- U.S. unemployment report expected to show steady economy

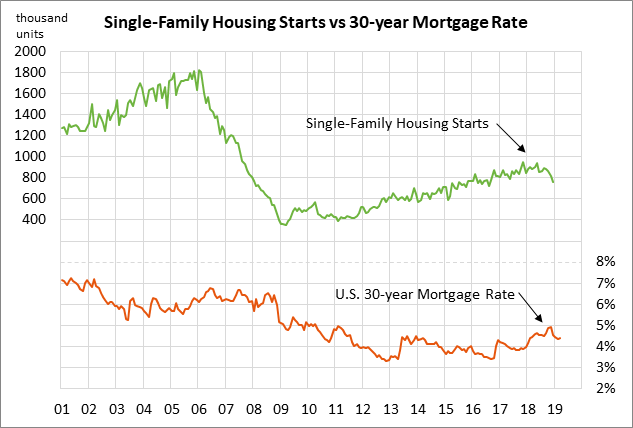

- U.S. housing starts expected to partially recover from 2-1/4 year low

- ECB moves faster than expected with dovish measures

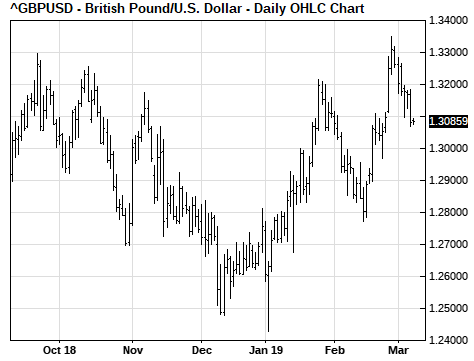

- Brexit crunch hits next week

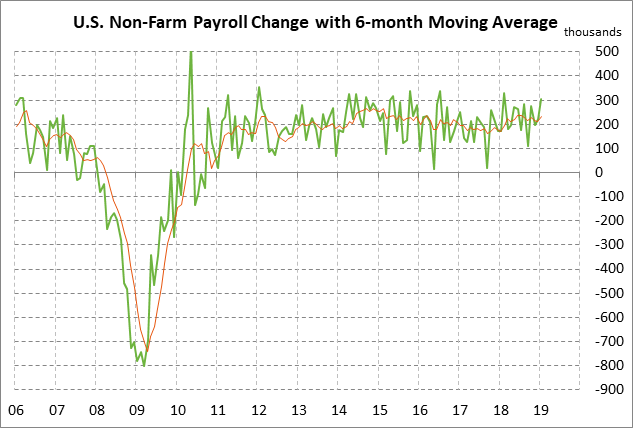

The market consensus is for today’s Feb non-farm payroll report to show an increase of +180,000, which would be down from Jan’s strong report of +304,000 and below the 12-month trend average of +234,000. The market is generally expecting payroll growth to downshift this year to the +180,000 area since the U.S. economy will slow this year after last year’s surge on the tax cut.

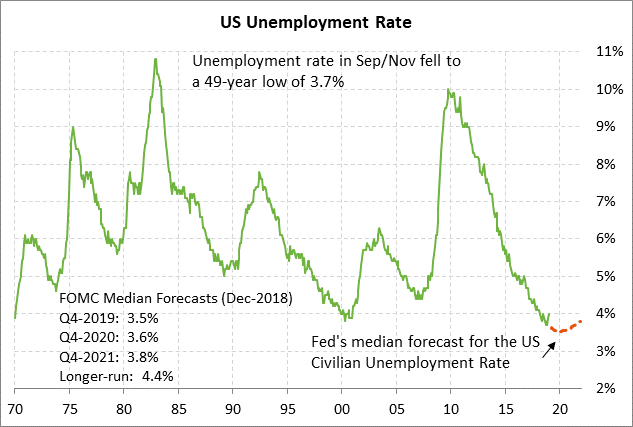

The consensus is for today’s Feb unemployment rate to fall by -0.1 point to 3.9%, reversing Jan’s +0.1 point increase to 4.0%. Today’s expected Feb unemployment rate of 3.9% would be only 0.2 points above 49-year low of 3.7% posted in September 2018. The Fed is expecting the unemployment rate to fall to 3.5% by year-end. The current Jan unemployment rate of 4.0% is well below the Fed’s view of a longer-run natural unemployment rate of 4.4%, which illustrates the continued tightness of the U.S. labor market.

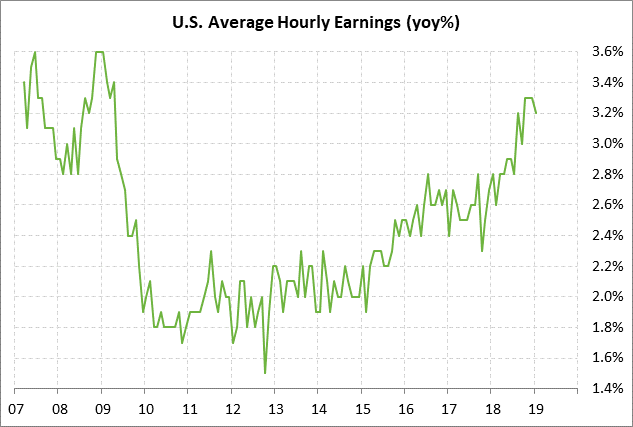

The tight labor market is expected to keep upward pressure on wages. The consensus is for today’s Feb average hourly earnings report to edge higher to +3.3% y/y from Jan’s +3.2%, thus matching the 10-year high of +3.3% posted in Oct-Dec 2018.

U.S. housing starts expected to partially recover from 2-1/4 year low — The consensus is for today’s Jan housing starts report to rise +10.4% to 1.190 million, recovering most of December’s -11.2% decline to 1.078 million. However, housing starts took a hit in late 2018 with a decline to a 2-1/4 year low in December that was 19% below the 11-year high posted in Jan 2018. Housing starts took a hit in late 2018 due to poor home sales and rising mortgage rates. However, mortgage rates have since fallen back, thus reviving some home builder confidence.

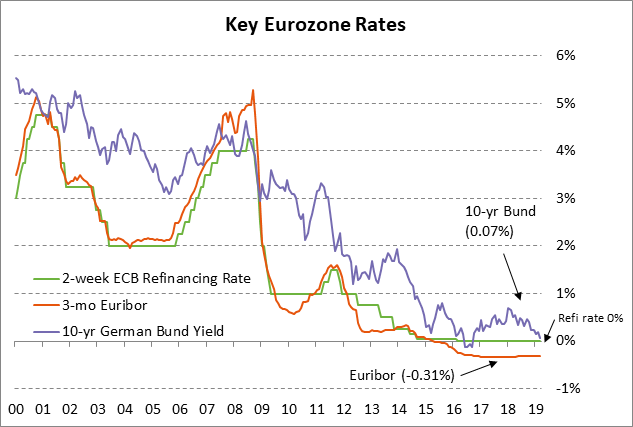

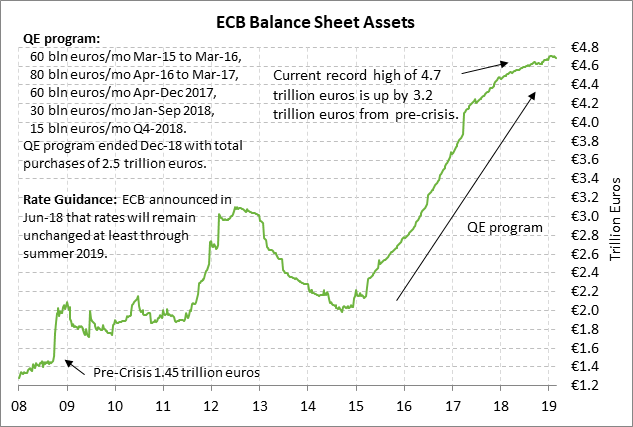

ECB moves faster than expected with dovish measures — The ECB on Thursday surprised the markets somewhat by moving faster than expected with its anticipated dovish measures. The ECB announced the details of new TLTRO bank loans and also extended its promise for unchanged rates until the end of the year from the previous timing of this summer. However, there was some disappointment that the TLTRO loans were not more aggressive.

In addition, the ECB’s quick dovish action made the markets wonder whether the ECB knows something the markets don’t and whether there are larger downside risks for the Eurozone economy. The ECB itself cut its 2019 GDP forecast sharply to +1.1% from +1.7%. Bloomberg later in the day reported that some ECB officials doubt the Eurozone economy will do as well as even the ECB’s 2019 GDP forecast of 1.1%.

The ECB changed its guidance on interest rates so that it now expects interest rates to remain at current levels “at least through the end of 2019.” That didn’t tell the markets anything they didn’t already know since the market is not expecting a rate hike until mid-2020. Still, it was a dovish factor that the ECB confirmed that it won’t raise rates this year.

The ECB announced that it will begin quarterly targeted longer-term refinancing operations (TLTROs) starting in September and lasting through March 2021. The markets were a bit disappointed that the TLTRO-III operations will not begin in June when banks need liquidity to replace the loss of nearly $400 billion worth of TLTRO-II in their ratio calculations. In addition, the new TLTRO-III loans will be only two years in duration versus four years for TLTRO-II, and the interest rate will be higher on the new TLTRO-III loans.

Brexit crunch hits next week — There are now only three weeks left until the March 29 Brexit deadline when the UK is scheduled to leave the EU with or without a separation agreement. If Parliament approves a separation agreement, then the UK will effectively remain within the EU until December 2020 under a transition period and nothing will change. However, if the UK leaves the EU without a separation agreement, then the “no deal” Brexit will usher in chaos since the UK will suddenly be surrounded by hard borders with tariffs and there will be massive delays in shipping goods in and out of the country.

The EU yesterday made a new offer to try to break the impasse on the Irish backstop by beefing up the review process that is already in the agreement. However, that is far short of what Prime Minister May is asking for and seems unlikely to push Parliament over the line to support Ms. May’s Brexit agreement. Ms. May might travel to Brussels this weekend to plead for some last-minute concessions.

Parliament is scheduled to vote on Ms. May’s Brexit agreement this coming Tuesday. The markets will be very happy if Parliament approves the bill, but odds still seem to be against approval. If Parliament rejects the bill, then Parliament on Wednesday will have the opportunity to vote to reject a no-deal Brexit and on Thursday will have the opportunity to extend the March 29 deadline. The only clear majority in Parliament is for preventing a no-deal Brexit, so it seems very likely that the deadline will be extended. Even if Parliament votes against Ms. May’s Brexit separation agreement next week, Ms. May will still have another two weeks to try to push it over the finish line prior to the March 29 deadline.