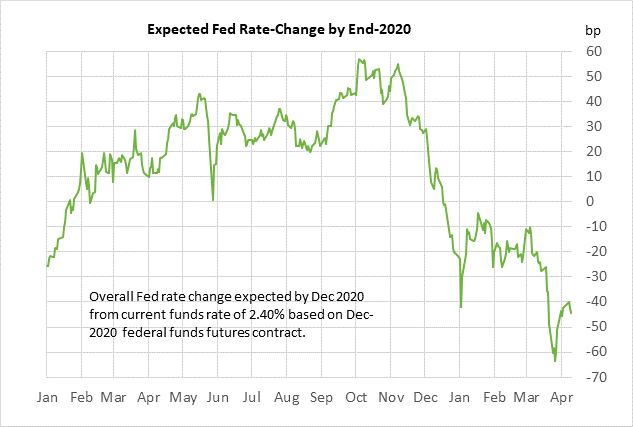

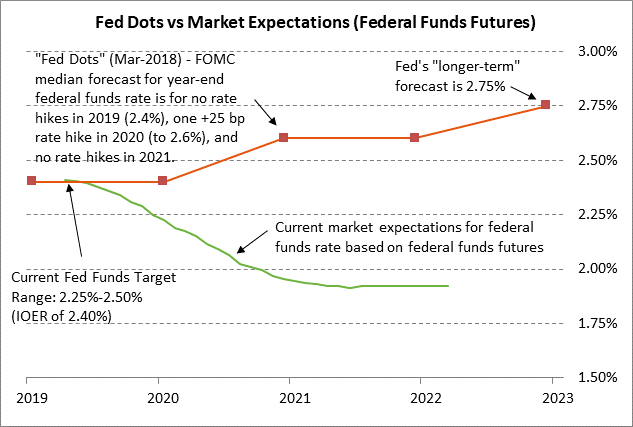

Minutes show most FOMC members are not thinking about rate cuts — Yesterday’s minutes from the March 20-21 FOMC meeting were generally in line with market expectations and had little impact on the markets. The federal funds futures curve yesterday showed no change for the 2019 contracts and a slight 1-2 bp dovish turn for the 2020 contracts.

The federal funds futures market is currently discounting a 60% chance of a -25 bp rate cut by the end of this year. By the end of 2020, the market is fully discounting one rate cut and is discounting an 80% chance of a second rate cut. The market remains far more dovish than the Fed, which is forecasting no rate change in 2019 and a +25 bp rate hike for 2020.

Yesterday’s FOMC minutes confirmed that the Fed remains on hold for the remainder of this year, but that the Fed if anything is leaning more toward a future rate hike than a rate cut. The minutes said that a “majority” of Fed officials expected that the economic outlook and risks “would likely warrant leaving the target range unchanged for the remainder of the year.”

However, the minutes also said that, “Some participants indicated that if the economy evolved as they currently expected, with economic growth above its longer-run trend rate, they would likely judge it appropriate to raise the target range for the federal funds rate modestly later this year.” Yet there were other Fed officials who were open to a rate cut since the minutes said that the views of several members on the funds rate “could shift in either direction based on incoming data and other developments.”

ECB meeting is in line with expectations — Yesterday’s ECB meeting was in line with market expectations and contained little fresh news for the markets to chew on. The ECB did not provide any further details of the TLTRO-III loan program that will begin in September. The markets are now expecting the ECB to release the details on how those loans will be priced at the ECB’s meeting in June. There is speculation that the ECB may keep the rates lower than earlier expected as a means of providing stimulus and further support to bank lending. The ECB at yesterday’s meeting left intact its guidance from the previous meeting that the ECB does not plan to raise interest rates before the end of the year.

U.S. core PPI expected to ease slightly — The consensus is for today’s March headline PPI to be unchanged from April at +1.9% y/y and for the core PPI to ease slightly to +2.4% from April’s +2.5%. In yesterday’s March CPI report, the headline CPI rose to +1.9% y/y from April’s +1.5% but the core CPI eased slightly to +2.0% from April’s +2.1%. The March core CPI on a 3-month annualized basis eased slightly to a 5-month low of +2.0%, matching the Fed’s inflation target. In Feb, the PCE deflator was at only +1.4% y/y and the core deflator was at +1.8%.

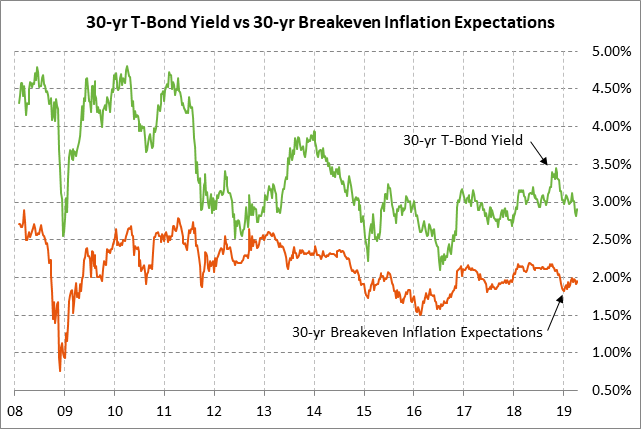

30-year T-bond auction to yield near 2.89% — The Treasury today will conclude this week’s $78 billion coupon package by selling $16 billion of 30-year bonds in the second and final reopening of the 3% 30-year bond of Feb 2049. The 30-year T-note yield has rebounded higher by +10 bp to 2.89% from the 1-1/4 year low of 2.79% seen two weeks ago. Still, the 30-year yield is down sharply by -57 bp from last November’s 4-3/4 year high of 3.46% due to the slower U.S. and global economies, reduced inflation expectations, and the Fed’s switch to a neutral policy from its previous forecast for three more rate hikes.

The 12-auction averages for the 30-year are as follows: 2.30 bid cover ratio, $5 million of non-competitive bids from mostly retail investors, 4.5 bp tail to the median yield, 36.4 bp tail to the low yield, and 43% taken at the high yield. The 30-year is a little below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 61.1% of the last twelve 30-year T-bond auctions, which is a little below the median of 62.1% for all recent Treasury coupon auctions.