- Prospects improve for today’s Brexit vote

- Lighthizer testifies today

- Fed is watching inflation carefully with today’s CPI report expected steady

- 10-year T-note yield remains subdued ahead of today’s auction

Prospects improve for today’s Brexit vote — The prospects improved substantially for the UK Parliament at its vote today to approve Prime Minister May’s Brexit withdrawal agreement. Ms. May on Monday announced, after consultations with the EU, that the UK could implement a “unilateral declaration” to void the Irish backstop and then exit the EU if there is no prospect for a UK-EU trade agreement in coming years. That provision may be enough to assuage worries in Parliament that the Irish backstop could trap the UK indefinitely in the EU.

If Parliament today approves the Brexit separation agreement, then the markets will be very pleased because then nothing will change and the UK will effectively remain within the EU during a transition period until December 2020. On the other hand, if Parliament today votes against Ms. May’s Brexit separation agreement, then the situation becomes much more complicated. In that case, Parliament will have the opportunity on Wednesday to vote against a no-deal Brexit and on Thursday will then have the opportunity to vote to delay the March 29 Brexit deadline.

While there is a clear Parliamentary path to avoid a disastrous no-deal Brexit on March 29, there is still the chance that the UK and EU could stumble into a no-deal Brexit. The betting odds for a no-deal Brexit by April 1 are still material at 20%. There is a chance that hardline Brexiteers, who want to avoid a delay on the March 29 deadline at all costs, might try to maneuver Parliament into a no-deal Brexit, which they see as the lesser evil. Alternatively, the EU and UK and might not be able to agree on an extension of the March 29 deadline considering that the EU wants to impose some tough conditions such as a payment of $1.3 billion for every month that the deadline is extended.

Lighthizer testifies today — USTR Lighthizer is scheduled to testify today before the Senate Finance Committee. The main topic is WTO reform, but other topics are likely to come up such as how close the US/China are to a trade agreement and whether the Trump administration plans to slap tariffs on imported autos.

The Commerce Department recently delivered recommendations to the White House on whether tariffs should be imposed on imported autos on national security grounds. However, those recommendations have not yet been made public even though the U.S. auto industry has been pushing to find out about the plan since tariffs on imported autos and parts, and retaliatory tariffs, could cost U.S. auto companies a bundle. The EU has already said it has a tariff retaliation package ready to go if President Trump slaps tariffs on European autos.

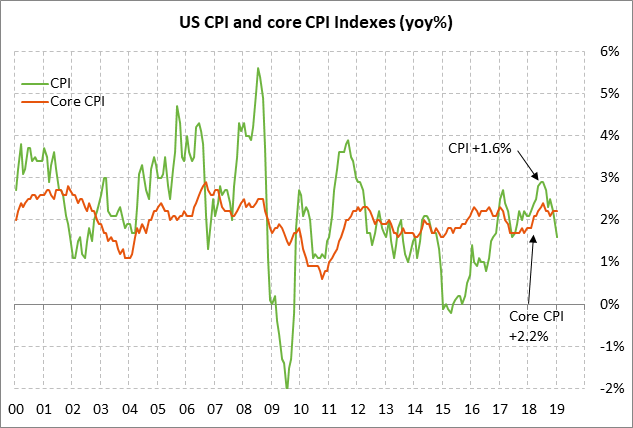

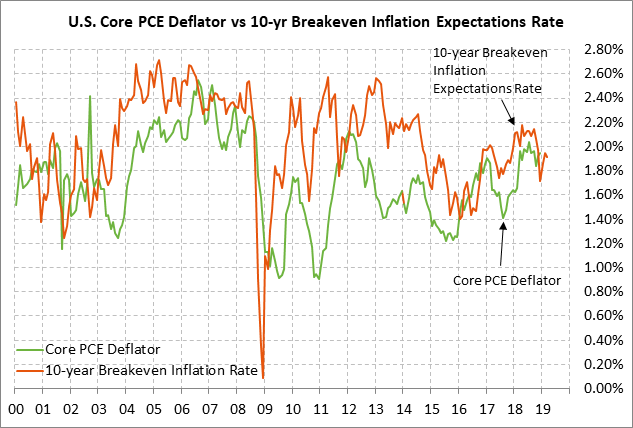

Fed is watching inflation carefully with today’s CPI report expected steady — The markets will carefully watch today’s CPI report since the Fed’s next policy move will be completely dependent on the incoming data. As long as inflation is moving sideways or lower, the Fed will not make any moves to revive its rate-hike regime. However, if inflation should unexpectedly start moving substantially higher, then the Fed will be under pressure to start raising interest rates again.

The consensus is for today’s Feb CPI report to be unchanged from Jan’s +1.6% y/y and for the Feb core CPI to be unchanged from Jan’s +2.2% y/y. The current CPI level of 1.6% y/y is down sharply from the 7-year high of +2.9% y/y posted in summer 2018. The current core CPI of +2.2% is just mildly below the 10-year high of +2.4% posted in July 2018.

Luckily, the Fed’s preferred inflation measure, the PCE deflator, is in weaker shape than the CPI data. In December, the PCE deflator fell to a 1-1/4 year low of +1.7% and the core PCE deflator of +1.9% was slightly below the Fed’s +2.0 inflation target. The Fed has recently made a point of saying that its 2.0% inflation target is symmetrical, which means the Fed would tolerate a period of the core PCE deflator going above +2.0%.

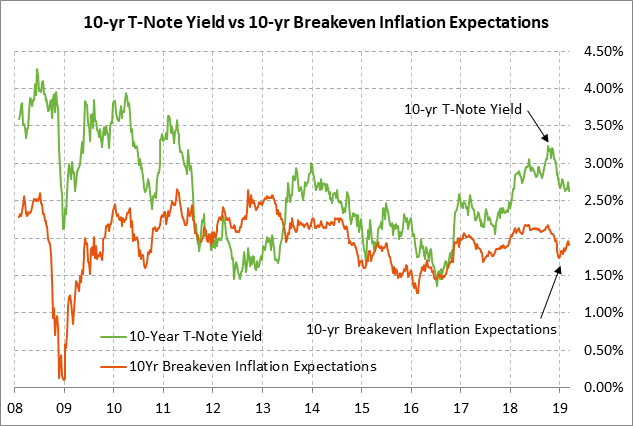

Regarding inflation expectations, the 10-year breakeven inflation expectations rate has rebounded upward by +24 bp to 1.91% from the early-Jan 1-3/4 year low of 1.67%. However, the 10-year breakeven rate remains 9 bp below the Fed’s +2.0% inflation target and 30 bp below last May’s 4-1/2 year high of 2.21%.

10-year T-note yield remains subdued ahead of today’s auction — The 10-year T-note yield so far this year has been moving sideways in the narrow range of about 2.60-2.80%. The 10-year T-note yield in Nov/Dec fell sharply by nearly 50 bp to the current range from October’s 7-3/4 year high of 3.26% due to (1) the sharp global stock market correction in Q4, (2) decelerating economic growth in China and Europe, (3) increased risks for the U.S. economy due to slower overseas growth and the fading stimulus from the 2018 tax cut, (4) the plunge in oil prices in Q4, which pushed inflation expectations lower, and (5) the Fed’s switch at its January meeting to a fully neutral policy and its abandonment of its 3-year rate-hike regime.

The Treasury today will sell $24 billion of 10-year T-notes in the first reopening of the 2-5/8% T-note of Feb 2029 that the Treasury first sold in February. The $24 billion size of today’s auction is unchanged from the Treasury’s last reopenings in Dec-Jan, but up from the $20 billion size that prevailed during 2016-17. The Treasury will conclude this week’s $73 billion package by selling $16 billion of reopened 30-year T-bonds on Wednesday. The 12-auction averages for the 10-year T-note are: 2.50 bid cover ratio, $21 million in non-competitive bids, 4.4 bp tail to the median yield, 23.8 bp tail to the low yield, 41% taken at the high yield, and 62.2% taken by indirect bidders (mildly above the recent coupon average of 61.3%).