- Weekly global market focus

- US/Chinese trade talks slow as China balks on enforcement

- Brexit crunch hits this week

- U.S. Jan retail sales expected to remain weak

- 3-year T-note auction yield expected near 2.44%

Weekly global market focus — The U.S. markets this week will focus on (1) continued concern about whether the U.S. and China will reach a trade deal after reports that China is pushing back on enforcement issues and is reluctant to schedule a Trump-Xi summit, (2) this week’s busy U.S. economic calendar amidst new doubts about the U.S. economy after last Friday’s very weak Feb payroll report of +20,000, (3) the Treasury’s sale of $78 billion of 3-year, 10-year, and 30-year securities, (4) today’s release of the Trump administration’s budget for the new fiscal year, which is likely to be overlooked by mostly bipartisan Congressional spending plans, and (5) earnings reports from six of the S&P 500 companies including Oracle and Adobe.

In Europe, the focus will mainly be on Brexit, which has entered its most critical week yet. The markets will also be on alert for any additional weak Eurozone economic data after the ECB last week downgraded its GDP growth forecasts, extended its promise for unchanged interest rates through year-end, and announced new long-term TLTRO bank loans starting in September.

In Asia, the focus is on the US/Chinese trade talks and on Chinese economic data after last Friday’s news that Chinese Feb exports fell by -20.7% and by a combined -4.6% in Jan-Feb, which caused new worries about the deceleration on China’s economy. China then reported over the weekend that Feb aggregate financing rose by only 703 billion yuan, less than expectations of +1.3 billion yuan, and Feb new yuan loans rose by +886 billion yuan, less than expectations of +950 billion yuan. The consensus is for this Wednesday night’s Chinese Feb industrial production to ease to +5.5% y/y from Jan’s +6.2% and for Feb retail sales to ease to +8.1% year-to-date from Jan’s +9.0%.

The Bank of Japan at its policy meeting on Friday is expected to leave its monetary policy unchanged. Japan’s economy is going through a weak patch with GDP growth of -2.6% (q/q annualized) in Q3 and +1.9% in Q4. However, the economy is not bad enough to encourage the BOJ to take any new stimulus measures.

US/Chinese trade talks slow as China balks on enforcement — US/Chinese trade talks are slowing as China pushes back on U.S. demands for what China perceives to be a one-sided enforcement mechanism. In addition, Chinese officials are now reluctant to hold a Trump-Xi summit unless an agreement has been concluded and the summit is essentially just a signing ceremony. The Wall Street Journal on Saturday reported that Chinese officials are concerned about President Trump’s walk-out from his recent summit with Kim Jong Un and are now reluctant to schedule a Trump-Xi summit where the same thing could happen if there are aggressive last-minute U.S. negotiating demands. White House advisor Kudlow on Sunday said that “We’re making great progress” on the US/Chinese trade talks and he is “optimistic” about a Trump/Xi meeting, possibly in March or April, which was somewhat of a downgrade from his recent remarks suggesting that historic agreement was imminent.

Brexit crunch hits this week — There are now only 18 days left until the March 29 Brexit deadline when the UK is scheduled to leave the EU with, or without, a separation agreement.

Parliament is scheduled to vote on Ms. May’s Brexit agreement on Tuesday. The markets will be very happy if Parliament approves the bill, but odds still seem to be against approval. Indeed, the Sunday Times reported that Ms. May’s loss could be worse than the first vote on her bill, which went down to defeat by an historic margin of 230 votes.

If Parliament rejects the bill, then Parliament on Wednesday will have the opportunity to vote to reject a no-deal Brexit and on Thursday will have the opportunity to extend the March 29 deadline. The only clear majority in Parliament is for preventing a no-deal Brexit, so it seems likely that the deadline will be extended. Even if Parliament votes against Ms. May’s Brexit separation agreement this week, Ms. May will still have another two weeks to try to push her plan or some variant over the finish line prior to the March 29 deadline.

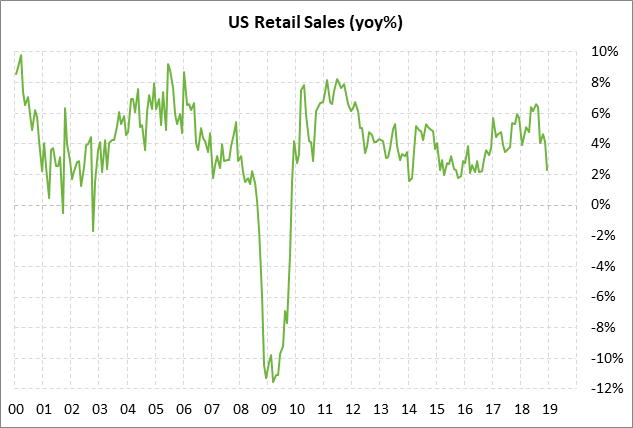

U.S. Jan retail sales expected to remain weak — The consensus is for today’s Jan retail sales report to be unchanged m/m and +0.3% ex-autos, failing to show much of an improvement after December’s very weak report of -1.2% and -1.8% ex-autos. U.S. consumers were in a bad mood in January, as seen by the fact that the Jan Conference Board U.S. consumer confidence index fell by -4.9 points and the Jan University of Michigan U.S. consumer sentiment index fell by -7.1 points. U.S. consumer confidence was undercut in January by the U.S. government shutdown and concern about the Q4 stock market weakness, although stocks rebounded higher in January. The good news is that U.S. consumer confidence rebounded higher in February by +9.7 points (Conference Board) and +4.3 points (Univ of Michigan), which suggests that next month’s February retail sales report may be stronger than today’s report for January.

3-year T-note auction yield expected near 2.44% — The Treasury today will sell $38 billion of 3-year T-notes. The Treasury will then continue this week’s $73 billion package by selling $24 billion of reopened 10-year T-notes on Tuesday and $16 billion of reopened 30-year T-bonds on Wednesday. The 3-year T-note yield last Friday fell to a 9-week low and closed the day at 2.44%, which is just 11 bp above the early-Jan 13-month low of 2.33%. The 12-auction averages for the 3-year T-note are: 2.66 bid cover ratio, $89 million in non-competitive bids, 3.2 bp tail to the median yield, 17.3 bp tail to the low yield, 58% taken at the high yield, and 46.4% taken by indirect bidders (far below the recent coupon average of 61.3%).